When considering an adjustable mortgage loan, it's essential to understand both the potential benefits and risks involved. These loans can offer lower initial interest rates, which may help you save money in the early years of homeownership. However, as rates fluctuate, your monthly payments might increase, leading to budgetary challenges down the line. Curious to learn more about how an adjustable mortgage loan could fit into your financial plan? Keep reading to explore all the details!

Image cover: Letter Template For Adjustable Mortgage Loan Details

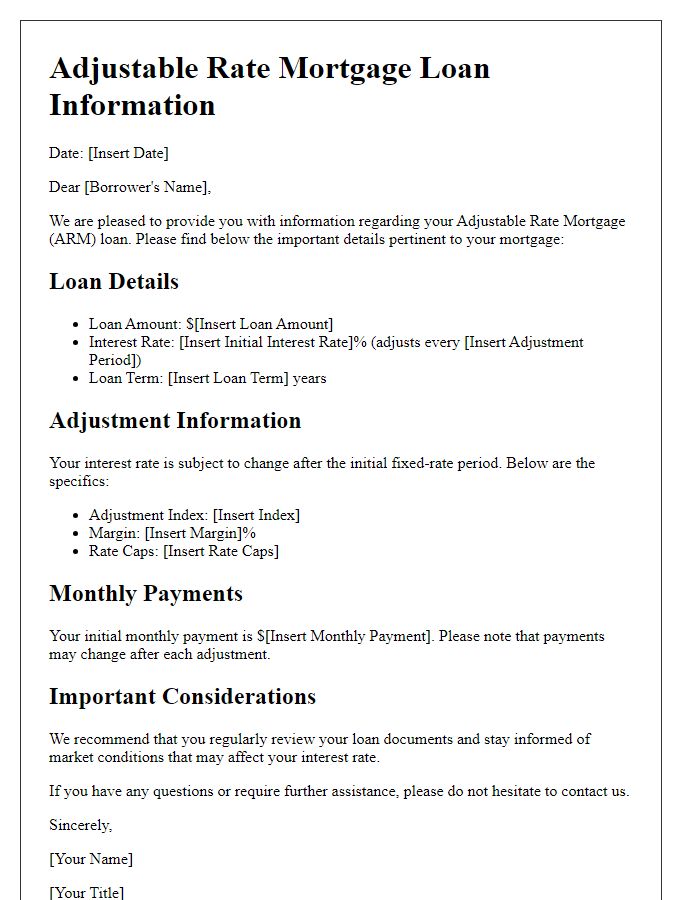

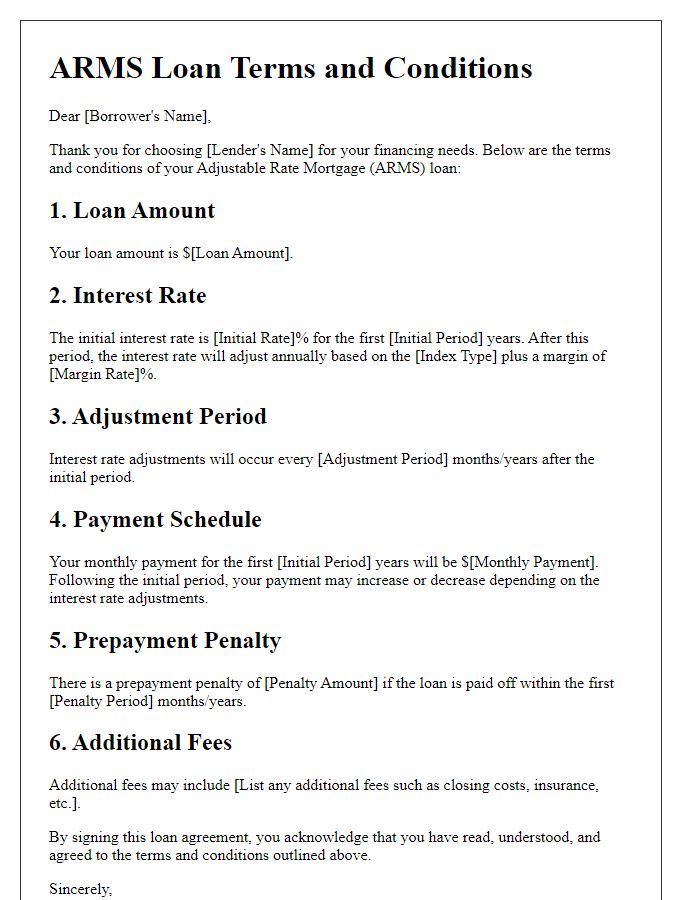

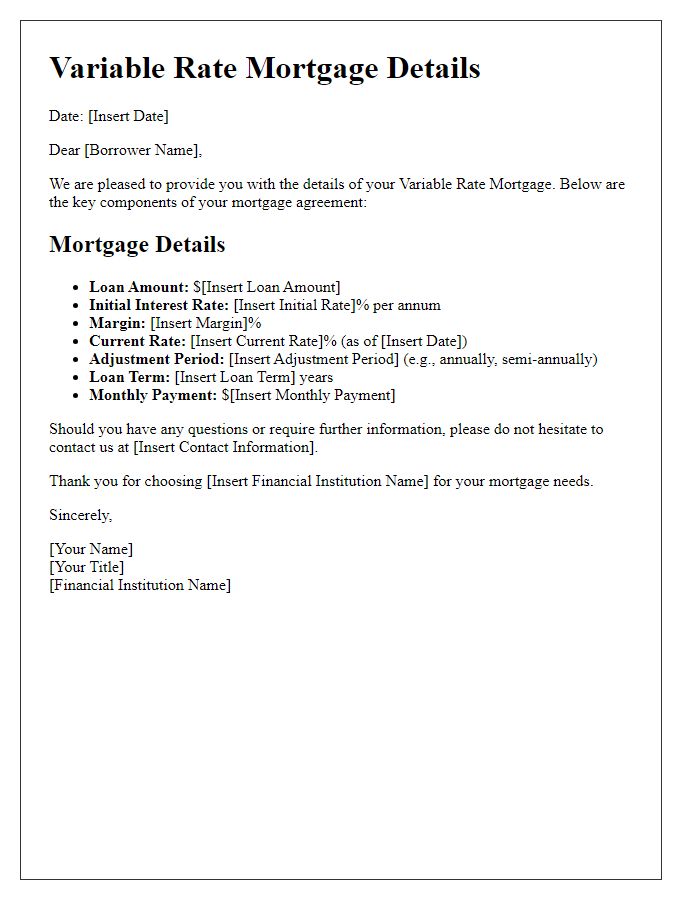

Letter Template For Adjustable Mortgage Loan Details Samples

Borrower's Name and Contact Information

Adjustable-rate mortgages (ARMs) can present various financial implications for borrowers, especially in fluctuating interest rate environments. Borrowers, typically individuals or joint applicants seeking home financing, must provide their full legal names and adequate contact information, including email addresses and phone numbers. These details facilitate communication with lenders, such as banks or mortgage companies, throughout the loan processing period. Key components of an adjustable-rate mortgage include the initial interest rate, which often remains fixed for a specific period (e.g., 5, 7, or 10 years), followed by adjustments based on market conditions. Consideration of potential rate caps and the index used (such as LIBOR or SOFR) is crucial in understanding how monthly payments may change over time, affecting the overall financial planning of the borrower.

Lender's Name and Contact Information

Adjustable-rate mortgage (ARM) loans offer borrowers a variable interest rate that can change periodically based on market conditions. Common lenders, such as Bank of America or Wells Fargo, provide detailed information regarding these loans. Typically, ARM loans feature an initial fixed-rate period lasting three, five, or seven years, after which the interest rate adjusts annually based on benchmarks like the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR). Borrowers should be aware of the potential for increased monthly payments when the interest rate resets. Important documents include the loan agreement and the Good Faith Estimate, which outlines projected costs. Contact information for lenders usually includes a local office address, phone numbers, and a dedicated website for inquiries, ensuring that borrowers can easily access assistance and further details about their loan options.

Loan Amount and Term Details

An adjustable-rate mortgage (ARM) typically features a loan amount that can vary based on the borrower's needs, often ranging from $100,000 to several million dollars. The term, or duration, of these loans commonly spans 15 to 30 years, affecting monthly payments and total interest paid. Initial rates are usually fixed for a specific period, like 5, 7, or 10 years, after which they adjust periodically based on market conditions. Rate adjustments are determined by a specific index, such as the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR), plus a margin defined by the lender. Borrowers should be aware that after the initial fixed period, interest rates can change, significantly impacting financial planning based on the adjustments.

Adjustable Rate Index and Margin

Adjustable-rate mortgages (ARMs) typically include a specific index used to determine interest rate fluctuations. Common indices for ARMs include the 1-Year Treasury Bill, the London Interbank Offered Rate (LIBOR), or the Cost of Funds Index (COFI). The margin, which is a fixed percentage added to the index, plays a crucial role in calculating the adjustable interest rate. For instance, if the chosen index is at 3% and the margin is set at 2%, the resulting interest rate for that adjustment period would be 5%. Borrowers should be aware of the adjustment frequency, which may occur annually or semiannually, as well as any annual or lifetime interest rate caps to mitigate potential payment increases. Understanding these details helps homeowners make informed financial decisions regarding their mortgage obligations.

Initial Interest Rate and Adjustment Frequency

Adjustable mortgage loans, particularly the commonly used 5/1 ARM (Adjustable Rate Mortgage), have specific details integral to their function. The initial interest rate, often significantly lower than fixed-rate mortgages, typically applies for the first five years. For example, an initial interest rate of 3.5% can substantially reduce monthly payments during this period. After this window, the loan adjusts annually based on the specified index, such as the 12-month London Interbank Offered Rate (LIBOR), plus a fixed margin. Adjustment frequency plays an essential role; in this case, the interest rate recalibrates every year, causing potential fluctuations in monthly payments. Borrowers must be aware of caps on adjustments, such as a maximum increase of 2% per adjustment period, as well as the lifetime cap, often set to prevent the interest rate from exceeding a designated upper limit, ensuring manageable payments even in fluctuating economic conditions.

Read Also: Our Loan provider's Blogs

Comments