Are you considering a 401(k) rollover? Navigating the world of retirement savings can be a bit overwhelming, especially when it comes to understanding your options. Whether you're changing jobs or simply seeking better investment opportunities, knowing how to effectively roll over your 401(k) is essential for your financial future. Join me as we explore the ins and outs of 401(k) rollovers and discover strategies to optimize your retirement portfolio!

Image cover: Letter Template For 401K Rollover Advice

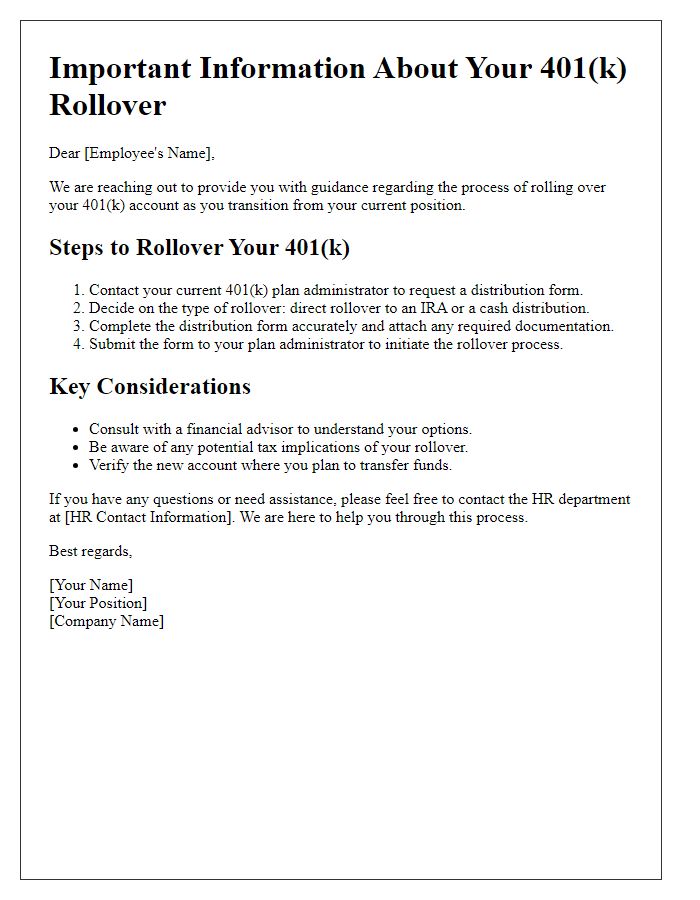

Letter Template For 401K Rollover Advice Samples

Personal and Account Information

Individuals may consider a 401(k) rollover to manage retirement savings more effectively. A 401(k) account, typically offered by employers, allows employees to save for retirement while benefiting from tax advantages. When transitioning between jobs, individuals can move funds to an IRA (Individual Retirement Account) or a new employer's 401(k) plan. Important factors include account balances, employer match policies, and investment options. Additionally, understanding tax implications during a rollover process is crucial. The timeline for processing these rollovers can vary, ranging from several days to weeks, depending on the financial institutions involved, making timely planning essential for maintaining investment growth.

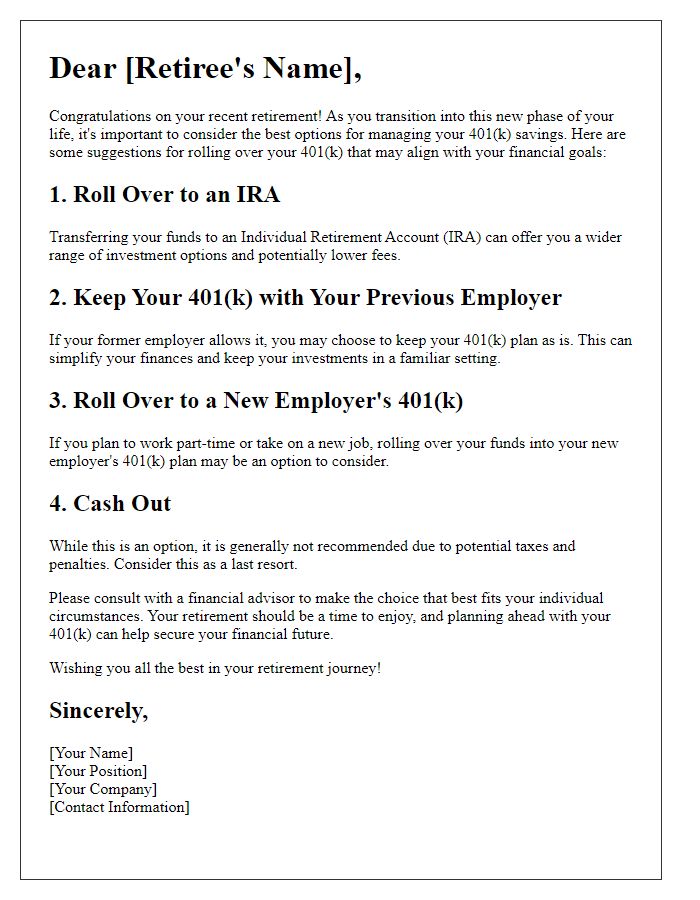

Rollover Options and Strategies

A 401(k) rollover provides individuals with the opportunity to transfer retirement savings from an employer-sponsored plan into an Individual Retirement Account (IRA) or another qualified plan. Factors such as age (above 59.5 years), tax implications, and investment options significantly influence rollover strategies. For example, transferring funds into a traditional IRA allows for tax-deferred growth while avoiding immediate tax liabilities. Conversely, rolling over to a Roth IRA triggers a taxable event but offers potential tax-free withdrawals in retirement. Financial institutions like Fidelity (a major player in retirement services) or Vanguard (known for low expense ratios) provide various investment options suitable for diverse risk tolerances, including index funds and ETFs. Consulting a financial advisor ensures that beneficiaries align their rollover strategy with long-term retirement goals, optimizing for factors such as fees, asset allocation, and future income needs.

Tax Implications and Considerations

When contemplating a 401(k) rollover, it's crucial to understand the tax implications associated with the transfer of retirement funds. A direct rollover, occurring when funds move directly from a 401(k) plan to an Individual Retirement Account (IRA), typically avoids taxation and penalties. The Internal Revenue Service (IRS) allows this method to maintain tax-deferred status, essential for long-term retirement planning. However, if a distribution is taken and subsequently deposited into an IRA, the IRS mandates withholding 20% for federal taxes, which can affect total retirement savings. Additionally, the age of the account holder plays a role; if under 59 1/2, there may be early withdrawal penalties. Thoroughly assessing options, including traditional versus Roth IRAs and their respective tax consequences, is advisable before proceeding with any rollover. Furthermore, understanding state tax regulations can provide additional insights into potential obligations during such transfers.

Compliance and Regulatory Guidelines

Navigating the process of a 401(k) rollover involves adhering to strict Compliance and Regulatory Guidelines set forth by the Employee Retirement Income Security Act (ERISA). Individuals must ensure that they are following specific protocols to maintain the tax-deferred status of their retirement funds during the rollover. In 2023, the IRS allows direct rollovers to Individual Retirement Accounts (IRAs), ensuring beneficiaries avoid potential tax penalties that can arise from cashing out. Failure to meet the 60-day rule for indirect rollovers can incur severe tax implications. Carefully reviewing the financial institution's policies, including any associated fees and investment options, is crucial to making informed decisions. Staying educated on potential changes to regulations, possibly influenced by future government policies, will better protect retirement savings.

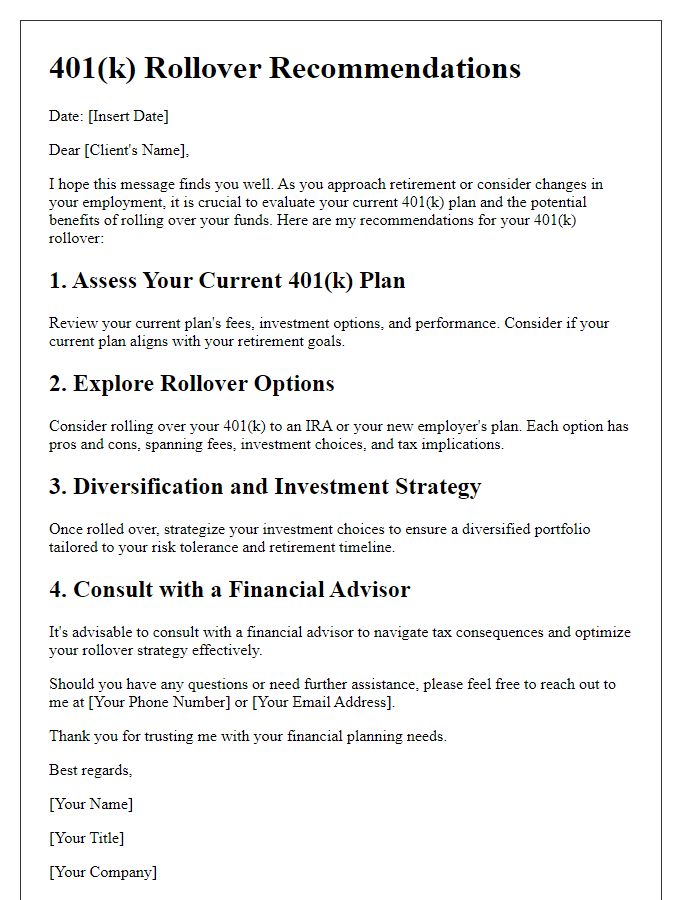

Financial Goals and Risk Assessment

A 401k rollover process can significantly impact an individual's financial goals and risk assessment strategy. Transitioning an employer-sponsored 401(k) plan, often valued in the tens of thousands of dollars, into an Individual Retirement Account (IRA) allows for broader investment choices, like mutual funds or ETFs, potentially improving long-term growth. It's crucial to assess personal risk tolerance, which can vary based on age, market experience, and overall financial situation. During this rollover, investors should consider factors like investment time horizon (typically between 10-30 years until retirement), expected returns, and volatility impacts. Understanding how different asset classes (stocks, bonds, and alternatives) behave during market fluctuations is vital for making informed decisions that align with retirement objectives, such as achieving a target retirement age (like 65 years) with sufficient liquidity and income generation potential.

Read Also: Our Financial consultancy's Blogs

Comments