Are you considering expanding your agricultural venture or starting a new project in your rural community? Obtaining a rural development loan can open up a world of opportunities to enhance your livelihood and support local growth. With flexible terms and funding options tailored for rural initiatives, these loans are designed to empower you and your neighbors. Ready to dive deeper into how a rural development loan can benefit your aspirations? Read on!

Image cover: Letter Template For Rural Development Loan

Letter Template For Rural Development Loan Samples

Applicant Information

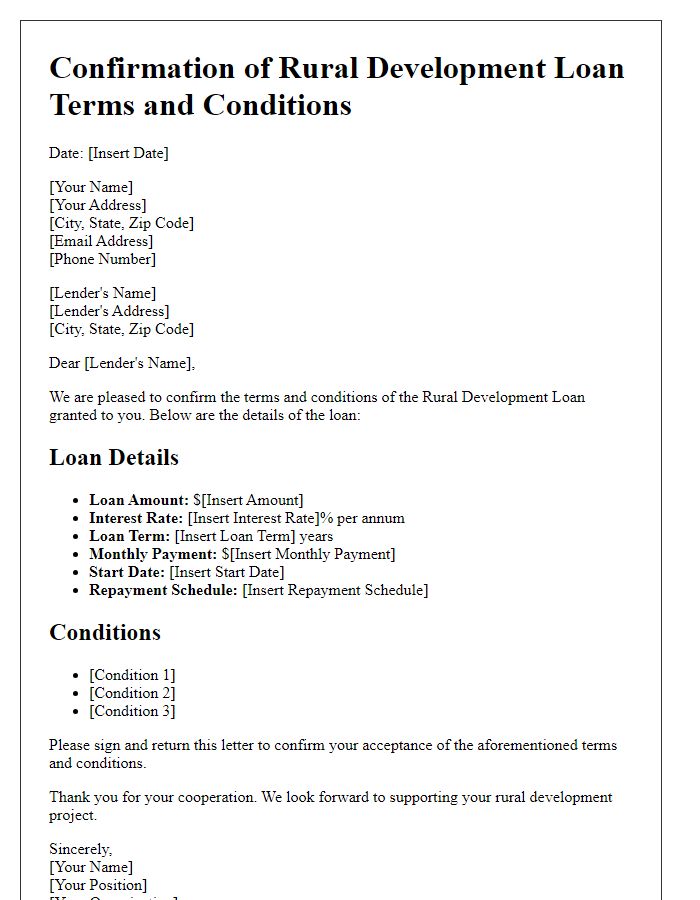

Rural development loans aim to provide financial assistance to applicants seeking to improve their rural properties, such as farms or homesteads. The applicant, typically a resident of areas designated as rural by the United States Department of Agriculture (USDA), submits detailed personal information including name, address, and contact number. This information is crucial for identifying eligibility for programs like the USDA Rural Development Guaranteed Housing Loan. Additionally, applicants must include financial details, such as income sources, debts, and credit history, to assess their ability to repay the loan. Supporting documents may also involve tax returns and asset declarations, which play a vital role in the approval process.

Loan Purpose and Description

A rural development loan facilitates various purposes aimed at enhancing community welfare in underserved areas. These loans support projects such as agricultural improvements, including modern irrigation systems, innovative crop techniques, and livestock enhancements tailored for farms in rural regions. Funding may also be allocated for infrastructure development, such as road construction, which connects isolated communities to commercial hubs, promoting economic growth. Additionally, the loans can assist in establishing small enterprises, including local markets that enhance food accessibility and job opportunities. Community engagement and sustainable practices are typically emphasized, fostering long-term benefits for residents and their environments.

Financial Need and Plan

In rural communities across the United States, access to financial resources remains a significant challenge due to limited local banking institutions. A rural development loan aims to address these financial gaps by providing necessary funding for essential projects such as agricultural expansion, infrastructure development, and housing improvements. Approximately 54 million people reside in rural areas, making it crucial to establish effective financial plans that cater to their unique needs. A detailed financial plan can outline specific funding requirements, such as property acquisition costs averaging $120,000 in rural settings, operational expenses, and potential job creation through business development initiatives. By securing a rural development loan, communities can empower local entrepreneurs, enhance agricultural productivity, and improve the overall living standards of residents in regions affected by economic stagnation and demographic shifts.

Community Impact and Benefits

Rural development loans significantly boost economic growth in underserved areas, fostering sustainable communities through improved infrastructure and access to essential services. These loans enable projects such as broadband cable installation, enhancing connectivity for rural households with populations often fewer than 2,500, ensuring residents can participate in the digital economy. Agriculture also benefits; investments in modern equipment increase crop yields by up to 30%, supporting food security. Community centers funded by such loans provide educational programs, serving hundreds of families and promoting skills development. Additionally, access to affordable housing initiatives positively impacts health outcomes and reduces poverty levels, contributing to overall social stability and resilience.

Supporting Documentation and Credentials

Rural development loans, often provided through the United States Department of Agriculture (USDA), require comprehensive supporting documentation to ensure eligibility and proper assessment. Essential documents include proof of income such as pay stubs or tax returns, detailing annual earnings, typically for the last two years. Credit reports from major bureaus like Equifax or Experian, showcasing credit history and scores, are crucial for assessing financial responsibility. Additionally, personal identification like government-issued IDs (driver's license or passport) must confirm identity and residency, often within designated rural areas. Property documentation, such as land surveys or titles, proves intended use, while detailed project plans outline proposed development, including budgets and timelines. Compliance with local regulations and zoning laws from municipal offices also strengthens the application. Lastly, letters of recommendation from community leaders or previous lenders may further validate the applicant's credibility and commitment to rural empowerment.

Read Also: Our Loan applicant's Blogs

Comments