Are you considering setting up a joint account to streamline your financial planning? Joint accounts can be an effective way for couples or business partners to manage shared expenses, but it's essential to approach them thoughtfully. Discussing your financial goals and establishing clear communication can help prevent misunderstandings down the road. If you're curious about how to navigate the process of joint financial planning, keep reading for expert insights and tips!

Image cover: Letter Template For Joint Account Financial Planning

Letter Template For Joint Account Financial Planning Samples

Purpose and Overview

Establishing a joint account for financial planning can enhance collaborative management of shared expenses and savings goals. A joint account enables two or more individuals, often partners or family members, to pool resources for specific purposes such as household costs, vacations, or emergency funds. The account facilitates transparent tracking of contributions and expenditures, minimizing potential misunderstandings. Key benefits include simplified budgeting and the ability to reach financial milestones more effectively. When the account holders regularly communicate about their financial objectives, they can align spending habits and savings strategies, fostering a sense of partnership in achieving shared financial security.

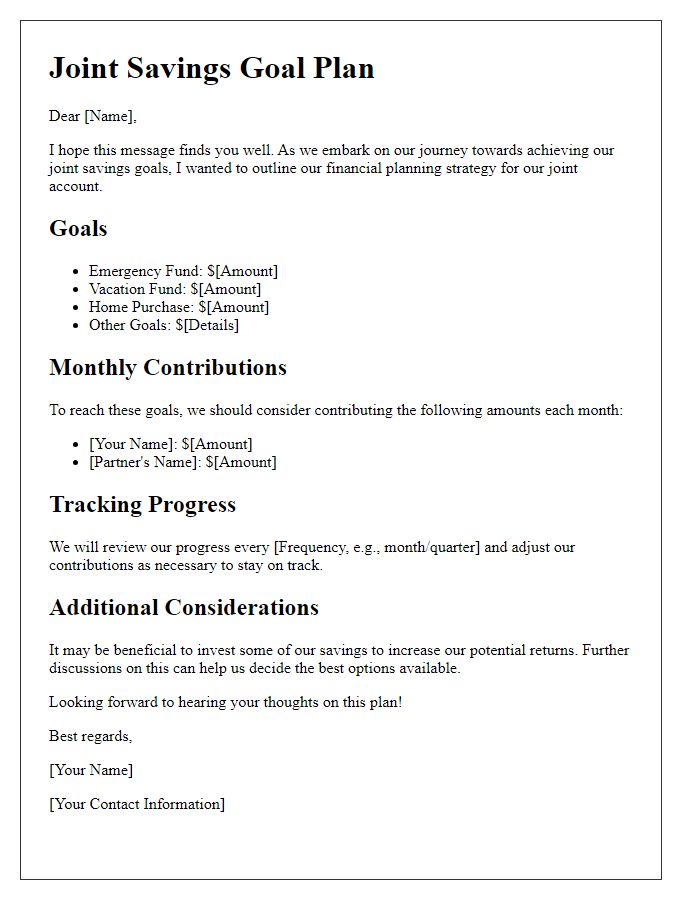

Financial Goals

Financial planning for joint accounts necessitates clear communication about financial goals. Couples should identify specific objectives, such as saving for a home (average cost of a house in the U.S. is over $300,000), retirement (with a target retirement age of 65 and a recommended savings of 15% of income), or funding children's education (where college expenses can exceed $30,000 annually). Choosing a joint savings strategy, such as traditional savings accounts or higher-yield options like certificates of deposit, is crucial for effective fund growth. Each partner should assess their contributions, ensuring a balanced approach, while regularly reviewing progress toward goals. Additionally, creating a budget will help manage monthly expenses and track fluctuations in income, hence sustaining financial stability.

Account Management

Effective joint account financial planning requires careful account management strategies. Regular communication between account holders ensures transparency regarding shared expenses, income contributions, and savings goals. Monthly budget reviews, ideally scheduled around the first week, can facilitate discussions about individual spending habits and necessary adjustments to maintain financial balance. Utilizing budgeting tools, such as mobile applications or spreadsheets, can help track expenditures accurately and provide visual representations of financial health. Setting clear financial objectives, including retirement savings (such as a combined $500,000 target by age 65) and emergency funds (aiming for three to six months' worth of living expenses), fosters alignment between both parties. Furthermore, periodic evaluations of investment strategies, particularly those in retirement accounts (like 401(k)s or IRAs), contribute to achieving long-term wealth growth while considering risk tolerance levels tailored to each partner's financial philosophy.

Contribution Agreement

A letter template for a joint account financial planning Contribution Agreement serves as a structured document outlining the specific financial commitments made by each party involved in a shared account. This agreement documents the allocation of funds, specifying percentages or fixed amounts each participant will contribute towards joint expenses. Clarity in expectations helps prevent misunderstandings regarding financial responsibilities, promoting transparency in shared financial goals like saving for a home or planning a vacation. Essential elements include the names of the account holders, contribution amounts, payment schedules, and provisions for changes in contributions or exit strategies. This template not only fosters accountability but also strengthens the financial partnership by establishing a clear framework for collaboration.

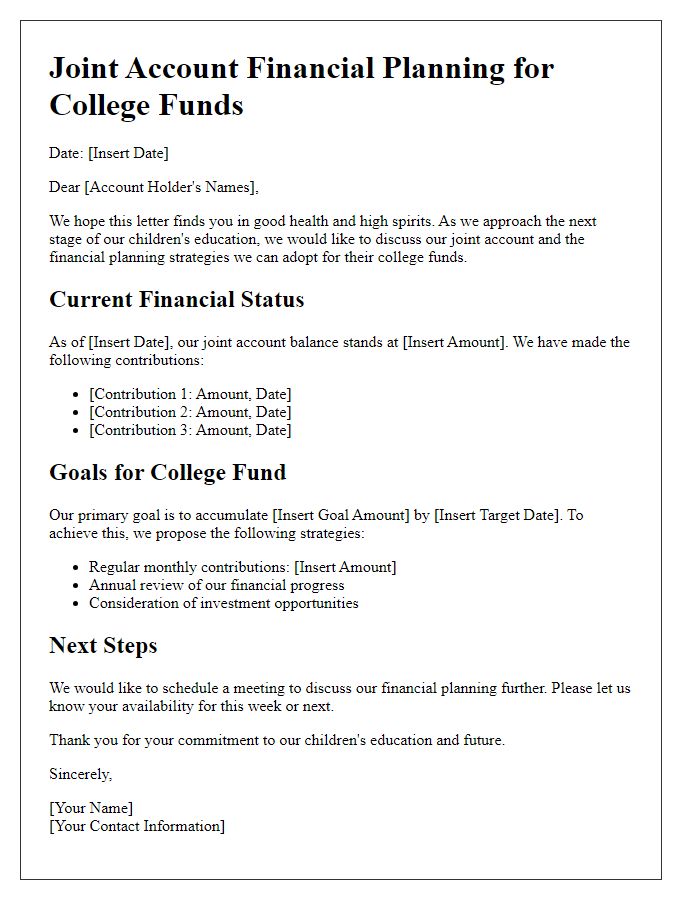

Review and Adjustment Plan

Creating a comprehensive financial planning review and adjustment plan for a joint account requires a thorough examination of income, expenditures, savings goals, and investment strategies. This plan aims to align both account holders' financial objectives, often involving detailed budget analysis, updated assessments of financial goals, and evaluations of current market trends affecting investments. According to recent data, joint households in the United States, approximately 27% of which manage assets over $100,000, should regularly assess their financial strategies to ensure both partners are on the same page regarding long-term goals such as retirement, major purchases, or emergency savings. Moreover, regular reviews can facilitate discussions on spending habits or any necessary changes prompted by significant life events, such as job changes or family expansions, impacting financial dynamics. Overall, a clear outline and structured approach to reviewing and adjusting the financial plan can promote healthy financial management in a joint account setting.

Read Also: Our Financial consultancy's Blogs

Comments