Are you looking to improve your understanding of audit findings? This summary will break down the key aspects of the audit process in a way that's easy to digest. We'll explore common findings, their implications, and how they can inform better practices in your organization. Ready to dive in and enhance your knowledge? Let's get started!

Image cover: Letter Template For Audit Findings Summary

Letter Template For Audit Findings Summary Samples

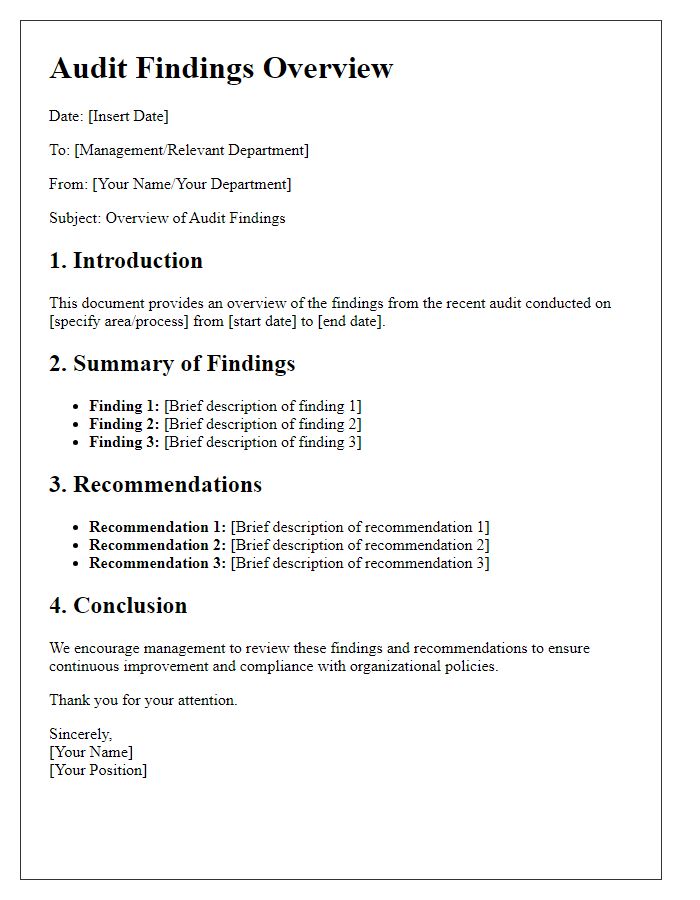

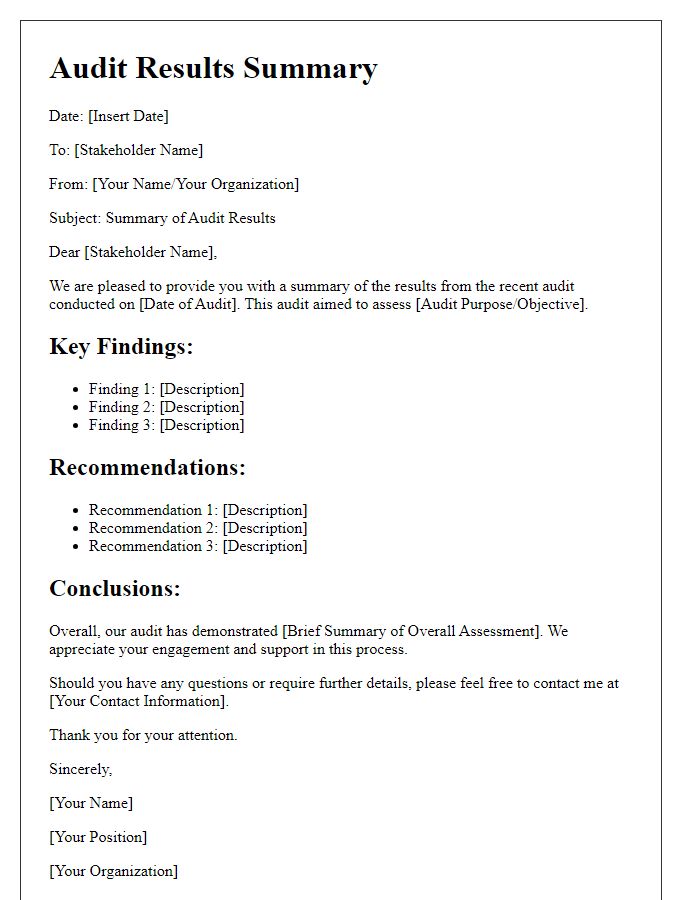

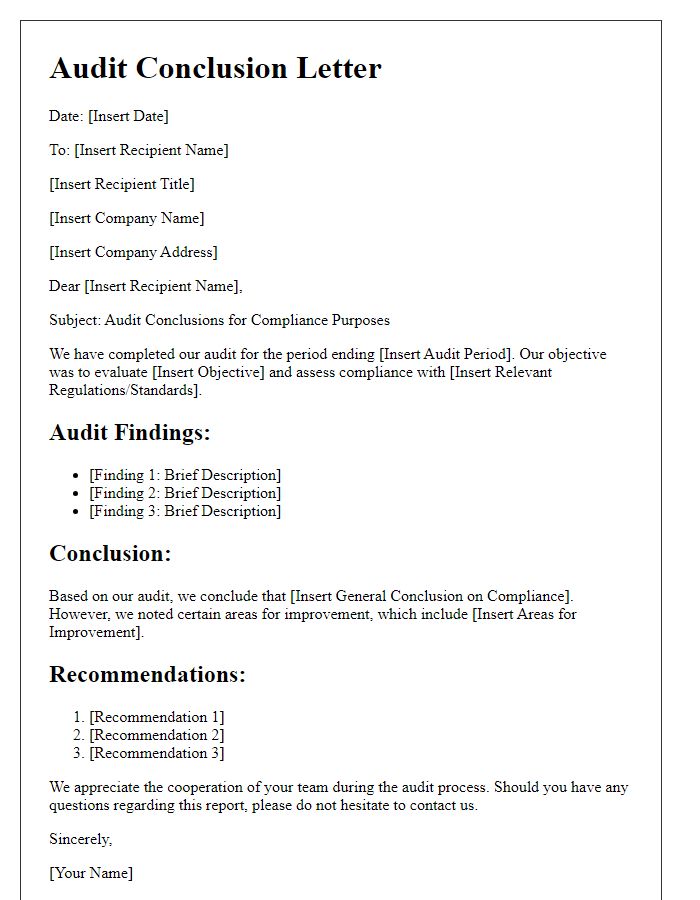

Introduction and Audit Objectives

Audit findings summary provides a comprehensive overview of the assessment conducted within an organization, specifically focusing on financial operations, compliance adherence, and procedural effectiveness. The primary audit objectives include evaluating the accuracy of financial statements, identifying compliance with regulatory standards, assessing internal controls effectiveness, and ensuring operational efficiency. This process involves rigorous examination of documents, interviews with key personnel, and analysis of data to uncover areas of improvement and potential risks, ultimately supporting the organization's strategic goals and fostering accountability.

Summary of Key Findings and Observations

The audit process for the fiscal year ending December 2022 revealed significant findings related to financial compliance within the organization. Revenue recognition practices, specifically regarding the implementation of ASC 606 (Accounting Standards Codification), showcased discrepancies that could lead to misstatements in reported income. Invoices amounting to $150,000, dated from June to August 2022, were not recorded in the correct period, resulting in a potential overstatement of financial results. Additionally, a lack of segregation of duties was identified in the accounts payable process, raising concerns about the risk of fraud. The internal controls surrounding vendor payment authorizations were found to be inadequate, with only one individual authorized to approve transactions over $50,000, posing a severe risk. Furthermore, inventory valuation methods were inconsistent with established accounting policies, leading to a misvaluation of approximately $200,000 in physical assets. These observations highlight the urgent need for remedial actions to mitigate risks and align practices with regulatory compliance.

Recommendations for Improvement

Inadequate internal controls may lead to significant financial discrepancies in organizations, particularly in large corporations with complex operations such as Fortune 500 companies. Regular audits conducted by independent firms, often during quarterly or annual reviews, can identify weaknesses in processes like vendor management or expense reimbursement. Recommendations for improvement include implementing automated systems for expense reporting, which streamline approvals and reduce human error. Training sessions for staff on compliance with financial policies can reinforce best practices. Additionally, adopting a centralized database for tracking invoices can enhance oversight and ensure accurate financial reporting, aiding in reducing instances of fraud and mismanagement.

Management's Response and Action Plan

During the recent financial audit conducted by [Auditor's Firm Name] at [Company Name] for the fiscal year ending [Date], several key findings were identified that necessitate management's immediate attention. Findings included discrepancies in the financial reporting process, a lack of adherence to internal control policies, and instances of non-compliance with relevant regulations such as the Sarbanes-Oxley Act. Management's response outlines a comprehensive action plan addressing each finding, including the implementation of enhanced training programs for staff regarding compliance protocols and the establishment of a dedicated oversight committee to monitor internal controls. Additionally, revised policies will be put in place to ensure accurate financial reporting, alongside regular follow-up audits to reinforce adherence to these new measures. The proactive engagement of [Management Team's Names or Titles] will play a crucial role in driving these initiatives and fostering a culture of accountability within [Company Name].

Conclusion and Next Steps

An effective audit findings summary emphasizes key areas, such as the identification of discrepancies and requires actions for improvement. The conclusion should encapsulate the overall effectiveness of internal controls observed during the audit period, highlighting any significant weaknesses located within processes or financial reporting practices. Recommendations for next steps must include timelines for remediation, assigned responsibilities to specific departments (e.g., finance or operations), and strategies for ongoing monitoring to ensure compliance. Continued communication with stakeholders, including senior management and the audit committee, should facilitate the implementation of proposed corrective actions. Additionally, enhancing training programs and conducting follow-up audits may further support the resolution of identified issues and strengthen overall governance.

Read Also: Our Auditor's Blogs

Comments