Are you feeling a bit overwhelmed by the ins and outs of credit card grace periods? You're not alone! Understanding how these grace periods work can save you some serious cash and help you manage your finances more effectively. So, let's dive in and explore everything you need to know about maximizing your credit card benefitsâread on for valuable insights!

Image cover: Letter Template For Credit Card Grace Period Information

Letter Template For Credit Card Grace Period Information Samples

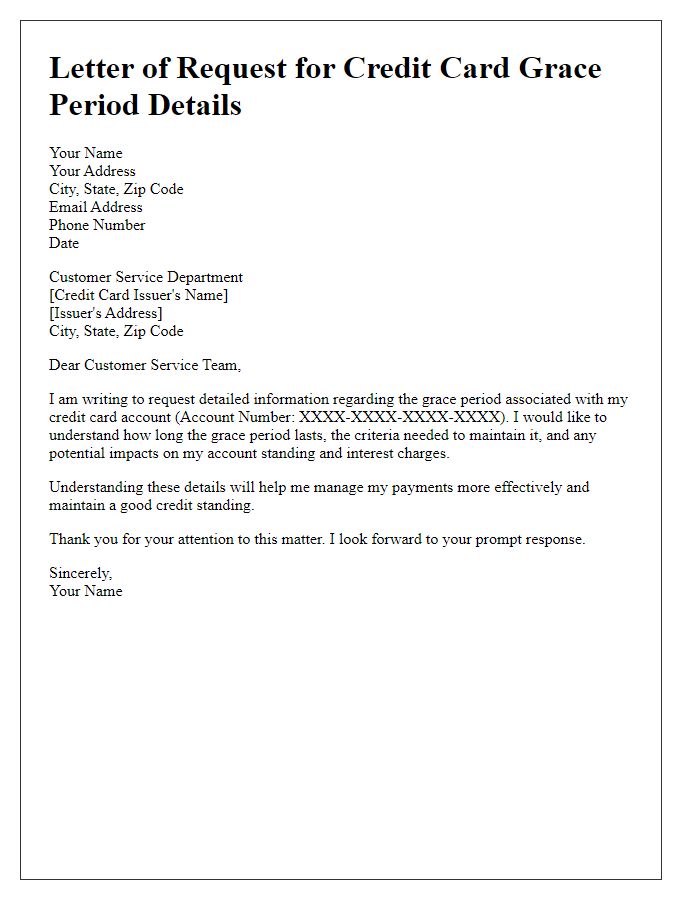

Cardholder's Personal Details

Credit card grace periods offer essential financial flexibility for cardholders. Typically lasting between 21 to 25 days, this grace period allows consumers to pay their monthly balance without incurring interest charges, provided the full amount is paid by the due date. Cardholders, such as individuals with the Chase Freedom card, can benefit from this feature by avoiding late fees when payments are made punctually. Notably, if a payment isn't received within this timeframe, substantial interest rates, sometimes exceeding 20%, may apply to the remaining balance. It is crucial to monitor statements and understand the specific terms that apply to each credit card, which can vary substantially among banks and account types.

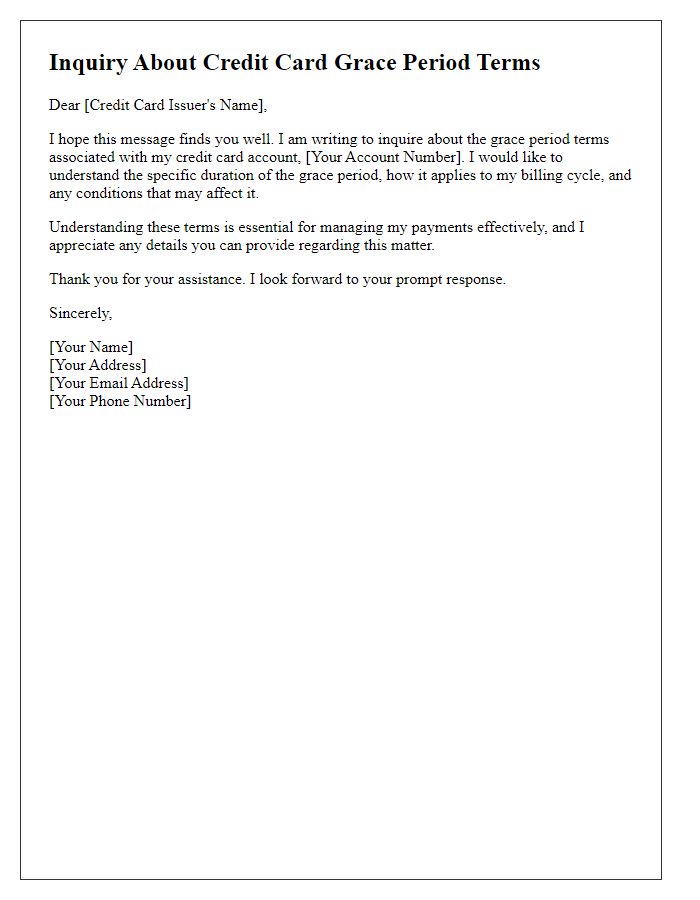

Grace Period Explanation

A credit card grace period typically refers to the time frame between the end of a billing cycle and the due date of the payment, allowing cardholders to avoid interest charges on new purchases if the previous balance is paid in full. Most credit card companies offer a grace period of approximately 21 to 25 days, depending on the specific card issuer such as Chase, American Express, or Capital One. During this period, if the total balance is cleared, no interest accrues on new purchases made within that cycle. However, if there is an existing balance carried over from prior months, interest may still apply even if new purchases are made within the grace period, highlighting the importance of timely payments. Cardholders should also be aware that any missed payments can result in the forfeiture of the grace period, causing immediate interest to accumulate on new purchases. Understanding these terms is crucial for effective credit management and avoiding unnecessary debt.

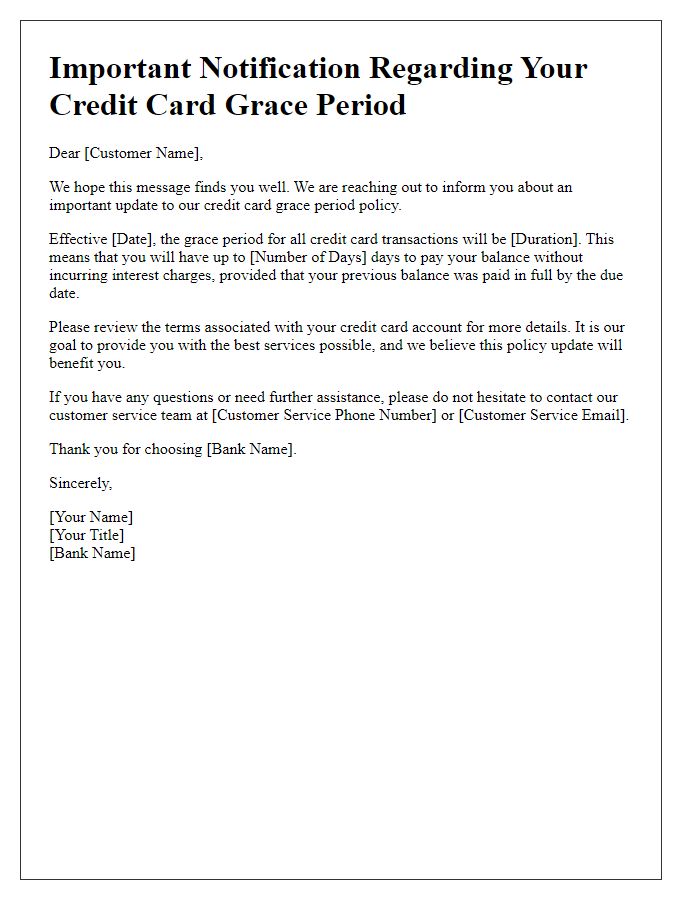

Payment Due Date Information

Credit card grace periods often allow cardholders to avoid interest charges on new purchases if the balance is paid in full by the due date. For example, typical grace periods range from 21 to 25 days after the billing cycle closes. Missing the payment due date, which varies by issuer and can fall on specific dates such as the 15th or 30th of each month, may result in interest accruing immediately on new transactions. Additionally, late payments may lead to penalties, increased interest rates, and a negative impact on the credit score, which is calculated by credit reporting agencies like FICO and Experian. Understanding these timelines is vital for maintaining financial health and leveraging the benefits offered by credit card companies.

Interest Calculation Method

The credit card grace period allows cardholders to avoid interest charges on new purchases if the balance is paid in full by the due date. Specifically, grace periods typically span between 21 to 25 days, depending on the issuer's policies. Purchases made during the billing cycle do not accrue interest if the entire balance from the previous cycle is paid by the due date. Cardholders should note that late payments can nullify the grace period benefits, causing interest to accrue immediately on new purchases. Additionally, cash advances often do not include a grace period and incur interest from the transaction date. Keeping track of the payment deadlines and understanding the specific grace period rules of the issuing bank can help manage credit card debt efficiently.

Contact Information for Inquiries

Credit card grace periods refer to the time frame in which cardholders can pay their balance without incurring interest charges. Typically, grace periods last between 21 to 25 days from the end of a billing cycle. Inquiries about specific grace periods for different credit cards can be directed to customer service representatives at banks, such as JPMorgan Chase or Bank of America. Contact numbers for these institutions, often found on their official websites or printed on credit card statements, provide direct access to assistance. Information may also be available via online banking platforms or mobile applications, which offer detailed insights into billing cycles and payment due dates. Understanding these elements is crucial for maintaining financial health and avoiding unnecessary interest fees.

Read Also: Our Credit card company's Blogs

Comments