Welcome to our comprehensive guide on audit methodology! If you're curious about the various approaches and techniques that auditors use to ensure financial statements are accurate and reliable, you're in the right place. From risk assessment to evidence gathering, we'll break down each step of the process in a way that's easy to understand. So, grab a cup of coffee and dive in to learn more about the intricacies of audit methodology!

Image cover: Letter Template For Audit Methodology Explanation

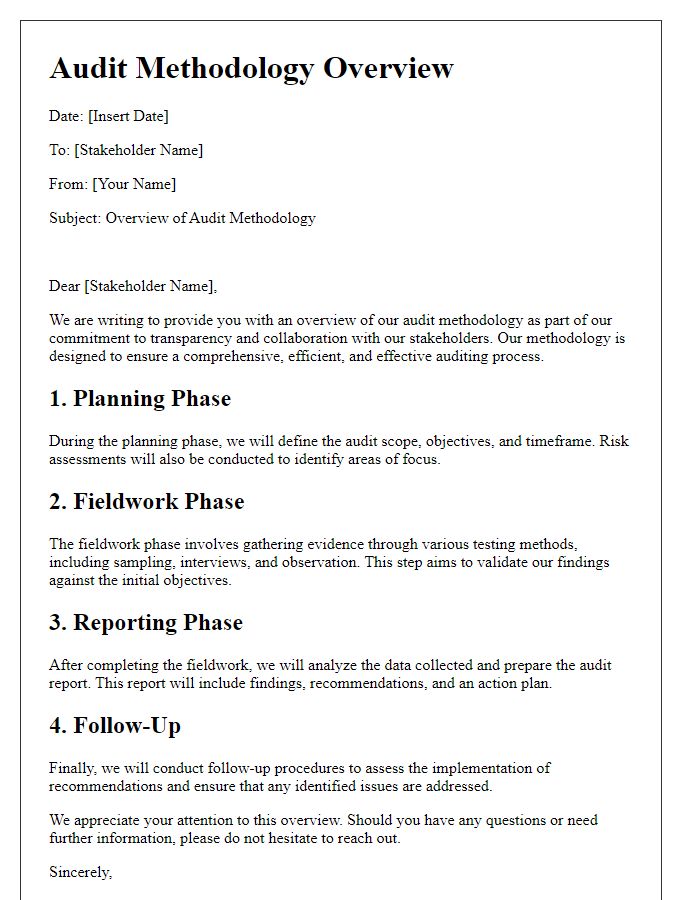

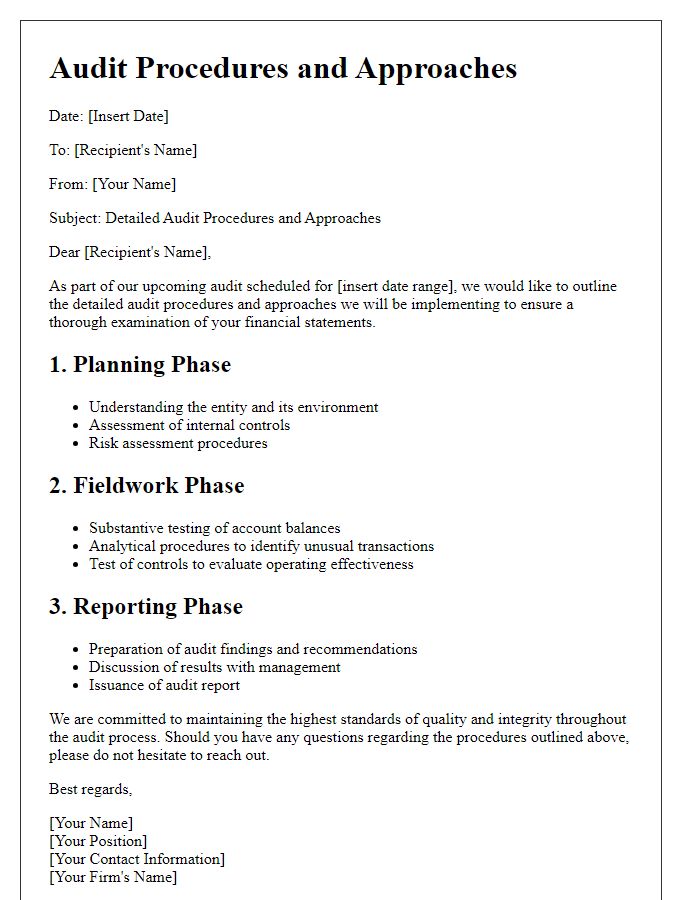

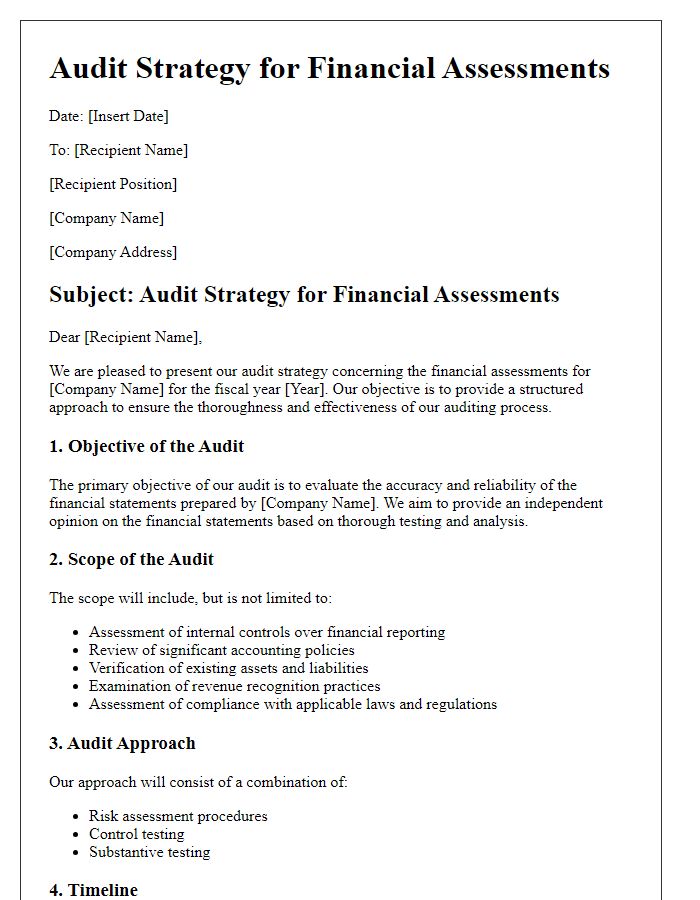

Letter Template For Audit Methodology Explanation Samples

Objective clarity and scope definition

The audit methodology outlines the systematic approach to examining financial records and compliance, focusing on objective clarity and scope definition. The primary objective involves assessing the accuracy and reliability of financial statements, ensuring adherence to regulations such as the International Financial Reporting Standards (IFRS). Clearly defined scope includes specific business units or operations, such as retail divisions generating over $10 million in annual revenue, allowing auditors to concentrate on high-risk areas. By establishing criteria for materiality, which may be set at a threshold of 5% of total assets, auditors ensure that significant discrepancies are prioritized, enhancing the overall effectiveness of the audit process.

Risk assessment and materiality considerations

During the audit process, risk assessment plays a critical role in identifying areas that may be susceptible to material misstatements. Auditors evaluate inherent risks, which relate to the nature of the entity and its environment, including industry-specific factors, regulations, and economic conditions. For example, in volatile markets like technology or cryptocurrency, inherent risk levels may increase significantly. The auditors apply a materiality threshold, often quantified as a percentage of total revenue or net profit, to determine the significance of identified risks. This threshold guides auditors in focusing their efforts on areas that could potentially influence the economic decisions of users. The consideration of both risk assessment and materiality ensures a streamlined audit approach that addresses the most critical aspects of financial statements, promoting transparency and accountability within the auditing process.

Data collection methods and sources

Data collection methods in the audit process encompass various techniques used to gather relevant information from multiple sources. Surveys, including questionnaires distributed to employees or stakeholders, provide quantitative insights into organizational practices. Interviews, whether structured or unstructured, offer qualitative data through direct dialogue with personnel at all levels, enhancing understanding of internal controls and processes. Document reviews, which involve analyzing financial statements, internal reports, and compliance records, ensure thorough examination of existing documentation. Observational methods allow auditors to witness processes and operations firsthand, revealing discrepancies or inefficiencies that may not be documented. Additionally, data analytics utilizes software tools to assess large datasets for trends, anomalies, and patterns, facilitating evidence-based conclusions. Together, these diverse methods and sources, which can include financial databases, regulatory filings, and industry benchmarks, support a comprehensive and objective audit methodology.

Internal control evaluation

Internal control evaluation is a crucial aspect of the audit methodology used by certified public accountants (CPAs) during financial audits. This process involves assessing the effectiveness of an organization's policies and procedures in safeguarding its assets, ensuring accurate financial reporting, and complying with applicable laws and regulations. Key components of internal control systems include risk assessment, control activities, information and communication systems, and monitoring processes. During the evaluation, auditors utilize tools such as questionnaires and walkthroughs to gather evidence on controls within specific areas, such as inventory management (often a significant risk area for misstatement). Additionally, auditors may test the design and operating effectiveness of these controls to determine the level of reliance that can be placed on them, impacting the overall audit approach. Effective internal control systems significantly reduce the likelihood of fraud, errors, or inefficiencies while promoting transparency and accountability in financial reporting.

Reporting standards and communication plan

An effective audit methodology ensures adherence to essential reporting standards such as International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). The reporting process details the structured presentation of financial data, ensuring transparency for stakeholders including investors, regulators, and management. A comprehensive communication plan is vital for engaging stakeholders throughout the audit process; this includes regular updates, feedback sessions, and final reporting meetings scheduled every quarter. Certain milestones include preliminary findings communicated within the first month of the audit initiation and a final report delivered within three months. Accountability is maintained through designated points of contact within the audit team providing consistent information flow, allowing for real-time support and addressing inquiries efficiently.

Read Also: Our Auditor's Blogs

Comments