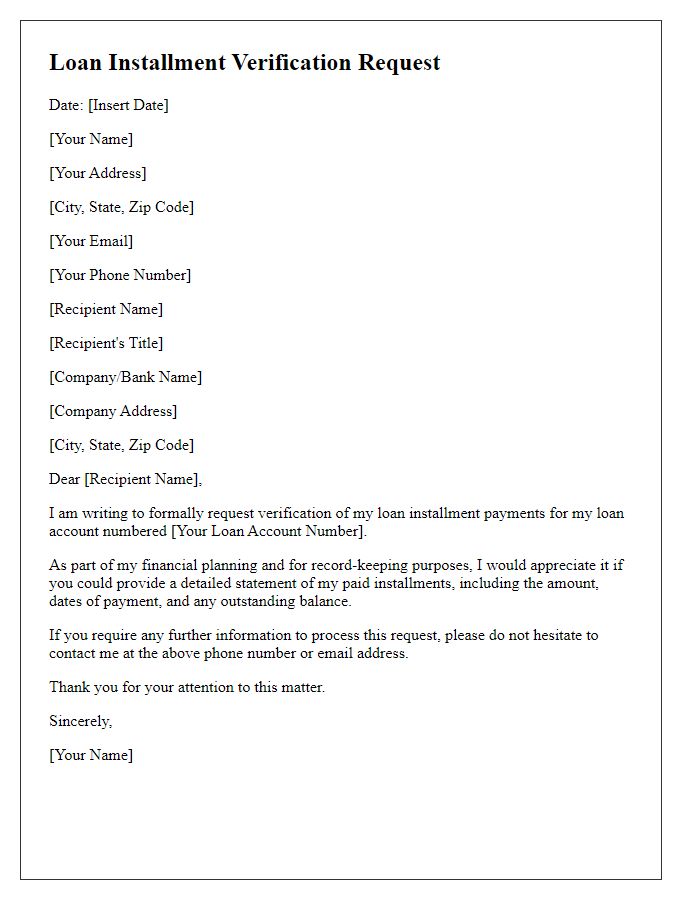

Hey there! If you're looking to verify your loan payment schedule, crafting a clear and concise letter is essential. This letter serves as a formal request to confirm your payment details, ensuring that both you and the lender are on the same page. Want to learn how to create an effective loan payment verification letter? Let's dive into the specifics!

Image cover: Letter Template For Verifying Loan Payment Schedule

Letter Template For Verifying Loan Payment Schedule Samples

Borrower's details

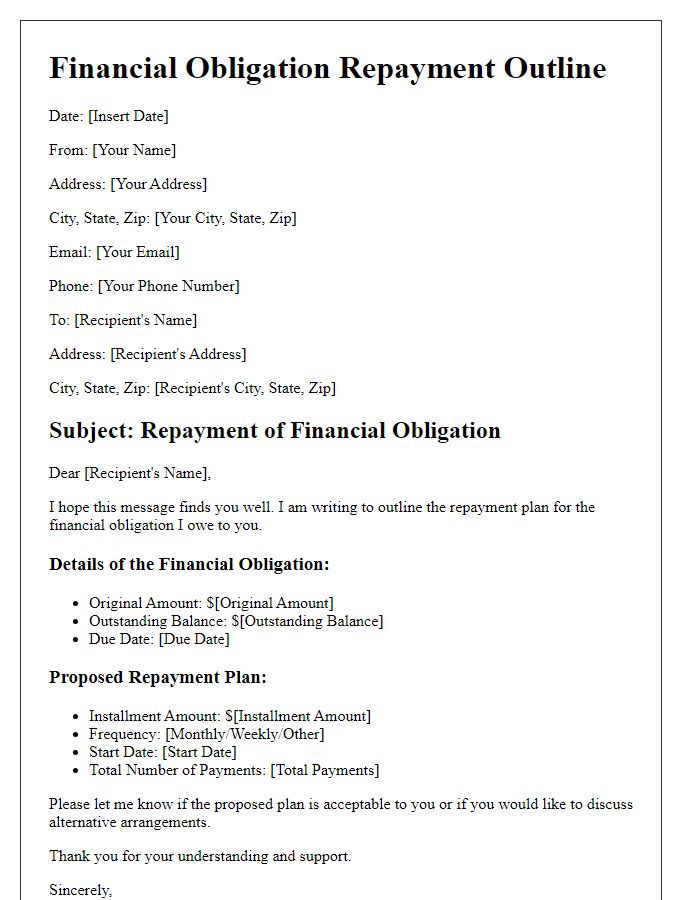

The loan payment schedule verification process involves essential details regarding the borrower's identity and financial commitment. The borrower's name, which identifies the individual responsible for the loan, typically includes their first name and last name. Additionally, the borrower's address, including street name, city, state, and zip code (for example, 123 Main Street, Springfield, IL, 62701), is mandatory for accurate identification. The loan account number serves as a unique identifier for the borrower's financial obligation, linking them to their specific loan details. Loan details encompass the original loan amount, the interest rate (often expressed as an APR), the loan term, and the payment frequency (such as monthly or bi-weekly). Confirming these details ensures that both borrowers and lenders maintain transparent and accountable financial practices.

Lender's contact information

Lender's contact information typically includes essential details such as the company's name, physical address, phone number, email address, and any applicable website URL. This information is crucial for borrowers to communicate effectively with their lender regarding inquiries or concerns. The lender's name should be clearly stated, followed by a full address including street name, city, state, and postal code. A direct phone number ensures quick access for any queries, while an email address allows for written correspondence. Additionally, the company's website can serve as a resource for information on services, payment portals, and customer support options, making it easier for borrowers to stay informed about their loan payment schedule.

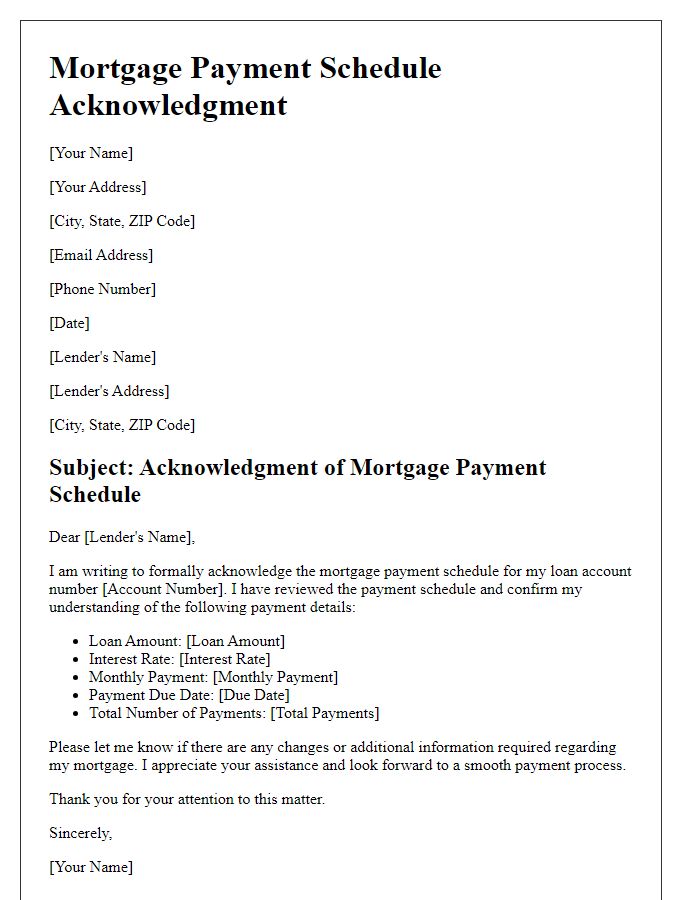

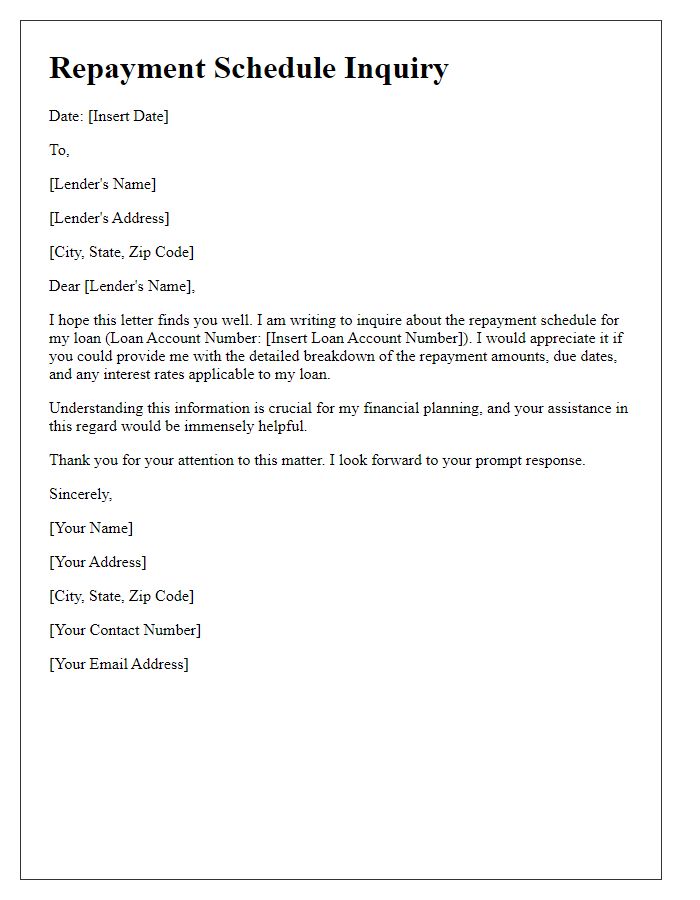

Loan account number

Loan account verification ensures accurate tracking of scheduled payments. Loan Account Number serves as the unique identifier, linking borrowers to their respective loan agreements. Monthly installments, calculated based on principal amount, interest rate, and loan term, typically vary among different loan types -- personal, auto, or mortgage loans. Financial institutions, such as banks or credit unions, maintain detailed schedules outlining due dates and amounts. Timely payments are crucial to avoid penalties and maintain a positive credit score, affecting future borrowing capabilities. Compliance with the established schedule fosters a responsible borrowing relationship.

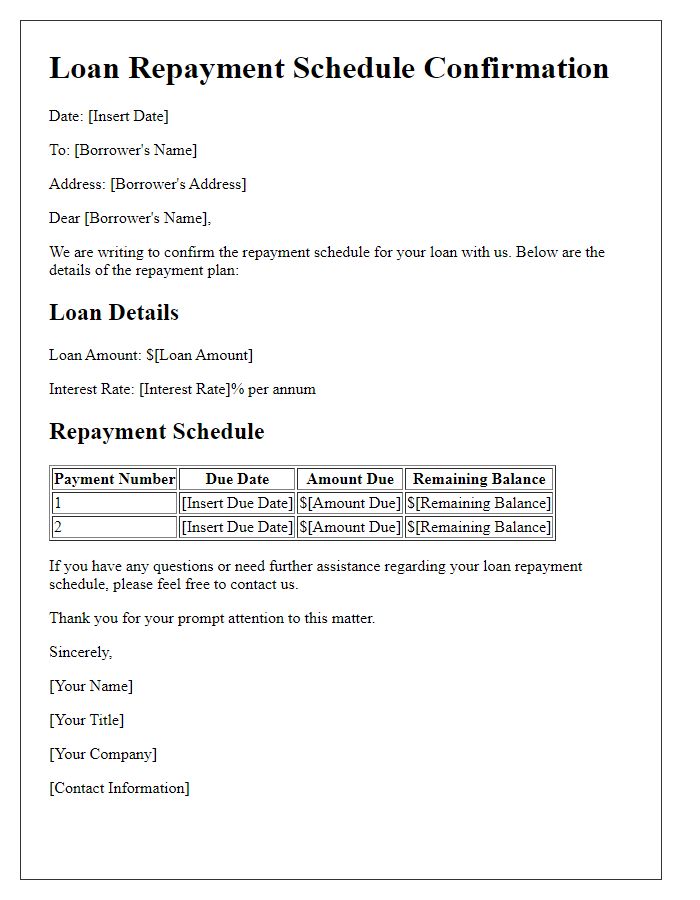

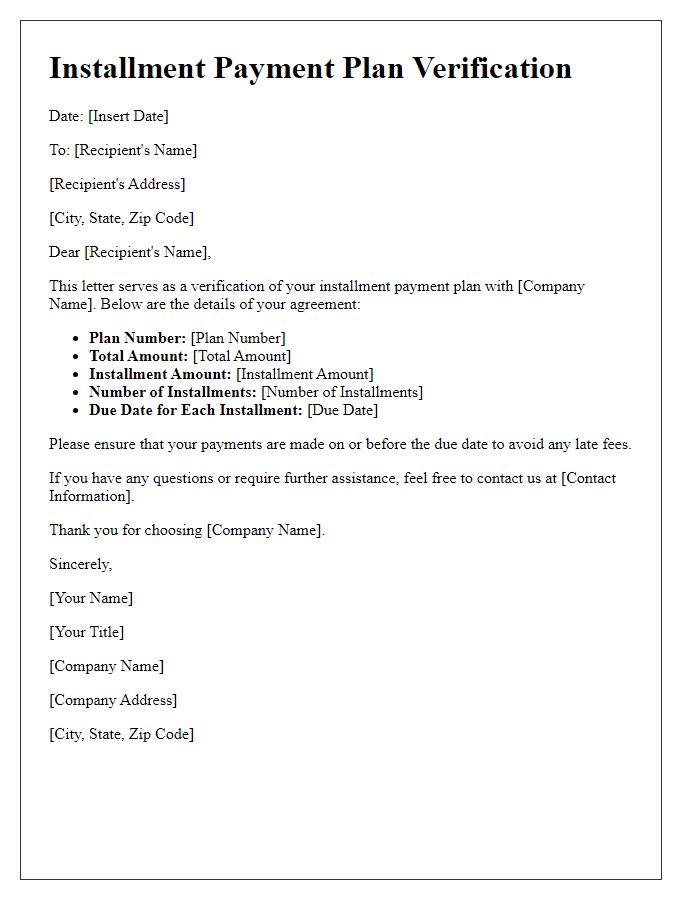

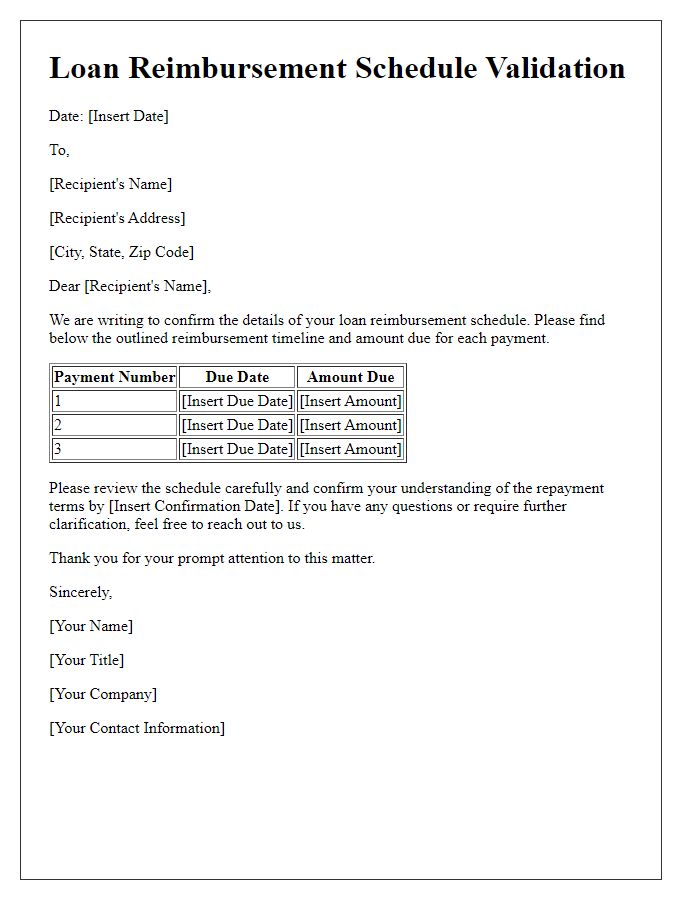

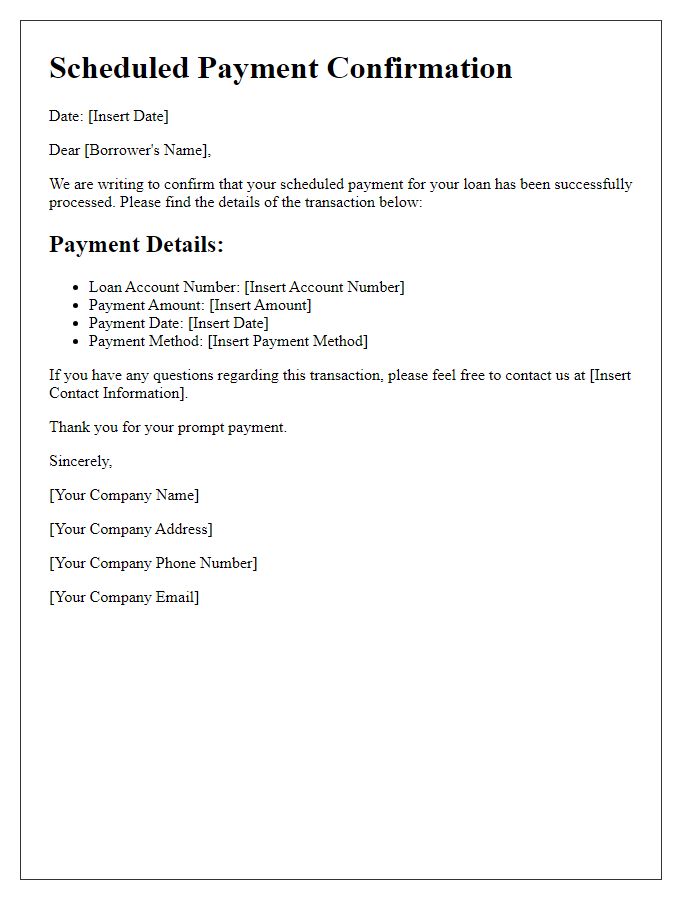

Payment schedule breakdown

A clear payment schedule breakdown is essential for managing loan repayments effectively. The structure typically includes the loan amount (e.g., $10,000), interest rate (e.g., 5% annual), loan term (e.g., 3 years), and the payment frequency (e.g., monthly). Each installment comprises a principal repayment portion and an interest portion, calculated based on the remaining loan balance. For instance, the first payment due date might be January 1, 2024, with monthly payments of approximately $299.71 for 36 months. Additionally, the schedule often details total interest paid over the life of the loan (e.g., $792.56), providing borrowers with a comprehensive view of their financial commitments. Tracking these payments helps maintain punctuality and avoid penalties.

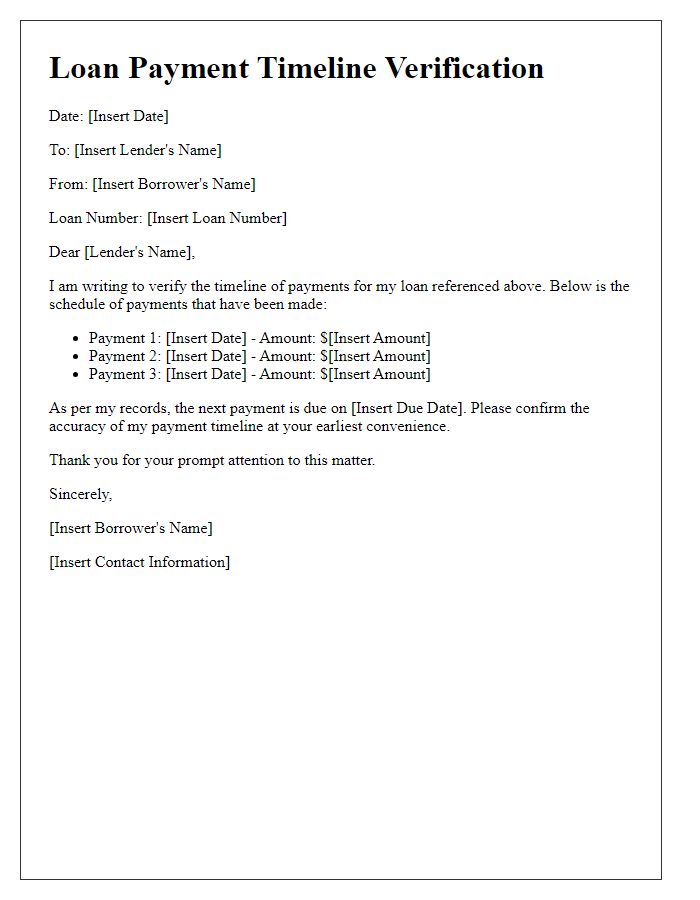

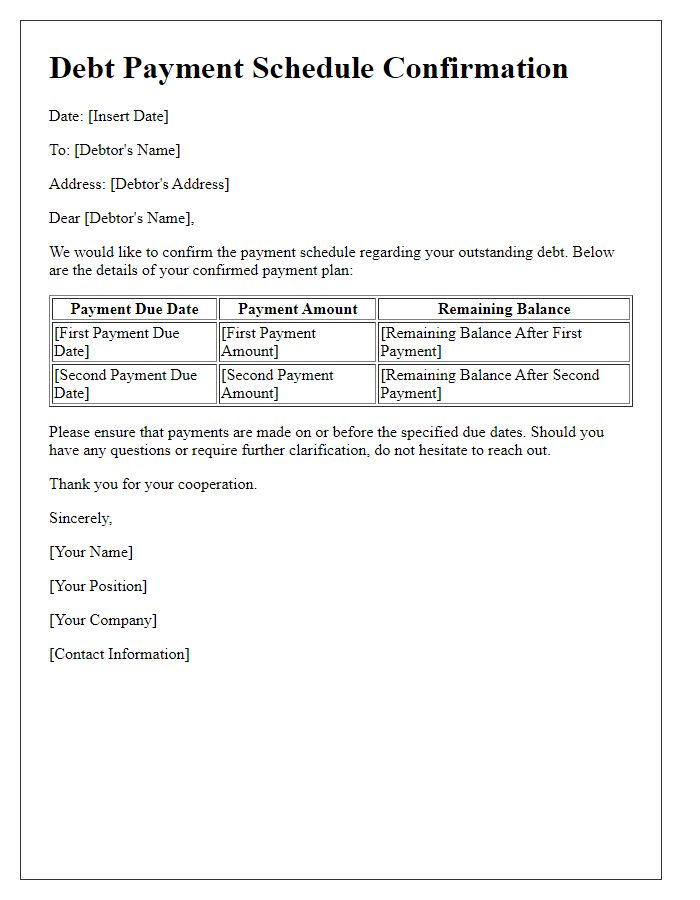

Confirmation statement

Loan payment schedules require meticulous tracking to maintain accurate financial records. A confirmation statement outlines specific payment amounts, due dates, and total loan balances, ensuring transparency between the lender and borrower. The statement often includes crucial details such as the loan origination date, interest rate (ranging typically from 3% to 7% annually), and potential fees for late payments, which can reach up to $50. Additionally, it is important that this documentation reflects remaining principal balances, early payment incentives, and the overall repayment term, often 15 to 30 years. Maintaining a clear understanding of the loan payment schedule minimizes misunderstandings and fosters healthy financial relationships.

Read Also: Our Borrower's Blogs

Comments