Are you considering taking out a fixed-rate loan? Understanding the terms and conditions can be a bit overwhelming, but it doesn't have to be! In this article, we'll break down the key components of fixed-rate loans, making it easier for you to navigate the borrowing process and make informed decisions. So, let's dive in and explore what you need to know to secure the best deal for your financial future!

Image cover: Letter Template For Fixed-Rate Loan Terms Explanation

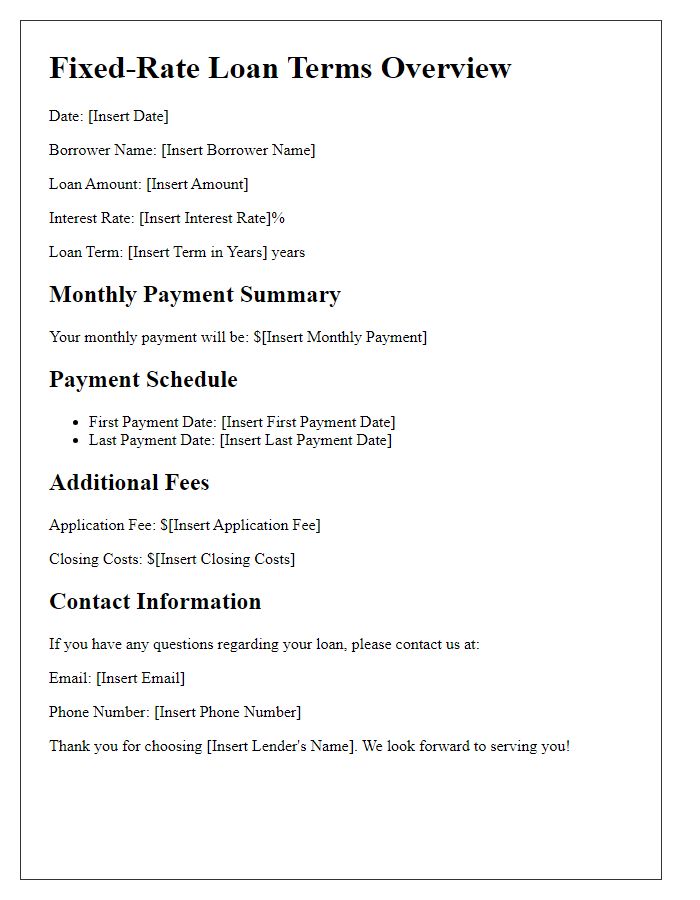

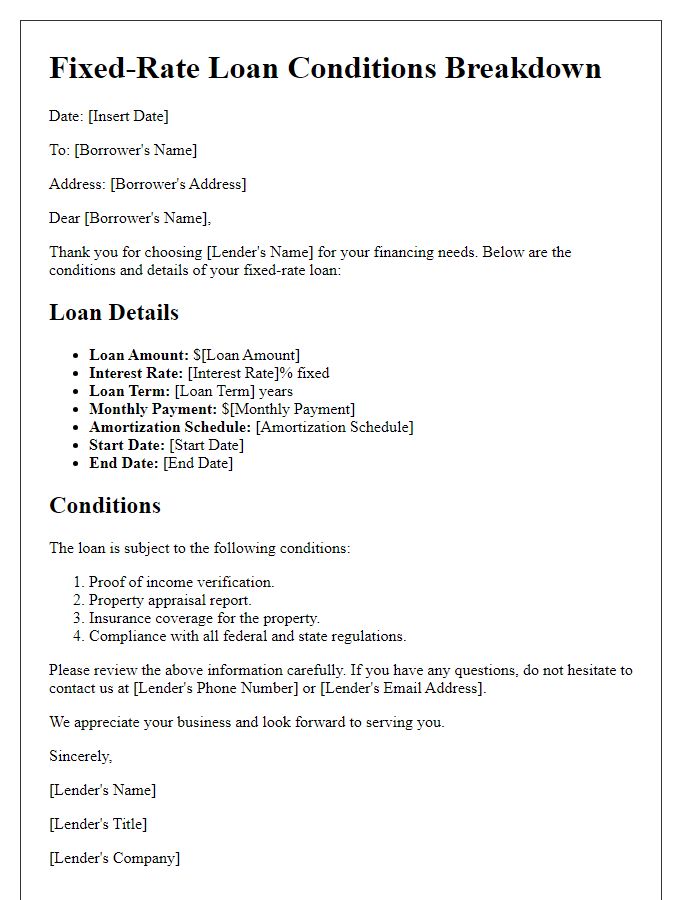

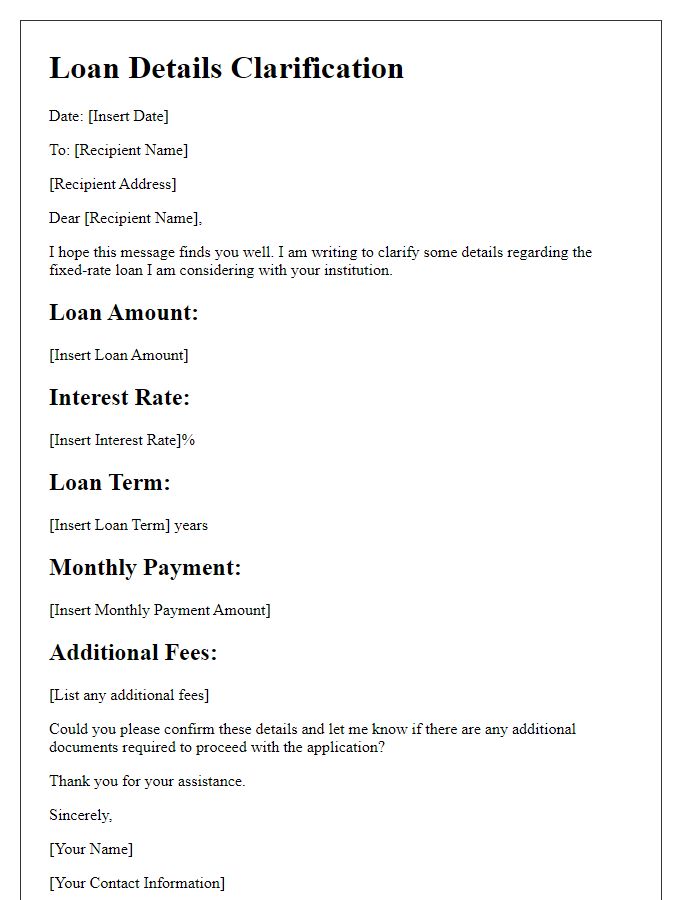

Letter Template For Fixed-Rate Loan Terms Explanation Samples

Loan Amount and Term Details

A fixed-rate loan offers borrowers a specified amount, often ranging from $10,000 to $500,000, with a predetermined interest rate that remains constant throughout the specified repayment period, usually between 5 to 30 years. This type of loan provides stability by ensuring monthly payments remain consistent, allowing borrowers to budget effectively without worrying about fluctuating rates due to market conditions. The repayment structure typically includes principal and interest portions, ensuring the loan is fully paid off by the end of the term. Key factors influencing loan terms include credit scores, current economic conditions, and type of loan, such as conventional or FHA. Understanding these elements is crucial for evaluating overall loan costs and payment strategies.

Interest Rate Description

Fixed-rate loans provide borrowers with a consistent interest rate throughout the loan duration, often making budgeting simpler. For instance, a 5% annual interest rate on a $200,000 mortgage ensures predictable monthly payments over a 30-year period. This stability protects borrowers from market fluctuations and rising interest rates, which often occur during economic changes or shifts in Federal Reserve policies. The principal amount ($200,000) remains unaffected by external market forces, while the total cost can be calculated using amortization schedules. Additionally, lenders may offer varying fixed-rate terms, such as 15 or 30 years, impacting the overall interest paid, with shorter terms generally reducing total interest costs.

Repayment Schedule and Frequency

Fixed-rate loans provide borrowers with a stable repayment schedule, ensuring predictable monthly payments. Typically, repayment occurs on a monthly basis, commonly extending over periods such as 15 or 30 years, allowing for gradual repayment of the principal amount along with fixed interest. For instance, a $200,000 loan at a 4% interest rate over 30 years results in monthly payments of approximately $955. Regular monthly payments facilitate budget management for borrowers, contributing to financial stability. Understanding the specifics of the repayment frequency and schedules ensures borrowers can effectively plan their finances and fulfill their loan obligations without unexpected financial strain.

Fees and Penalties Overview

Fixed-rate loans provide borrowers with predictable monthly payments, making budgeting easier compared to variable-rate loans. Typical terms range from 10 to 30 years, with interest rates fixed over the entire loan duration, ensuring stability despite market fluctuations. Fees associated with fixed-rate loans may include application fees, origination fees, and closing costs, which can vary by lender. Penalties for early repayment often apply, commonly known as prepayment penalties, which can significantly affect borrowers wishing to pay off loans ahead of schedule. Familiarity with these fees and potential penalties is crucial for borrowers to make informed financial decisions and avoid unexpected expenses.

Borrower's Rights and Obligations

The fixed-rate loan agreement outlines specific terms regarding the borrower's rights and obligations, focusing on consistent monthly payments and interest rates that remain unchanged throughout the loan's duration. Borrowers should comprehend their right to receive clear disclosures detailing loan terms, including annual percentage rate (APR), total repayment costs, and potential late fees, ensuring transparency and informed decision-making. Obligations include timely payment adherence to the agreed schedule, which typically spans 15 to 30 years, as non-compliance may result in penalties or default risk, potentially leading to foreclosure on mortgaged property. It's crucial for borrowers to maintain communication with lenders regarding financial changes or repayment difficulties, ensuring compliance with necessary reporting to avoid adverse effects on credit scores and financial stability.

Read Also: Our Financial institution's Blogs

Comments