Understanding negative amortization can be a bit perplexing, but it's essential for making informed financial decisions. Essentially, negative amortization occurs when your loan payments are lower than the interest charged, causing your loan balance to increase over time. This can lead to financial strain if not managed carefully, especially for homeowners or borrowers. Curious to learn more about how negative amortization impacts your finances? Dive into the details below!

Image cover: Letter Template For Negative Amortization Explanation

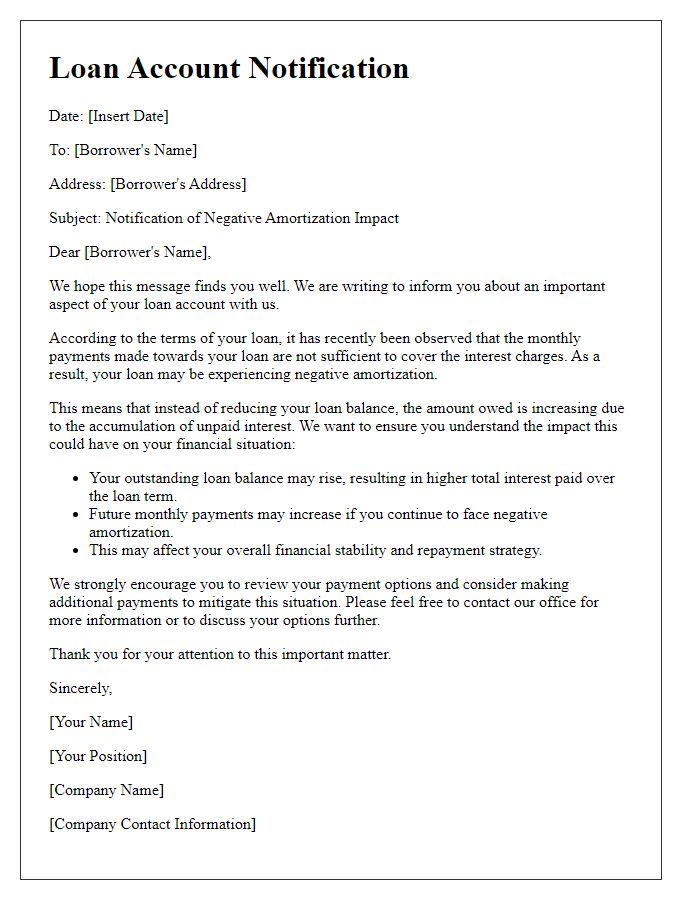

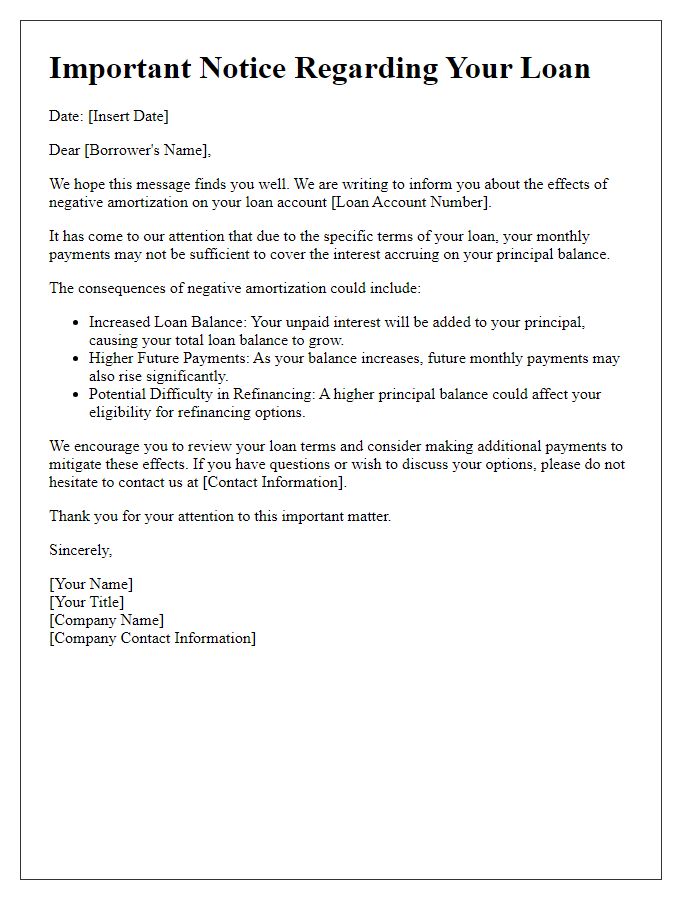

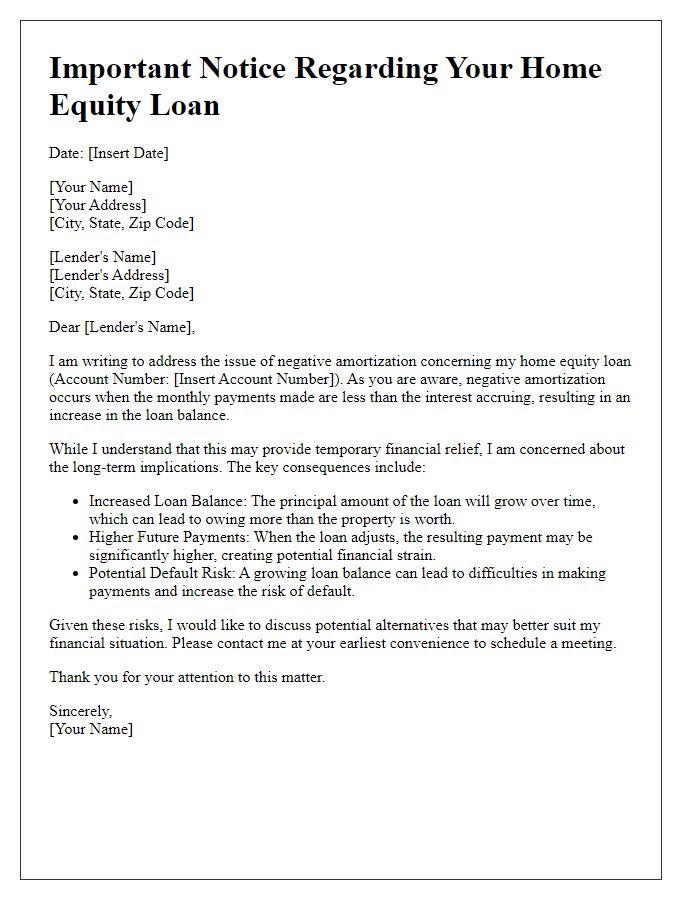

Letter Template For Negative Amortization Explanation Samples

Clear definition of negative amortization.

Negative amortization refers to a financial situation in which the outstanding balance of a loan increases over time, despite regular monthly payments being made. This can occur when the monthly payments are insufficient to cover the interest charged on the loan, leading to a growing principal balance. Typically associated with certain types of adjustable-rate mortgages (ARMs) or loans with deferred interest options, negative amortization can result in a borrower owing more than the original loan amount. This condition poses significant risks, especially if property values decline or if borrowers experience financial difficulties, potentially leading to foreclosure or increased debt burden. Understanding this concept is critical for borrowers to make informed decisions about their mortgage options and to manage their financial future effectively.

Detailed explanation of causes and implications.

Negative amortization occurs when a borrower's monthly payments are insufficient to cover the interest accruing on a loan, resulting in an increase in the loan principal. This situation often arises in certain loan types, such as adjustable-rate mortgages (ARMs) or interest-only loans, especially during periods of economic downturn or rising interest rates. For instance, a borrower with a $300,000 loan at a 6% interest rate may only pay $1,500 monthly; however, if the interest accrues to $1,800, the outstanding balance can grow significantly, reaching $350,000 over time. The implications of negative amortization can be severe, potentially leading to an increased debt burden, a higher risk of default, and decreased equity in the property. Additionally, when the loan eventually requires full payments, borrowers may face financial strain due to an unexpected jump in monthly payments, making it challenging to maintain ownership of their asset, often located in volatile real estate markets such as Florida or California. Understanding these aspects is crucial for borrowers to make informed decisions regarding their financial futures and to seek alternatives, such as fixed-rate loans, to avoid pitfalls associated with negative amortization.

Itemized breakdown of current loan terms and future projections.

Negative amortization occurs when a loan's payments do not cover the interest due, leading to an increase in the total loan balance over time. Loan terms can vary significantly, but in a common scenario, a borrower may have an adjustable-rate mortgage with an initial interest rate of 3%, typically lasting for five years. During this period, monthly payments might be set at 2% of the loan balance, resulting in insufficient funds to cover accrued interest of approximately 4% annually. As a result, the outstanding principal may rise instead of decrease, potentially reaching alarming levels. For example, a $200,000 loan could increase to $220,000 within five years if these conditions persist. Projections indicate that after the initial fixed period, the rate may reset based on market conditions, often leading to higher payments once the borrower enters the amortization phase. Such financial trends necessitate careful budgeting and planning to avoid unexpected financial strain.

Repercussions on credit score and financial health.

Negative amortization occurs when monthly payments on a loan, such as an adjustable-rate mortgage, are insufficient to cover interest, causing the loan balance to increase over time. This situation often arises in scenarios where interest rates, like the average 5% in recent years, rise unexpectedly. As loan balances grow, borrowers may face significant long-term repercussions on credit scores, typically calculated by major credit bureaus like Experian, Equifax, or TransUnion. A declining credit score, reduced below the 620 threshold, can hinder access to future credit opportunities, impacting financial health and stability. Additionally, lenders may view negative amortization as a risk, potentially leading to higher interest rates for new loans or credit products. Understanding these implications is crucial for maintaining financial well-being.

Contact information for further assistance and resources.

Negative amortization occurs when loan payments do not cover the interest costs, leading to an increase in the outstanding principal balance. This situation often arises in adjustable-rate mortgages, particularly those with low initial rates, resulting in borrowers owing more than the original loan amount. In the United States, many homeowners faced negative amortization during economic downturns, particularly around the housing crisis of 2008. Commonly, loan specifics like payment schedules (usually set monthly) and interest rate adjustments (often annual) contribute to the complexity of negative amortization scenarios. Understanding these terms is crucial for borrowers to avoid financial pitfalls linked to escalating debt.

Read Also: Our Lender's Blogs

Comments