Are you ready to take the exciting leap into homeownership? Securing a mortgage can feel overwhelming, but having the right documentation is key to a smooth approval process. From your income verification to your credit history, knowing what to gather can save you time and stress. Dive into our article for a comprehensive letter template that simplifies the documentation required for mortgage approval and sets you on the path to your dream home!

Image cover: Letter Template For Documentation Required For Mortgage Approval

Letter Template For Documentation Required For Mortgage Approval Samples

Comprehensive personal identification details

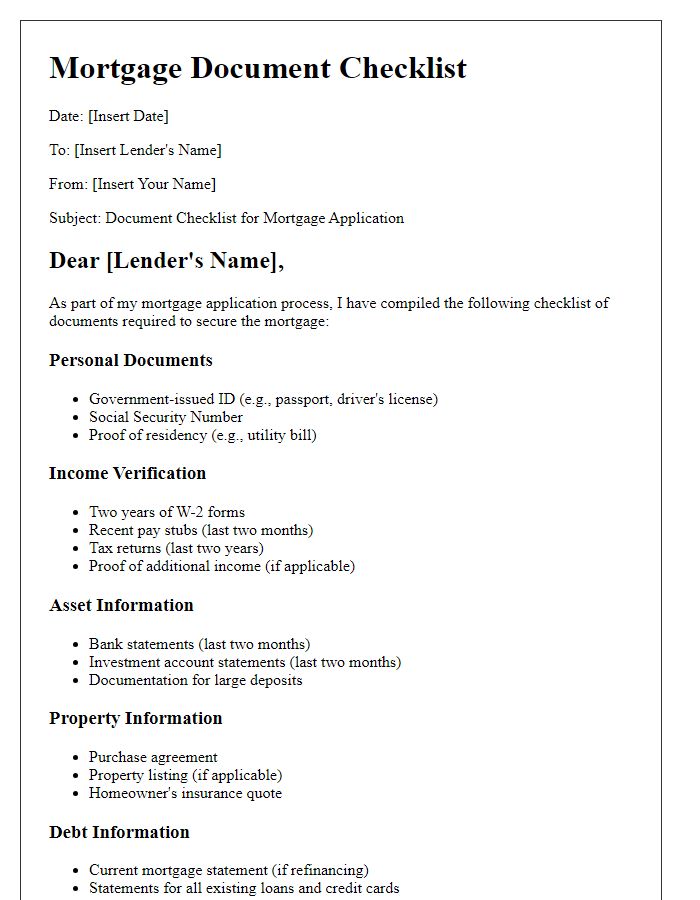

Comprehensive personal identification details are crucial for mortgage approval processes. Common documentation requirements include government-issued photo identification, such as a driver's license or passport, which verifies identity and residency. Social Security Number (SSN) documentation helps establish creditworthiness, ensuring lenders assess financial stability. Proof of residence, including utility bills or lease agreements, confirms the applicant's current living situation, while employment verification letters from employers substantiate income claims. Additionally, bank statements from the last few months offer insights into financial health, displaying spending habits and savings. Incorporating these elements accurately expedites the mortgage approval process, ensuring a smooth transaction for home buyers.

Detailed employment and income information

Detailed employment and income information is crucial for mortgage approval processes. Employment verification documents, such as recent pay stubs (typically covering the last 30 days), W-2 forms from the last two years, and a letter from an employer indicating job title, tenure, and salary, should be included. Self-employed individuals must provide additional documentation, such as tax returns (for the last two years) and profit and loss statements. Bank statements (covering the last two to three months) reflecting consistent income deposits will strengthen the application. Furthermore, any additional sources of income, such as bonuses, commissions, or rental income, should be documented with supporting statements or contracts. This comprehensive representation of financial stability assures lenders of the borrower's ability to meet mortgage obligations.

Complete list of assets and liabilities

A comprehensive list of assets and liabilities is crucial for mortgage approval, ensuring lenders assess financial stability. Assets include cash reserves, investments in stock markets (S&P 500, NASDAQ), real estate holdings (primary residence, rental properties), retirement accounts (401(k), IRA), and personal property (vehicles, jewelry). Liabilities encompass outstanding debts such as mortgage balances (current loan amounts), credit card debts (monthly payment totals), student loans (remaining balance, interest rates), and any personal loans. Providing accurate documentation for each category improves the chances of obtaining favorable mortgage terms and demonstrates fiscal responsibility. Include supporting documents, such as bank statements, tax returns, and credit reports, to substantiate financial claims.

Explicit request for specific documentation

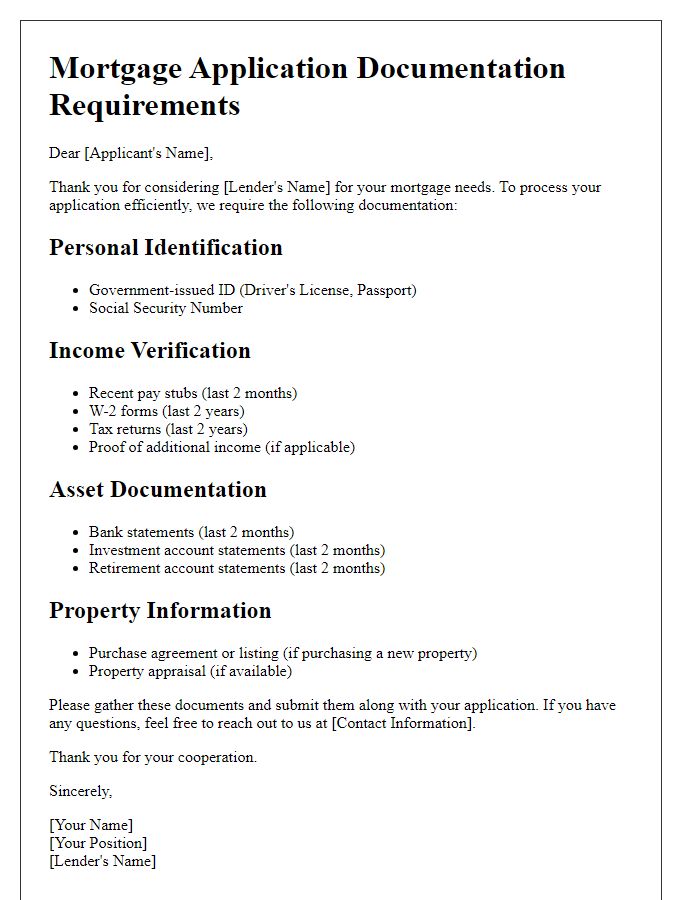

Mortgage approval requires comprehensive documentation that verifies the borrower's financial stability and creditworthiness. Essential documents include recent pay stubs (typically covering the last 30 days), W-2 forms, and tax returns (usually for the past two years). Lenders also typically request bank statements (at least two months' worth) to assess savings and checking account balances. Proof of assets, such as investment statements or retirement accounts, is necessary to demonstrate additional financial resources. Documentation of any outstanding debts, including credit card statements and any installment loans, helps assess the debt-to-income ratio. Borrowers may also be asked to provide a list of employment history covering the last two years, as well as identification verification, which could include a government-issued photo ID or Social Security card. Each document contributes significantly to the lender's decision-making process.

Clear deadline for submission

Mortgage approval requires specific documentation to ensure eligibility and financial stability. Key documents include proof of income, such as recent pay stubs (typically covering the last 30 days), W-2 forms from the previous two years, and tax returns for the last two years. Borrowers must also provide bank statements (last two months) to verify available funds for the down payment and closing costs. Employment verification letters from employers, detailing job position and salary, can enhance the application. Identification documents, including a government-issued photo ID and Social Security card, are necessary for identity verification. A clear deadline for submission, often set within 30 days of the initial application date, ensures timely processing of the mortgage application.

Read Also: Our Real estate firm's Blogs

Comments