Are you feeling a bit confused about civil liability insurance and what it entails? You're not alone; many find the terminology a bit tricky and the purpose even murkier. This insurance is designed to protect individuals and businesses from claims resulting from injuries and damages to others, and understanding it can save you a lot of headaches down the road. So, if you're ready to clarify your doubts and gain a better insight into this essential coverage, keep reading to discover more!

Image cover: Letter Template For Civil Liability Insurance Clarification

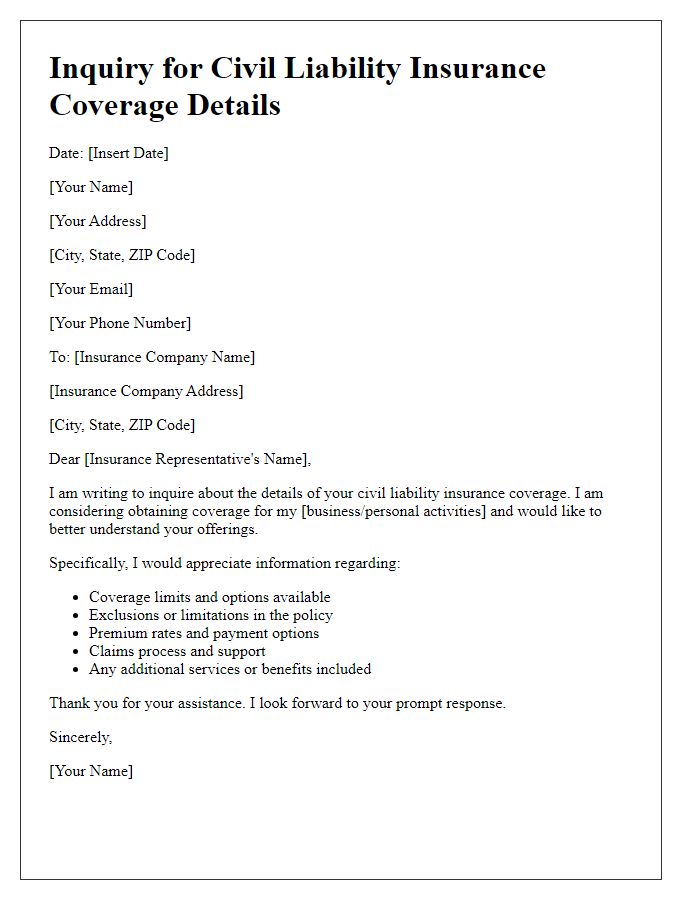

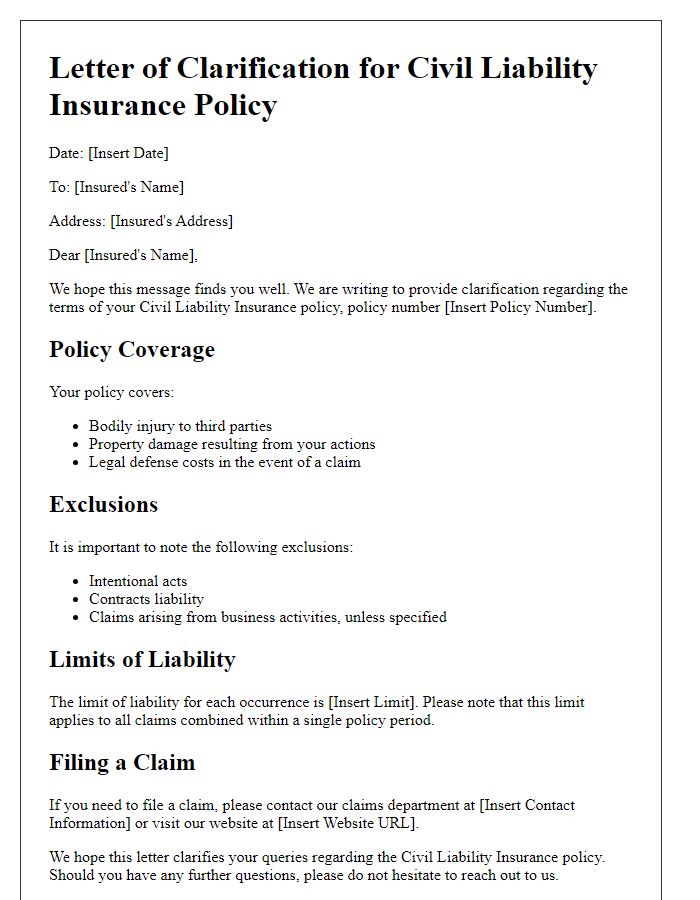

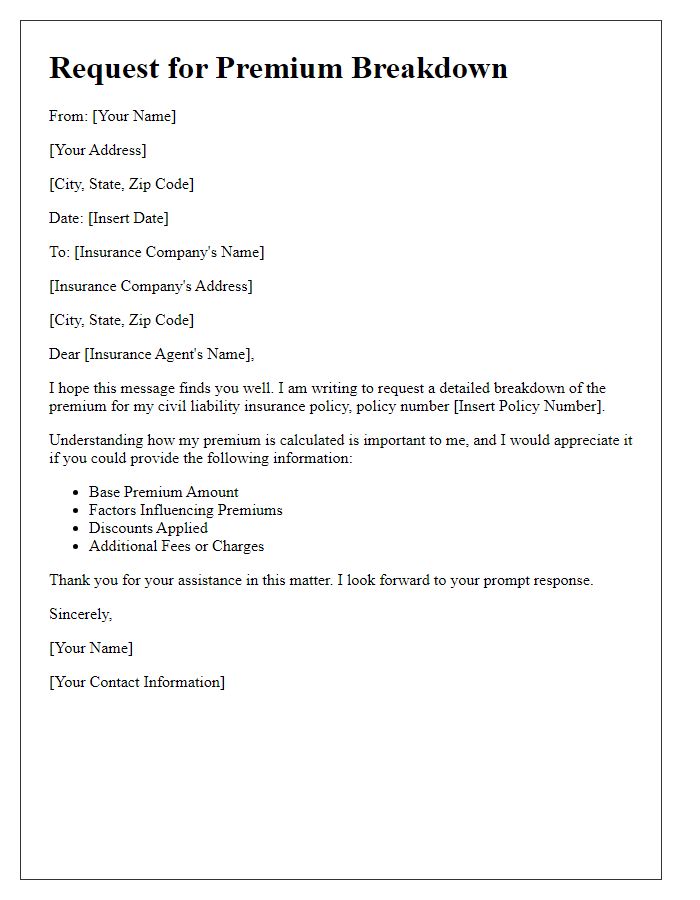

Letter Template For Civil Liability Insurance Clarification Samples

Policy Details and Coverage Limits

Civil liability insurance provides critical protection for individuals and businesses against various claims, including bodily injury and property damage. Policy details typically encompass essential features such as coverage limits, which define the maximum amount payable in the event of a claim. For instance, a standard policy may offer $1 million in coverage per occurrence with an aggregate limit of $3 million for the policy term. It is vital to understand specific exclusions within the policy, such as intentional acts, contractual liabilities, and certain professional services, which may not be covered. Additionally, it's important to note that endorsements can alter standard coverage, adding protections for particular risks or increasing limits for specific incidents. Underwriting requirements are also significant, as they ensure that the insured meets specific criteria, affecting the overall premium and coverage terms. Regular policy reviews can ensure that coverage aligns with evolving risks and business needs, safeguarding against unforeseen liabilities.

Terms and Exclusions Explanation

Civil liability insurance serves as a financial safety net for individuals and businesses, protecting against claims resulting from negligent acts that cause harm to third parties. This insurance often includes specific terms and exclusions that outline what is covered and what is not. Coverage typically includes bodily injury, property damage, and legal defense costs. However, exclusions may apply to intentional acts, criminal activities, and contractual liabilities. For instance, incidents occurring outside the policy period or in specific high-risk activities, such as motor racing or pollution-related events, may not be covered. Understanding these nuances is crucial to ensuring adequate protection in various situations.

Claim Process and Documentation Required

Civil liability insurance provides coverage for individuals or businesses against claims resulting from negligence or failure to perform a legal duty. The claim process typically involves multiple steps. First, policyholders must notify their insurance providers promptly, ideally within 48 hours of an incident leading to a claim. Essential documentation includes a completed claim form, detailed incident report outlining circumstances, photographs of any damages, witness statements, and any related police reports if applicable. Additionally, claimants must provide medical records or repair invoices if bodily injury or property damage is involved. Insurance companies may have specific forms and requirements, making it crucial for policyholders to consult their policy documentation or a claims adjuster for precise instructions. Each state may have different regulations affecting the claims process, adding further complexity to the procedure. Timely and accurate submission of all documents is critical to ensure a smooth claims experience and expedite potential reimbursements.

Contact Information for Further Inquiries

Civil liability insurance provides crucial protection against claims arising from personal injuries or property damage caused by negligence. Understanding policy coverage, limits, and exclusions is vital for all insured parties. Specific terms include liability limits, typically ranging from $100,000 to $1 million, and deductibles, which may vary. Important entities include insurance providers, such as Allianz and State Farm, known for comprehensive policies. Locations like California exhibit unique legal requirements influencing policy stipulations. For further inquiries regarding coverage details, claims process, or premium rates, contact your insurance representative or the company's customer service directly.

Legal and Compliance Obligations

Civil liability insurance protects individuals and businesses from claims alleging negligence or wrongful conduct that results in bodily injury or property damage. Understanding legal obligations is crucial, as policies often include specific conditions and exclusions. For instance, general liability policies may cover incidents occurring at business premises, while professional liability insurance addresses errors in services provided by professionals. Jurisdictions may impose different regulatory requirements, mandating minimum coverage amounts or specific terms related to employee injuries and contractual obligations. Compliance with local laws, like the Insurance Act or Consumer Protection Legislation, is essential to avoid legal penalties or insufficient protection during claims.

Read Also: Our Insurance policyholder's Blogs

Comments