Hey there! Understanding how promotional credit can affect your credit score is crucial for making smart financial decisions. Many people are unaware that these offers can positively or negatively influence their score, depending on how they manage them. If you're curious about the ins and outs of promotional credit and want to learn how to navigate this often-overlooked aspect of credit scoring, keep reading!

Image cover: Letter Template For Promotional Credit Impact On Score

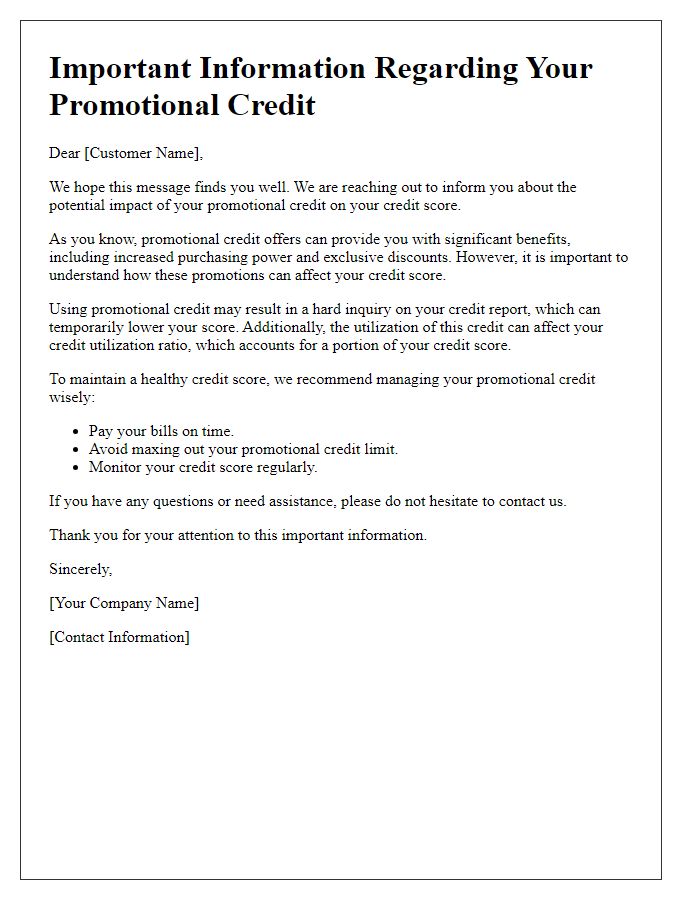

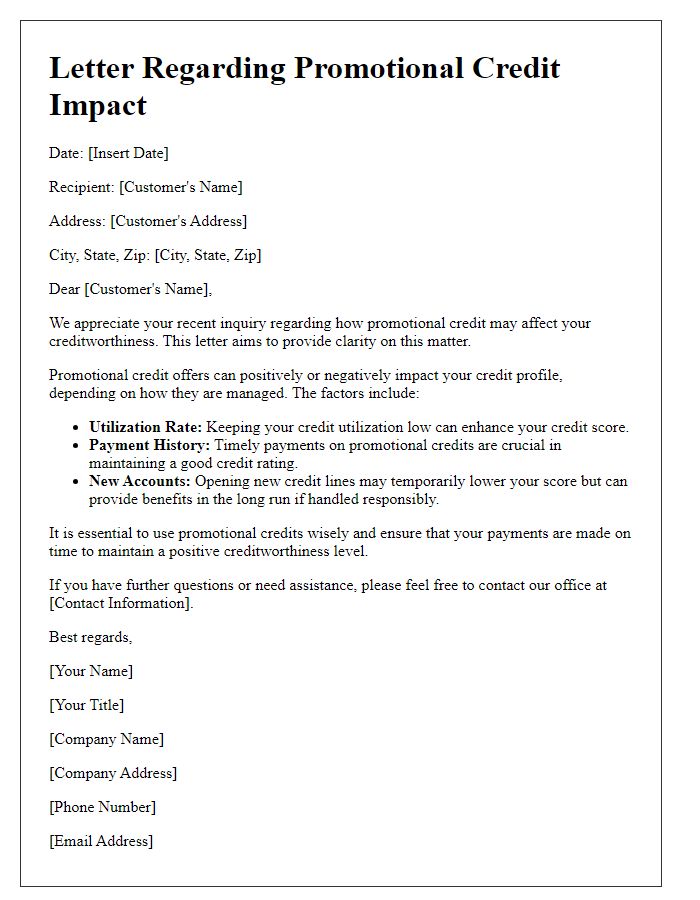

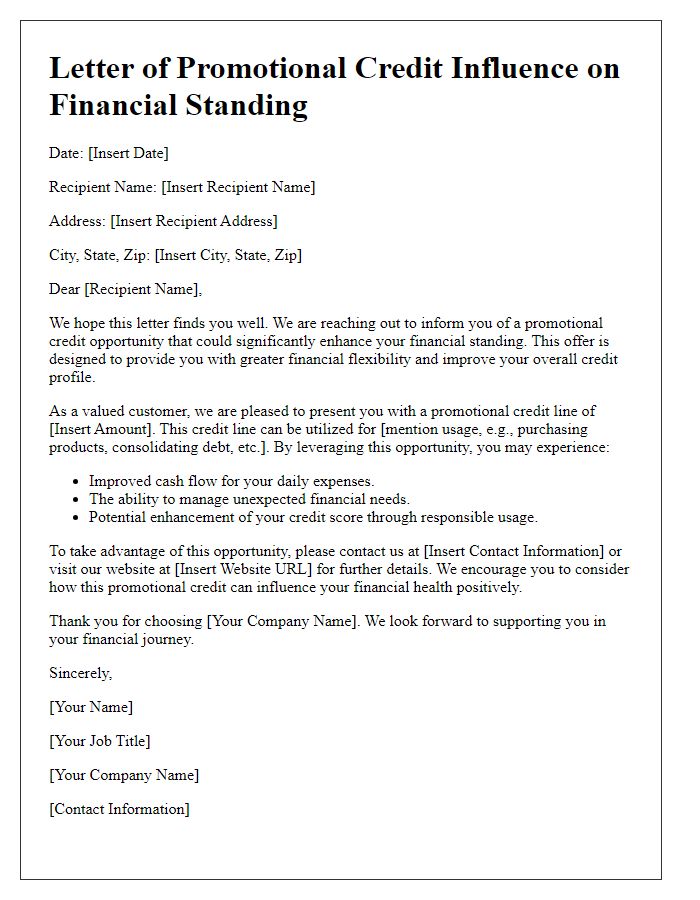

Letter Template For Promotional Credit Impact On Score Samples

Credit Score Changes

Promotional credit offers can significantly influence individual credit scores, especially those involving new lines of credit. For example, applying for a promotional credit card may result in a hard inquiry that can decrease a credit score by 5 to 10 points temporarily. Additionally, utilizing this credit can increase the credit utilization ratio--defined as the total credit used divided by total credit available. A ratio above 30% may negatively impact scores, while maintaining low utilization can contribute to better scores over time. Moreover, timely payments on promotional credit accounts can enhance payment history, which constitutes 35% of the FICO score calculation, thus positively influencing overall creditworthiness.

Promotional Credit Benefits

Promotional credit offers can significantly enhance an individual's credit score, especially when utilized effectively. For instance, a promotional credit card from a notable financial institution can provide a temporary interest-free period, allowing users to manage their finances responsibly. When individuals utilize only a portion of their credit limits, typically below 30%, they can boost their credit utilization ratio. Credit scores, calculated by major credit bureaus like FICO or VantageScore, can reflect positive changes typically within one or two billing cycles. Additionally, timely payments during promotional periods contribute to an improved payment history, a critical factor in credit score calculation. Overall, understanding how to leverage promotional credit strategically can lead to long-term financial benefits.

Temporary vs. Permanent Impact

Promotional credit programs, such as those from major retailers or financial institutions like credit card companies, can temporarily influence credit scores based on specific usage and repayment behavior. When a consumer utilizes promotional credit for high-value purchases, it may initially increase their credit utilization ratio, potentially lowering their score since utilization above 30% is generally considered detrimental. However, timely repayments during the promotional period can lead to positive credit history, which contributes positively to the score over time. Permanent impacts occur when consumers default or do not adhere to repayment terms, leading to derogatory marks on credit reports that can substantially lower scores for years, impacting future creditworthiness. Understanding these dynamics is crucial for consumers seeking to manage their credit health effectively.

Monitoring Credit Reports

Monitoring credit reports is essential for understanding personal financial health and evaluating creditworthiness. Regular reviews of credit reports from major agencies, such as Equifax, Experian, and TransUnion, can help identify discrepancies or fraudulent accounts that might negatively affect scores. A typical credit score ranges from 300 to 850, with higher scores indicating better creditworthiness. Noting significant events like late payments, high credit utilization ratios (ideally below 30%), and the age of credit accounts provides insight into factors influencing credit scores. Accessing these reports at least once a year, as encouraged by the Fair Credit Reporting Act, allows individuals to stay informed and make necessary adjustments to enhance their credit profiles.

Communication with Credit Bureaus

Communication with credit bureaus can significantly influence promotional credit offers and their subsequent impact on credit scores, particularly for consumers seeking to leverage opportunities for financial growth. Credit bureaus, including Experian, Equifax, and TransUnion, track an individual's credit history, encompassing various factors such as payment history, credit utilization ratio (ideally below 30%), and length of credit history, which averages around 15 years for a healthy profile. When new promotional credit inquiries occur, they can result in hard inquiries on credit reports, potentially lowering scores by a few points (typically 5 to 10 points), particularly if there are multiple inquiries within a short timeframe. Monitoring services, like Credit Karma or MyFICO, empower consumers to track changes effortlessly alongside educational resources regarding optimal credit management strategies. Establishing open lines of communication with credit bureaus ensures accurate reporting and rectification of any discrepancies that may arise, ultimately fostering a healthier credit profile conducive to favorable promotional offers.

Read Also: Our Credit applicant's Blogs

Comments