Hey there! Navigating the world of peer-to-peer loans can feel a bit daunting, but it doesn't have to be. You might be wondering how to formally accept a peer-to-peer loan offer, and that's where a well-crafted letter comes in handy. We've put together a comprehensive guide on crafting your acceptance letter, complete with tips and a handy template, so you can step confidently into your next financial venture. Ready to dive in and make the most of your loan?

Image cover: Letter Template For Peer-To-Peer Loan Acceptance

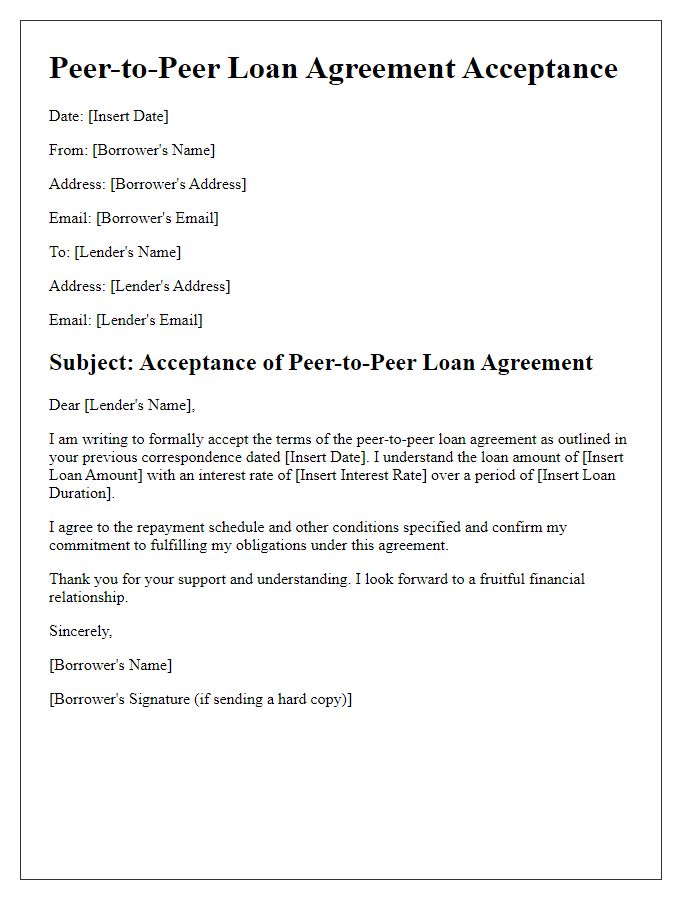

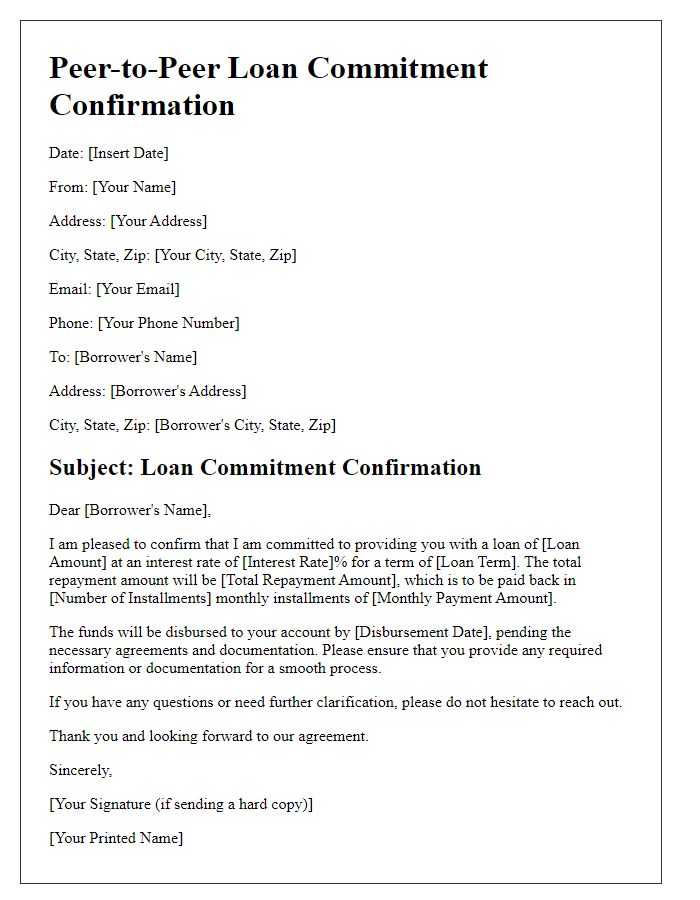

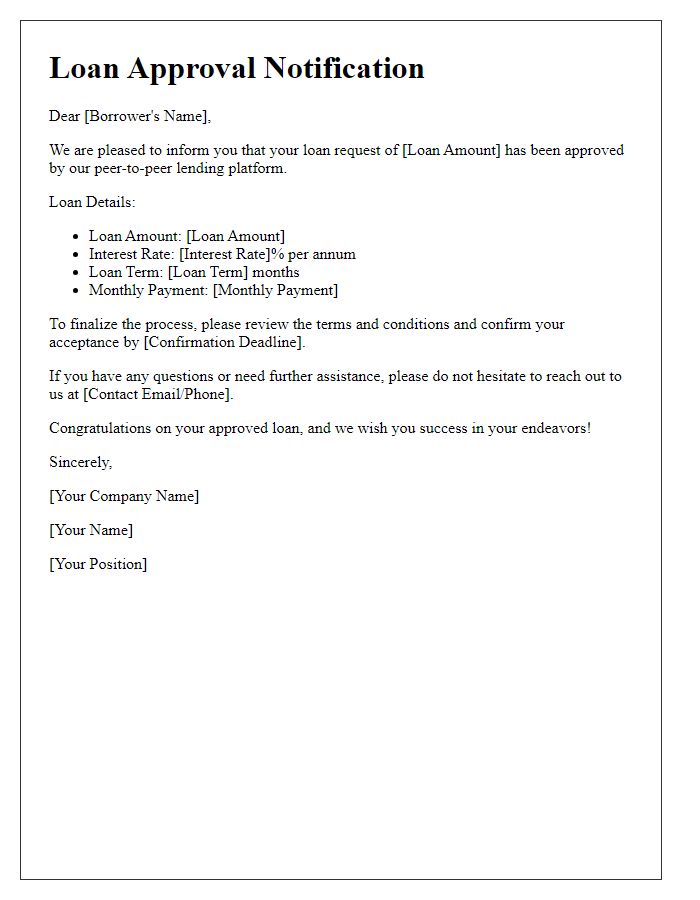

Letter Template For Peer-To-Peer Loan Acceptance Samples

Clear borrower and lender identification

In a peer-to-peer loan acceptance scenario, clear identification of both the borrower and the lender is essential for maintaining transparency and trust. The borrower, an individual or entity seeking financial assistance, should provide their full name, address, and a valid identification number, such as a Social Security number in the United States or a tax identification number for businesses. The lender, often an individual investor or a financial institution, must also present their name, contact details, and relevant identification to establish credibility. Including a loan agreement reference number can further assist in tracking the transaction details. Additionally, stipulating the loan amount, interest rate, and repayment terms within the documentation reinforces accountability for both parties and ensures effective communication throughout the loan process.

Loan amount and currency

A peer-to-peer loan agreement specifies the loan amount and currency clearly to ensure mutual understanding and legal compliance. For instance, a loan of $5,000 USD might be arranged between two individuals through a platform like LendingClub or Prosper. The agreement should detail specific aspects including the duration of the loan, interest rate (often ranging between 5% to 36% based on credit risk), repayment schedule (monthly or biweekly), and any associated fees (such as origination fees, which can be around 1% to 5% of the loan amount). Including the currency specifies that the loan is specifically in United States Dollars, thus preventing confusion for both borrower and lender about the currency exchange rates and payment methods involved.

Interest rate and repayment terms

The peer-to-peer loan agreement outlines conditions including interest rates and repayment terms between the borrower and lender. Typically, interest rates range from 5% to 36%, influenced by credit scores and risk assessments. Repayment terms often vary between 1 to 5 years, with monthly installments specified. Additional factors such as late payment penalties and prepayment options may also be detailed, enhancing transparency in financial responsibilities and obligations for both parties involved in the transaction. Understanding these elements ensures a clear framework for managing the loan effectively.

Loan start date and maturity date

The peer-to-peer loan agreement establishes a loan amount of $10,000, with a loan start date set for April 1, 2023, and a maturity date on April 1, 2025. This duration of two years allows for a structured repayment schedule encompassing monthly installments designed to facilitate timely repayments. Interest rates are fixed at 5% annually, ensuring predictable payments for both lender and borrower. Platforms facilitating such loans often utilize secure technologies to manage transactions while maintaining transparency throughout the term. Furthermore, adherence to local lending laws ensures the transaction remains compliant, safeguarding the interests of both parties involved.

Payment method and late fees

Peer-to-peer loan agreements often include specific terms regarding payment methods and late fee policies. Payment methods may vary, with options such as bank transfers, PayPal, or other financial services like Venmo. Timely repayments are crucial, with standard grace periods typically ranging from 3 to 5 days after the due date. Late fees, often established as a percentage of the outstanding amount, can escalate rapidly, sometimes accumulating at rates of 5% to 10% of the principal each month. Clear communication of these terms is essential to ensure both parties understand their obligations to maintain a successful loan experience.

Read Also: Our Loan provider's Blogs

Comments