When it comes to financial disclosures, transparency is key for public companies. Investors and stakeholders rely on clear, comprehensive information to make informed decisions about their investments. Crafting a well-structured letter can enhance understanding and foster trust between the company and its audience. So, if you're interested in learning how to effectively communicate your financial disclosures, keep reading for our detailed guide!

Image cover: Letter Template For Public Company Financial Disclosure

Letter Template For Public Company Financial Disclosure Samples

Compliance with regulatory requirements

Public companies are mandated to adhere to stringent financial disclosure regulations, ensuring transparency and accountability to shareholders and stakeholders. Securities and Exchange Commission (SEC) guidelines dictate the frequent release of earnings reports, providing comprehensive insights into revenue performance, net income, and operational expenses. The Sarbanes-Oxley Act of 2002 emphasizes corporate governance practices aimed at preventing financial misstatements and enhancing fiscal responsibility. This legislative framework requires chief executive officers (CEOs) and chief financial officers (CFOs) to certify the accuracy of financial statements, with potential penalties for non-compliance. Regular audits by external firms contribute further to the integrity of disclosed information, fostering investor confidence in publicly traded entities.

Clear and concise summary of financial performance

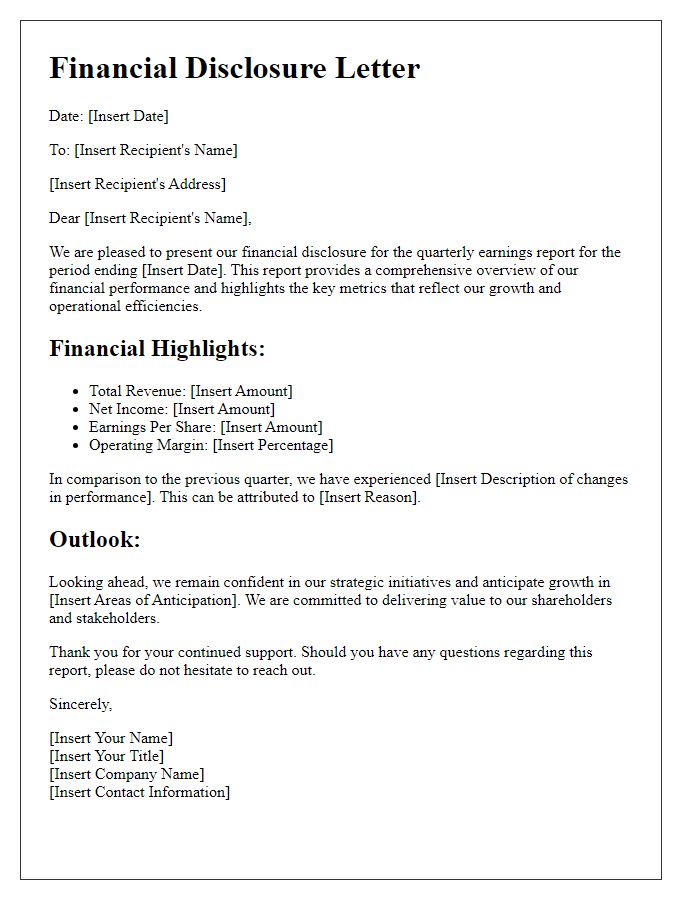

Publicly traded companies must deliver a clear and concise summary of their financial performance quarterly and annually. This typically includes key figures such as total revenue, net income, and earnings per share (EPS). For example, a company may report a revenue increase of 15% to $150 million compared to the previous quarter, with net income reaching $30 million. This performance might be attributed to strong sales in specific markets, such as North America or Europe, where the demand for their flagship product surged. Detailed breakdowns of operating expenses, including Research and Development (R&D) costs, need to be included, showcasing efforts towards innovation. A comparative analysis with prior periods highlights growth trends or challenges in different fiscal quarters, aiding shareholders in making informed decisions. Moreover, any significant events such as acquisitions, mergers, or regulatory changes should be mentioned, providing context for the financial data presented.

Forward-looking statements and risk disclosures

Forward-looking statements, often found in financial disclosures of public companies, present estimates and expectations regarding future performance, growth, and financial conditions. These projections may refer to key indicators such as revenue targets, operational efficiency, or expansion plans into emerging markets. Risk disclosures outline potential challenges faced by companies, including market volatility, regulatory changes, technological disruptions, and supply chain issues, which can significantly affect results. The importance of these statements lies in their role in assessing the company's strategic position, informing investors about uncertainties that could influence financial outcomes, and highlighting areas of opportunity for innovation or investment. Such disclosures must adhere to regulations set by entities like the Securities and Exchange Commission (SEC) and require careful consideration of the underlying assumptions and inherent risks that could impact future performance.

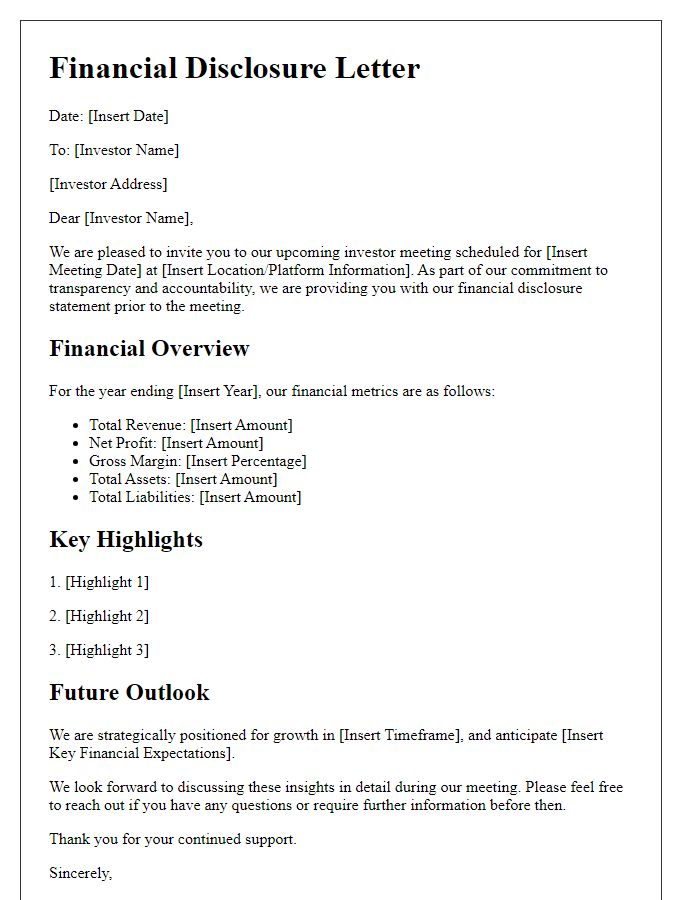

Key financial metrics and highlights

In the first quarter of 2023, Company XYZ reported a total revenue of $150 million, representing a notable increase of 20% compared to Q1 of 2022. The gross profit margin improved to 45%, driven by enhanced operational efficiencies and cost control measures across its manufacturing facilities in Texas. Operational expenses were recorded at $65 million, reflecting a rise of 5% year-over-year. Net income surged to $30 million, showcasing an impressive growth rate of 25%, which resulted in an earnings per share (EPS) figure of $0.75, up from $0.60 in the previous year. The company also announced a dividend payout of $0.10 per share, underscoring its commitment to returning value to shareholders while maintaining a strong cash position of $200 million. Furthermore, new customer acquisitions increased by 15%, highlighting sustained demand for its flagship product line, which includes innovative solutions in the renewable energy sector.

Consistent and transparent reporting format

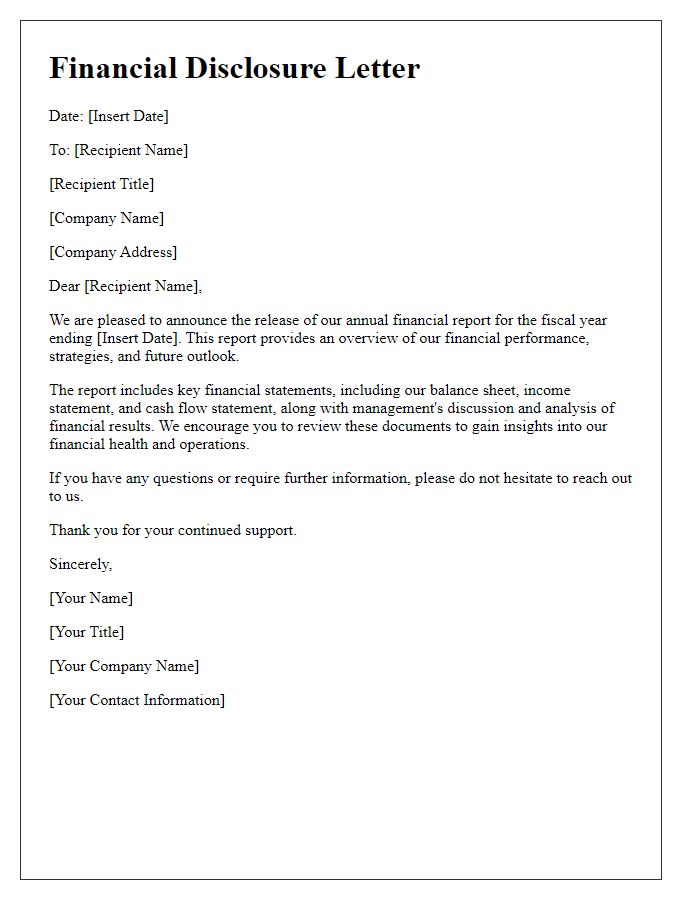

Public companies must adhere to a consistent and transparent financial disclosure format to maintain regulatory compliance and foster investor trust. This framework typically includes detailed sections such as the balance sheet, which showcases assets, liabilities, and shareholder equity figures as of the reporting date; the income statement, revealing revenues and expenses over a specified period, allowing stakeholders to assess profitability; and the cash flow statement, illustrating cash inflows and outflows from operating, investing, and financing activities. Specific metrics noted in financial disclosures may include revenue growth percentage, earnings before interest and taxes (EBIT), and net profit margin, providing insights into financial performance. Additionally, accompanying notes to financial statements can elaborate on accounting policies, risk factors, and contingent liabilities, enriching stakeholders' understanding of the financial position and operational results. Regular adherence to the Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) ensures reliability and comparability across reporting periods.

Read Also: Our Accountant's Blogs

Comments