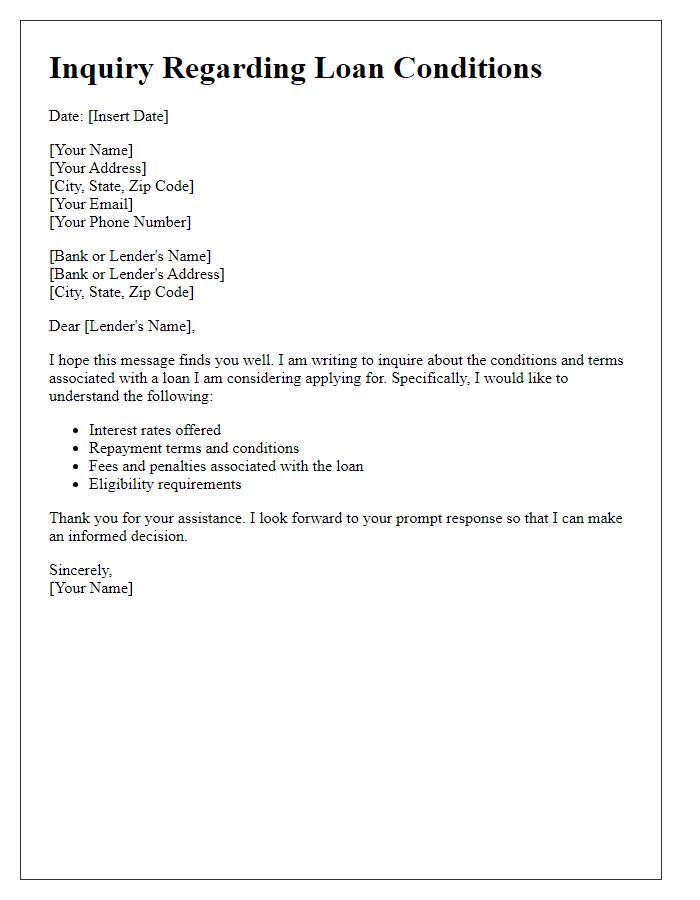

Are you navigating the complex world of loan terms and agreements? It's crucial to understand every detail before you commit, and a verification letter can be your best friend in this process. This letter not only clarifies the terms of your loan but also ensures that both you and your lender are on the same page. Ready to learn how to draft an effective verification letter? Keep reading to discover valuable insights!

Image cover: Letter Template For Verification Of Loan Terms

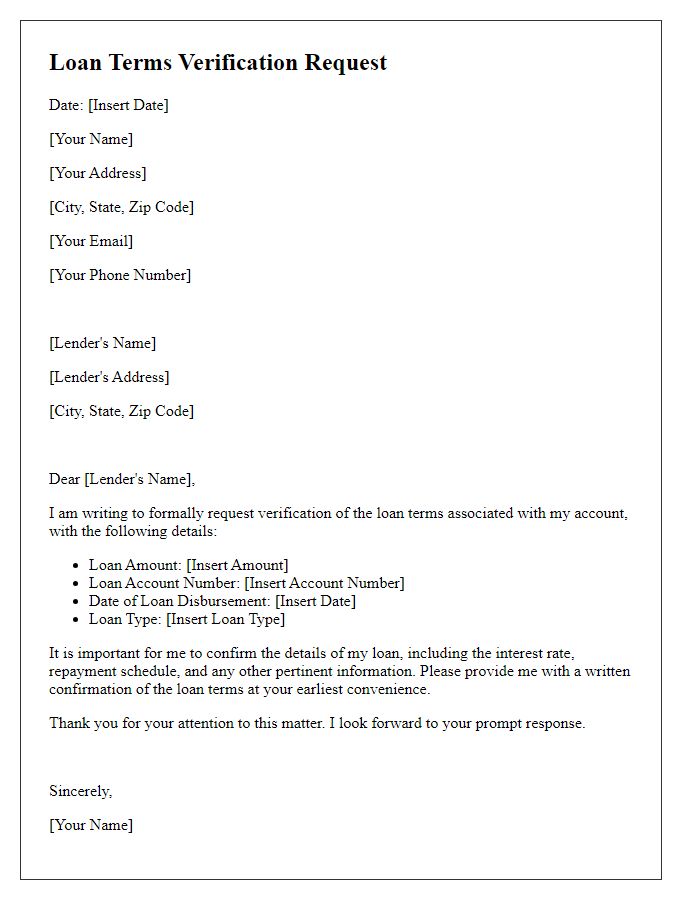

Letter Template For Verification Of Loan Terms Samples

Borrower and Lender Information

In the context of financial transactions, verifying loan terms is crucial for both borrowers and lenders. The borrower, typically an individual or entity seeking funds, must provide clear identification, such as a Social Security Number or Employer Identification Number, along with personal information, like full name, address, and contact details. Conversely, the lender, often a financial institution or private entity, should include its legal name, address, and relevant licensing information. Interest rates, repayment schedules, and loan amounts are essential elements in this verification process, influencing both parties' financial stability. Adherence to state regulations (such as truth in lending laws) ensures transparency and trust in this financial agreement. Accurate documentation can prevent future disputes over the loan's terms and conditions, ultimately safeguarding both parties involved in the transaction.

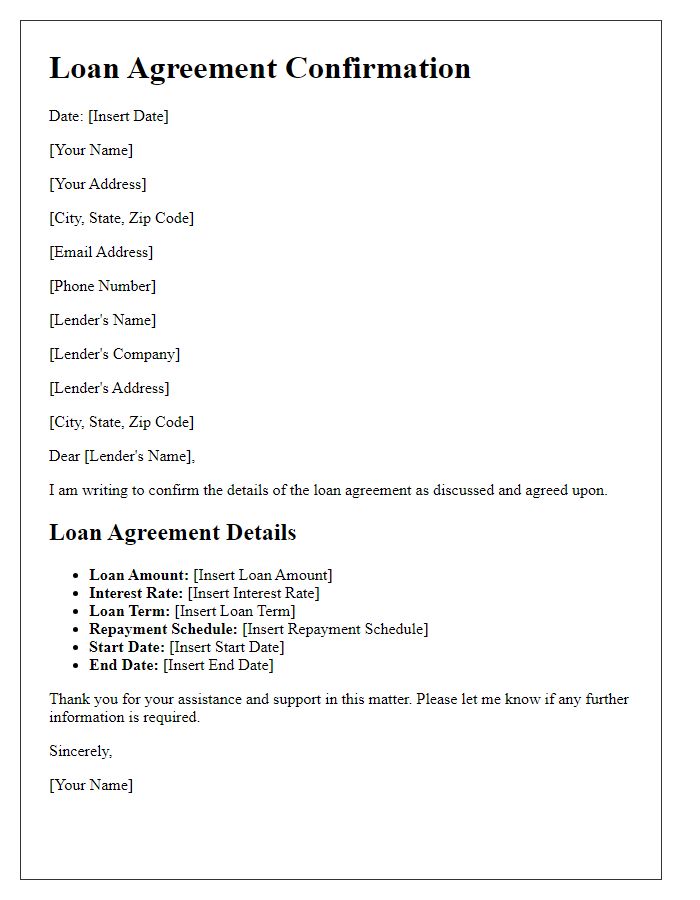

Loan Amount and Interest Rate

Loan verification communication can detail essential components such as principal amount and interest rate specifics. A typical personal loan may range from $1,000 to $50,000, often determined by individual creditworthiness. Standard interest rates in the United States can fluctuate between 5% to 36%, heavily influenced by factors like FICO scores (300 to 850 scale). For instance, a secured loan may offer lower rates, while unsecured loans might present higher rates. Furthermore, clarity on repayment terms is vital; typical durations may vary from 12 months to 60 months or longer, impacting the total repayment amount. Every detail contributes to understanding financial obligations and planning for future investments.

Repayment Schedule and Terms

Loan verification processes play a crucial role in financial institutions, like banks or credit unions, ensuring transparency and clarity in repayment schedules. A typical repayment schedule outlines the specific dates for monthly payments, often spanning a typical duration of 15 to 30 years depending on the loan type, including mortgages and personal loans. Loan terms refer to conditions such as interest rates, which can vary between fixed (remaining constant throughout the loan duration) and variable rates (changing periodically). Additional clauses might include prepayment penalties, affecting borrowers who wish to pay off loans early, and late payment fees, which apply if payments exceed a grace period, usually about 15 days. Understanding these elements is vital for borrowers to manage their finances effectively and avoid surprises.

Collateral or Security Details

Collateral verification in loan agreements is crucial for assessing risk. Common forms include real estate properties, vehicles, or financial assets. For instance, a house located in Los Angeles, valued at $500,000, could serve as collateral. Financial assets, like stocks from notable companies such as Apple or Tesla, offer liquidity and can be easily liquidated. Lenders conduct appraisal processes, often using licensed appraisers, to determine the market value. Borrowers must ensure all documentation, including titles and insurance policies, is accurate and up-to-date to facilitate a smooth verification process. Understanding these aspects is vital for both parties in a loan agreement.

Default and Penalty Clauses

Understanding loan terms is crucial for borrowers. Default clauses in loan agreements outline specific conditions that constitute a default, such as late payments exceeding 30 days or failure to comply with additional covenants. Penalty clauses, often including late fees or interest rate hikes, are applied when a borrower fails to meet the repayment schedule. These penalties can vary significantly by lender, with some imposing fees of 5% of the overdue amount. Documentation should specify the timeline for defaults and clearly communicate the financial consequences to ensure all parties are aware of their obligations. Legal frameworks, such as those found in the Uniform Commercial Code (UCC) in the United States, govern these agreements, emphasizing the importance of understanding local regulations.

Read Also: Our Loan applicant's Blogs

Comments