Are you a small business owner in need of a financial boost to help your venture thrive? Crafting a well-structured loan inquiry letter can significantly enhance your chances of securing the funds you need. In this article, we'll walk you through the essential components of an effective letter that captures the attention of lenders and clearly outlines your financial needs. So, let's dive in and explore how to create a compelling loan inquiry that opens doors to new opportunities!

Image cover: Letter Template For Small Business Loan Inquiry

Letter Template For Small Business Loan Inquiry Samples

Business Information

A small business loan inquiry requires essential business information for accurate assessment. Business name should reflect the entity, such as "Tech Innovations Inc." located in Austin, Texas. Entity type includes considerations like sole proprietorship, LLC (Limited Liability Company), or corporation. Date established (e.g., January 15, 2020) highlights the business history, while the number of employees (e.g., 15) demonstrates growth potential. Revenue figures, like annual sales of $250,000, indicate existing financial health. Purpose of the loan can range from expansion efforts in emerging markets to purchasing equipment crucial for operational efficiency. Documentation such as a business plan lays out strategic goals and financial forecasts, enhancing credibility for loan approval.

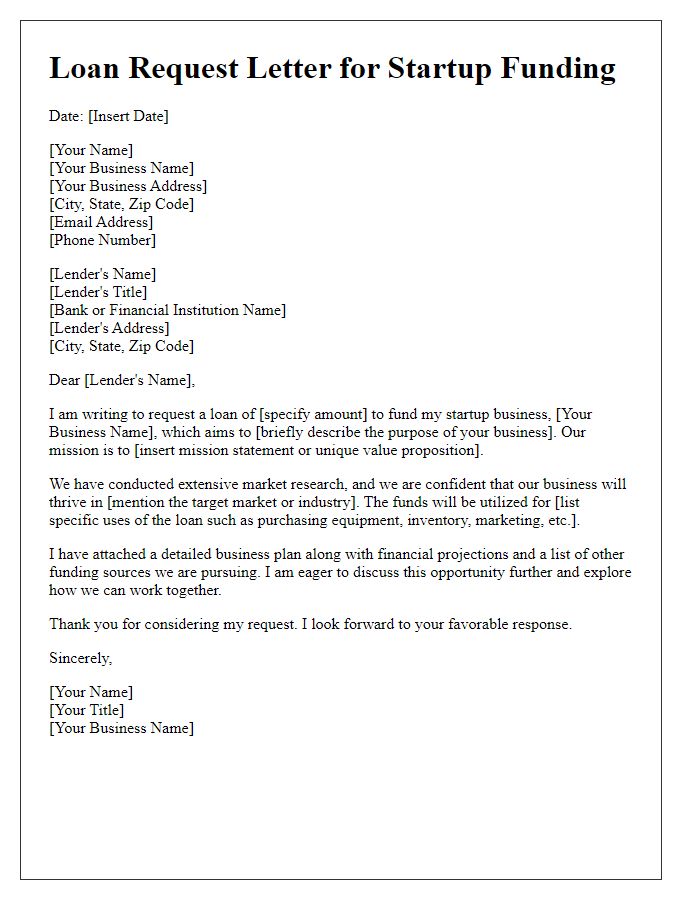

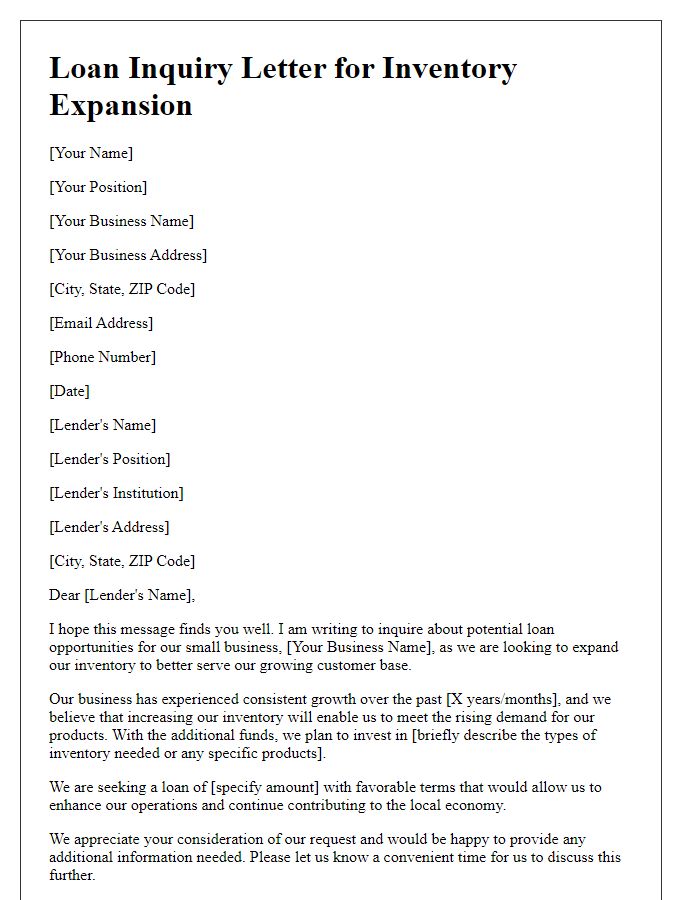

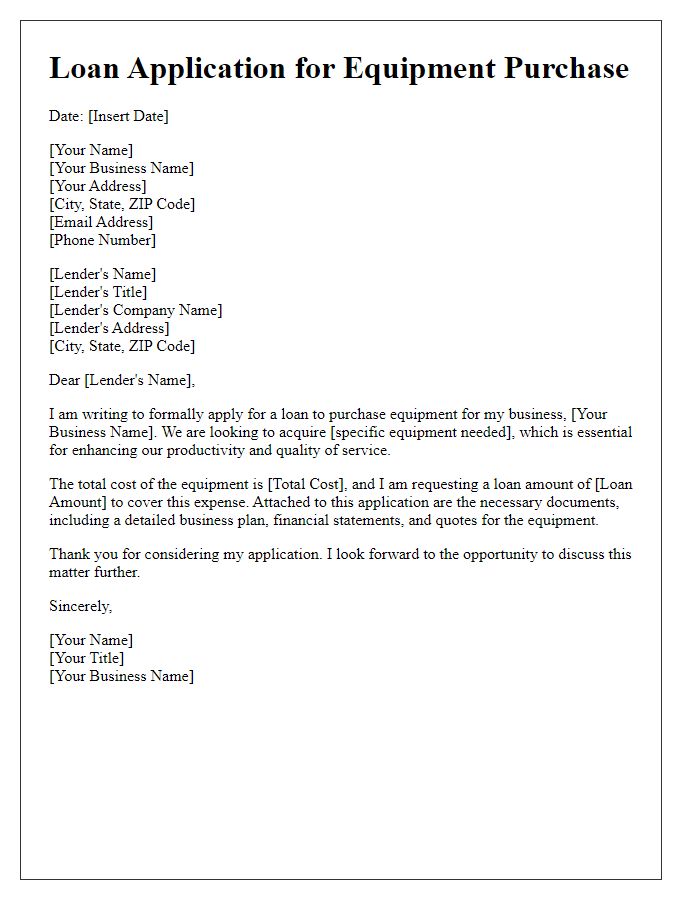

Loan Amount and Purpose

A small business loan inquiry typically includes essential details like the requested loan amount and specific purpose for funding. For instance, a business seeking $50,000 might aim to enhance operational efficiency by purchasing new equipment, such as state-of-the-art computers valued at $15,000, and increasing inventory by $25,000 to meet rising demand. Additionally, $10,000 could be allocated to marketing initiatives to boost visibility in the local market, specifically targeting neighborhoods in cities like Seattle or Portland. This structured approach not only clarifies the financial requirements but also demonstrates the planned impact of the loan on business growth and community engagement.

Financial History

A small business seeking a loan must present a well-documented financial history highlighting key aspects such as annual revenue, cash flow trends, and outstanding debts. The last three years of financial statements (profit and loss, balance sheet) should be prepared to reflect a positive trajectory, especially in 2022 where an average revenue growth of 15% is noted. Essential documents, including tax returns, bank statements, and accounts receivable aging reports, provide a transparent overview of fiscal management. A strong credit score, ideally above 700, supports favorable loan terms. Maintaining records of any previous loans, showing timely repayments, demonstrates reliability and helps build lender confidence in the business's financial stability.

Collateral Details

A small business seeking a loan may need to provide collateral details to assure lenders of repayment security. Common collateral types include real estate, such as commercial properties or residential homes, inventory, which may include raw materials or finished goods, and equipment assets like machinery or vehicles. Valuation of these assets can vary significantly; for example, commercial real estate properties may be assessed at several hundred thousand dollars, while specialized equipment could range from thousands to millions based on its condition and market demand. Additionally, documentation such as property deeds, inventory lists, and equipment appraisals serve to reinforce the loan application, demonstrating the tangible value used to back the borrowed funds.

Contact Information

Local small businesses often seek funding to expand operations, manage cash flow, or invest in new equipment. A thorough inquiry about small business loans requires essential contact details for effective communication. This includes business name, owner's name, and phone number to establish direct communication. Email address is crucial for formal correspondence. Business address provides location context, which may influence loan decisions, particularly in areas with economic growth. Additional information such as business type--retail, service, or manufacturing--helps lenders assess loan eligibility and potential risks. Understanding demographic details, including years in operation and revenue figures, can enhance the application's reliability and impact.

Read Also: Our Loan application's Blogs

Comments