Are you tired of high-interest rates eating away at your finances? A credit card promotional balance transfer might just be the solution you need to regain control. By moving your existing credit card debt to a card with a lower interest rate, you can save money and pay off your balance faster. Curious about how this process works and the benefits it can bring? Read on to discover more!

Image cover: Letter Template For Credit Card Promotional Balance Transfer

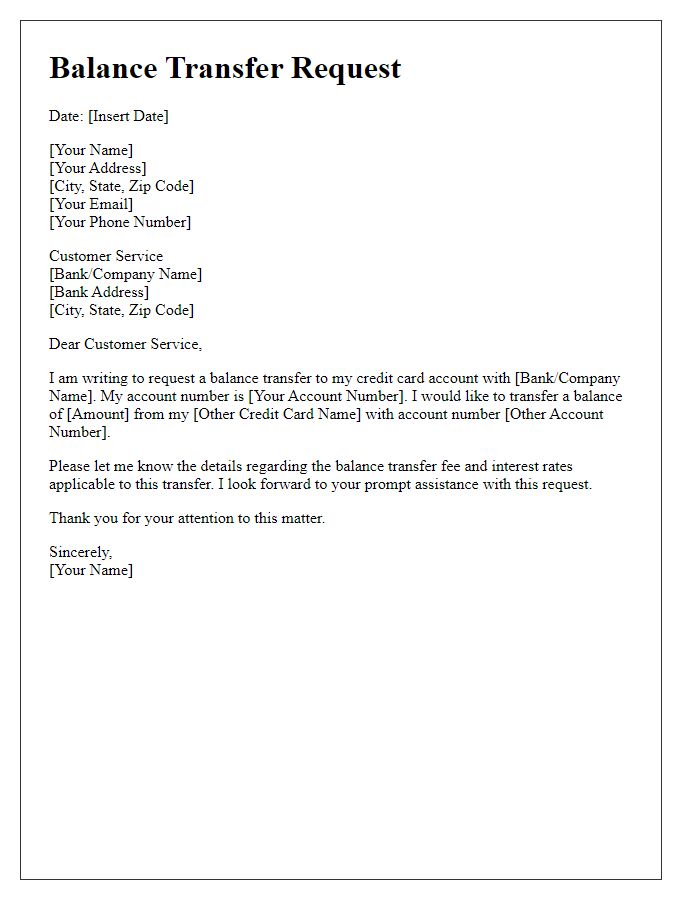

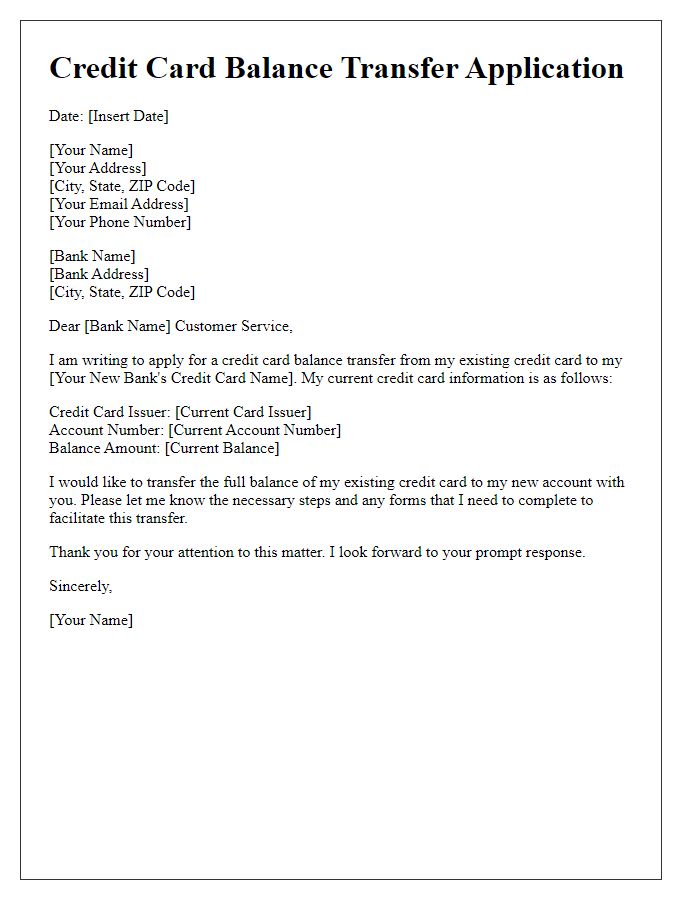

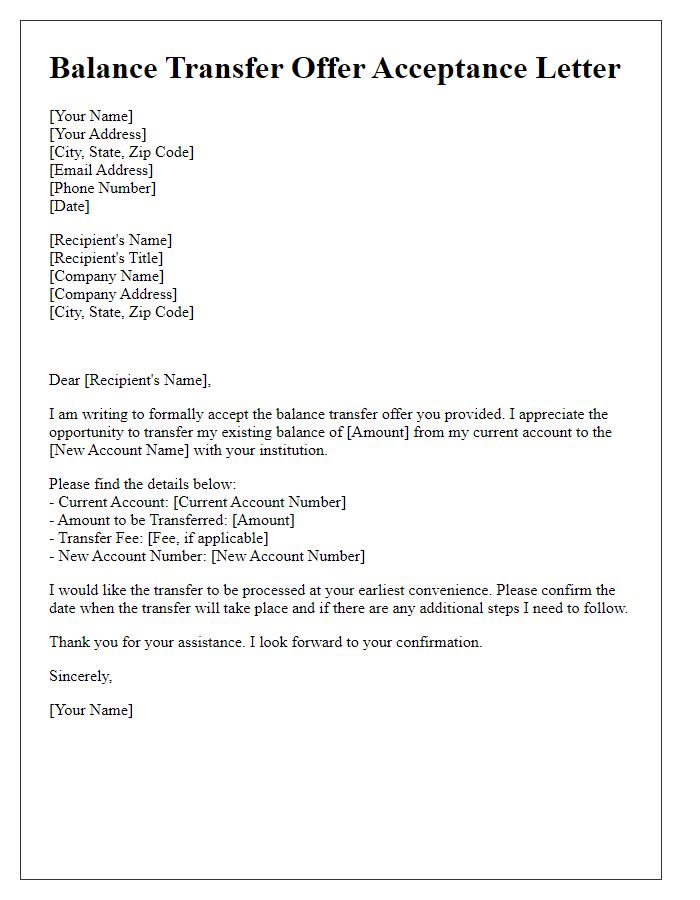

Letter Template For Credit Card Promotional Balance Transfer Samples

Introductory offer details

Credit card promotional balance transfer offers are designed to attract new customers with enticing incentives. Typically, these offers feature a low or 0% introductory annual percentage rate (APR) for a specified period, often ranging from 12 to 18 months, enabling cardholders to transfer outstanding balances from other credit cards, such as Visa, MasterCard, or American Express, without incurring interest during that promotional timeframe. Clear terms accompany these offers, detailing any balance transfer fees--usually around 3% to 5% of the transferred amount--as well as the standard APR applying after the promotional period ends. Many financial institutions, including banks like Chase, Citibank, or Capital One, provide online applications for convenience, allowing potential customers to quickly determine eligibility and see potential savings, especially for those carrying significant credit card debt.

Eligibility criteria

Eligibility for promotional balance transfers often requires applicants to meet specific criteria set by financial institutions. Age must be at least 18 years, establishing legal responsibility for a credit contract. A valid Social Security number or taxpayer identification number is typically necessary for identity verification. Applicants generally need to maintain a steady source of income, evidenced by recent pay stubs or tax returns, ensuring ability to manage debt. Creditworthiness indicated by a minimum credit score, often around 650 or above, is crucial for approval, as it reflects risk to lenders. Existing credit card balances must usually be from different issuers, as internal transfers may not qualify for promotional rates, maximizing potential savings. Details regarding promotional terms, such as introductory APR rates, duration of the offer, and any applicable fees must be carefully reviewed before proceeding.

Transfer fee information

Promotional balance transfer offers can significantly alleviate financial burdens. Typically, a transfer fee of 3% to 5% applies, based on the total amount transferred. For example, transferring a balance of $5,000 could incur a fee ranging from $150 to $250. This fee is often added to the transferred balance, affecting the overall debt. Many credit card issuers, like Chase or Citibank, may provide promotional periods lasting 12 to 18 months during which interest rates could be as low as 0% APR, provided the transfer occurs within a specific timeframe. It's essential to read the terms carefully since missing payments during this promotional period can trigger higher interest rates on the remaining balance.

Payment terms and conditions

Promotional balance transfers from credit card companies can provide significant financial relief. Generally, these offers feature low introductory annual percentage rates (APRs), often around 0% for the first 12 to 18 months, allowing consumers to save on interest payments. Transfer limitations may apply, typically capping the maximum amount at 75% of the credit limit on the new card. Standard transfer fees, which can range from 3% to 5% of the amount transferred, often apply. Additionally, it's crucial to understand the terms that revert to the standard APR post-introductory period, potentially exceeding 20%. Late payments or missed deadlines can lead to penalties, including the loss of promotional rates. Being aware of these conditions ensures informed financial decisions for managing credit effectively.

Expiry of promotional rate

Promotional balance transfer offers often entice consumers with a temporary low interest rate, typically ranging from 0% to 3.99% for a specific duration, usually between 6 to 18 months. These offers can help individuals consolidate debt accrued from high-interest credit cards or loans, providing an opportunity to pay down balances more efficiently. However, it is crucial for consumers to be aware of the promotional rate's expiration, as post-promotional interest rates can soar to standard rates, sometimes exceeding 20%. Missing payments or exceeding credit limits during the promotional period can also lead to the loss of this advantageous rate. Understanding the terms, including any balance transfer fees, is essential for maximizing the benefits of such offers while avoiding potential financial pitfalls in the future.

Read Also: Our Credit card company's Blogs

Comments