Are you considering taking over an existing mortgage? Understanding the process of mortgage assumption can be tricky, but it could save you time and money. This article will guide you through the ins and outs of mortgage assumption notifications and what you need to do to ensure a smooth transition. So, grab a cup of coffee and read on to learn more about this potential financial opportunity!

Image cover: Letter Template For Mortgage Assumption Notification

Letter Template For Mortgage Assumption Notification Samples

Borrower and lender information

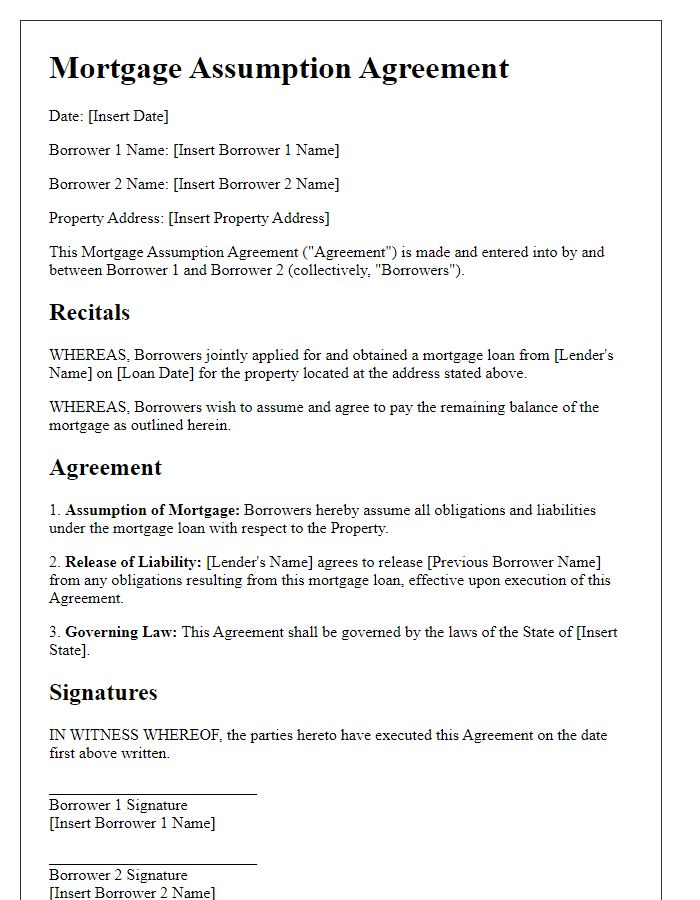

A mortgage assumption notification involves a transfer of mortgage responsibility from one borrower to another, underlining the details of the agreement. The documentation must include the borrower's personal information, including full name, address, and contact details. Lender information should consist of the financial institution's name, address, and relevant contact information. It's also essential to state the mortgage account number linked to the property, typically recorded in official documentation. Additionally, the notification will cover the terms attached to the assumption, such as any fees associated with the transfer process, interest rates, and any changes in payment schedules. Clear communication is vital to ensure all parties involved understand their roles and responsibilities for this financial transaction.

Property details and mortgage terms

The process of mortgage assumption involves transferring the existing mortgage obligation from one borrower to another, impacting property ownership and financial responsibilities. Properties involved in this action typically include single-family homes, multi-family residences, or condominiums, often valued at significant amounts dictated by real estate markets. Mortgage terms can vary, typically comprising the principal balance that remains, the interest rate applicable (which may be lower or higher than current market rates), and the remaining loan duration, which might be 15, 20, or 30 years. Noteworthy details include whether the mortgage is assumable, the specifics of the loan servicer's approval process, and any fees associated with the assumption process. The assumption of a mortgage can also result in implications for property taxes and insurance obligations, crucial in maintaining the property's equity.

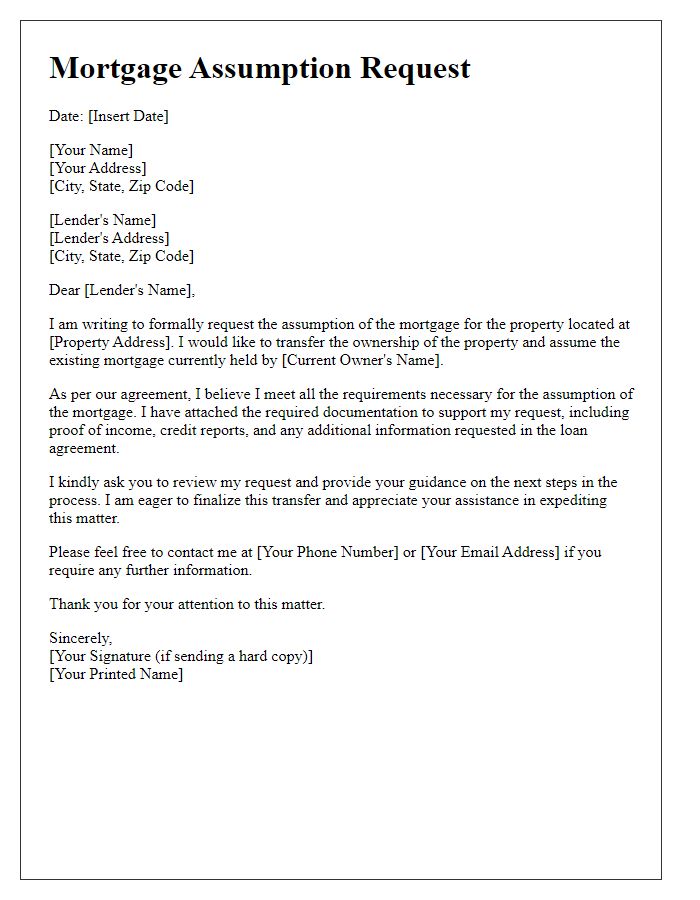

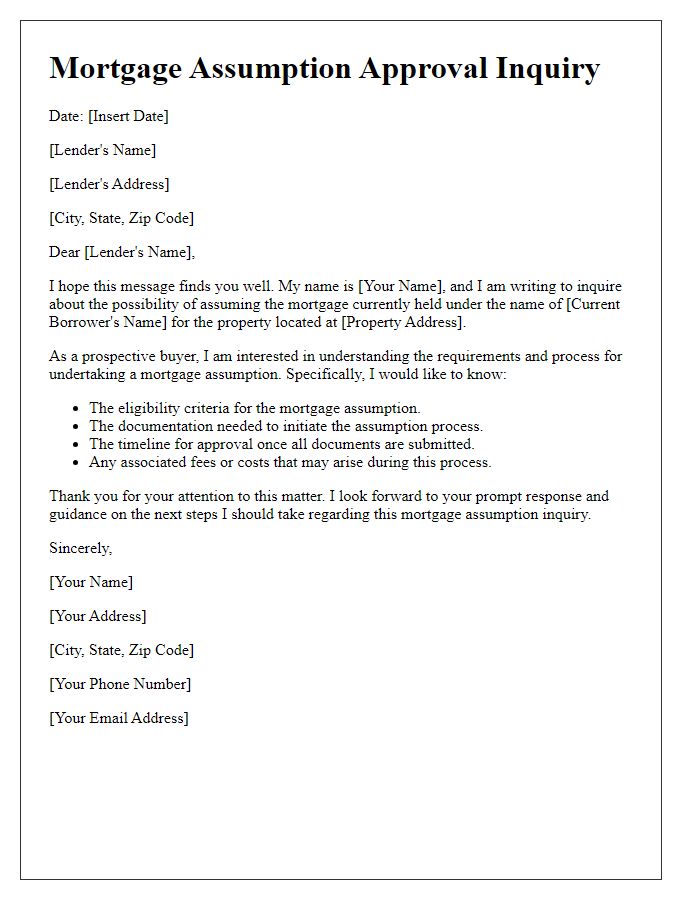

Request for assumption approval

Mortgage assumption notifications require specific details to facilitate a smooth transition of responsibility for the mortgage loan. When a borrower seeks to transfer their mortgage obligations to another party, a formal request for assumption approval is essential. This notification should include information such as the property address, mortgage account number, and the names of the current borrower and the prospective borrower. Additionally, essential context includes the original loan terms, applicable interest rate (for instance, 4.5% fixed), and any pertinent financial considerations, such as debt-to-income ratios that demonstrate the prospective borrower's ability to uphold the mortgage payments. It is crucial to reference any contractual obligations and ensure the notification complies with relevant regulations, such as the Real Estate Settlement Procedures Act (RESPA). The lender's response time typically varies, but it may take around 30 days for approval of the assumption request.

Supporting documentation

Mortgage assumption notifications require supporting documentation to facilitate the transfer of responsibility for an existing mortgage loan to a new borrower. Relevant documents include the original mortgage agreement, which outlines terms and conditions from the lender, the formal assumption agreement that indicates the new borrower's acceptance of the mortgage obligations, and credit reports detailing the financial history of the new borrower to assess eligibility. Additionally, income verification documents, such as pay stubs or tax returns, are necessary to demonstrate financial stability. Other required materials might include a loan payoff statement, which provides the current balance of the mortgage, and any relevant disclosures stipulated by the lender to ensure transparency in the assumption process.

Contact information for follow-up

Mortgage assumption notification involves the process whereby a new borrower takes over the existing mortgage obligations from the original borrower. This typically occurs during a property transfer or sale, allowing the new owner to assume the remaining balance and terms of the loan. This process often requires contacting the mortgage lender, usually based in the United States, for specific guidelines and necessary documentation. Important details include the loan account number, which can be found on the mortgage statement, as well as the address of the property involved in the assumption. Follow-up communication, usually via phone or email, is crucial for resolving any potential issues and ensuring a smooth transition, making accurate contact information essential for both parties involved.

Read Also: Our Mortgage lender's Blogs

Comments