Are you diving into the world of audit sampling methodologies and feeling a bit overwhelmed? You're not aloneâmany auditors find this topic complex but essential for ensuring accurate results. In this article, we'll break down the key concepts, practical tips, and common pitfalls to watch out for when implementing sampling techniques. So, grab a cup of coffee and join us as we explore these vital insights tailored just for you!

Image cover: Letter Template For Audit Sampling Methodology

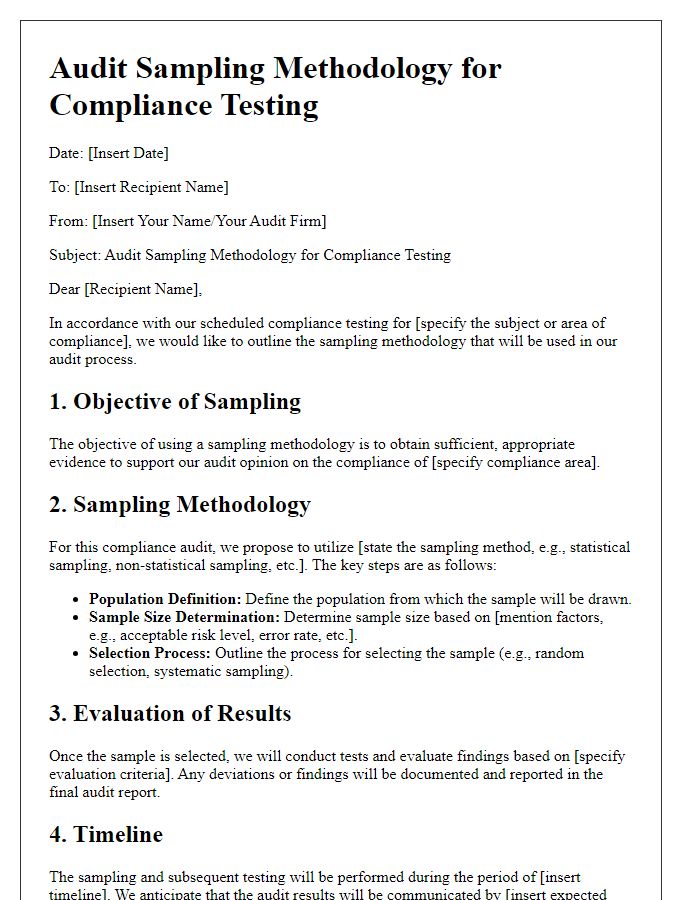

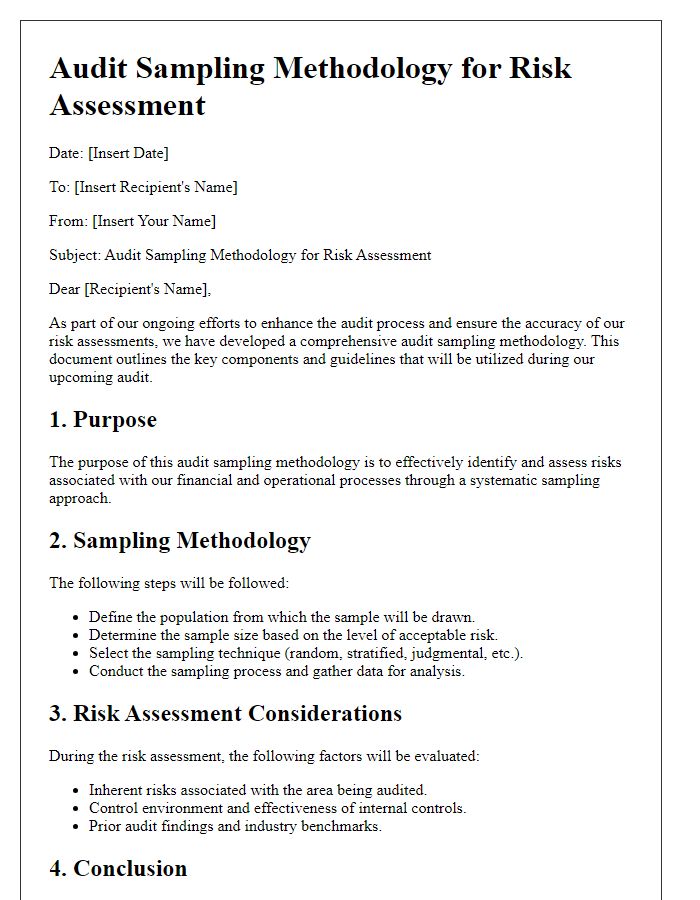

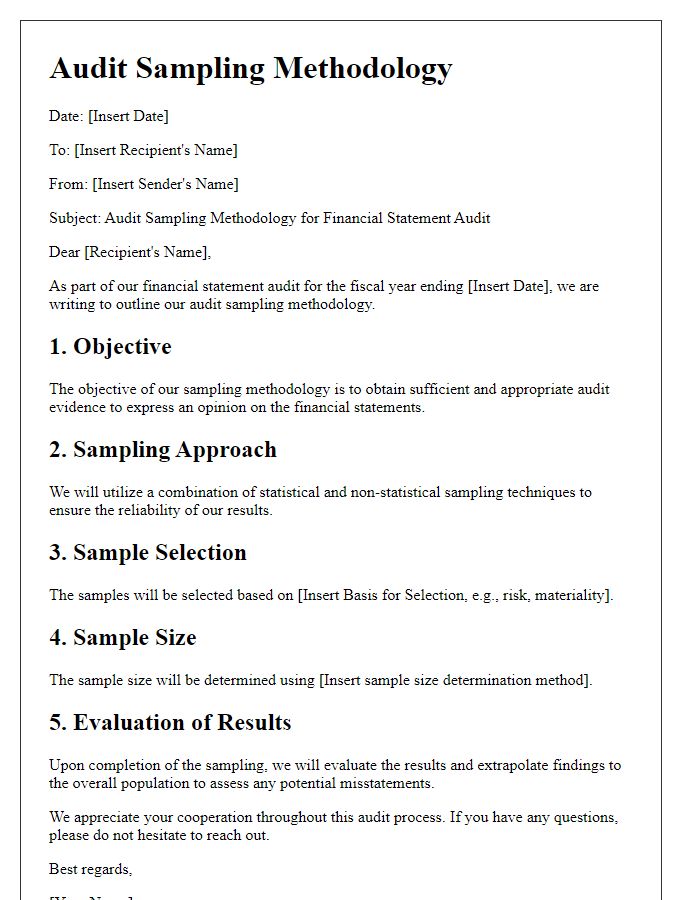

Letter Template For Audit Sampling Methodology Samples

Purpose and Objective of the Audit

The primary purpose of the audit sampling methodology is to evaluate financial statements and operational processes with an emphasis on accuracy, compliance, and efficiency. This involves selecting an appropriate sample size from the total population, which may include transactions, accounts, or internal controls, to draw meaningful conclusions about the overall integrity of the financial data. The objective focuses on identifying material misstatements (errors or fraud that could influence economic decisions) that may exist within the sampled data set, guiding auditors in assessing risks effectively. A systematic approach ensures that the sampling techniques meet industry standards, enhancing the reliability of the audit results and providing stakeholders with a clear understanding of the organization's financial health as reported in documents such as the 2022 Annual Report or financial statements presented to creditors and investors.

Sampling Criteria and Techniques

Audit sampling methodology incorporates specific criteria and techniques essential for ensuring representativity, accuracy, and reliability in the evaluation of financial statements. Statistical sampling methods, such as random sampling, can yield insights into the population's characteristics, while non-statistical sampling may involve judgment-based selections to target high-risk areas. Common sample sizes often range from 30 to 100 items, depending on the population's size and auditor's significance threshold, usually set at 5%. Techniques like attribute sampling help in testing the existence of specific attributes in a population, while variable sampling can measure monetary amounts or variances. Additionally, stratified sampling divides the population into subgroups, allowing each stratum to be sampled proportionally to its size, enhancing coverage and reducing variability. Clear documentation of sampling decisions and methodologies is crucial for transparency and future reference.

Risk Assessment and Materiality Considerations

Audit sampling methodology encompasses the systematic approach to selecting and evaluating a portion of financial data or transactions to draw conclusions about the entire population, particularly in risk assessment and materiality considerations. Risk assessment involves identifying and evaluating risks of material misstatement in financial statements, with specific attention to inherent risks, such as fraud or error, and control risks, which arise from the inadequacy of internal controls. Materiality considerations relate to the significance of transactions, balances, and disclosures, often based on quantitative thresholds, such as 5% of net income or 1% of total assets. The auditor utilizes sampling methods, like statistical sampling (e.g., random sampling) or non-statistical sampling (e.g., judgmental sampling), to effectively focus on high-risk areas while ensuring the audit remains efficient and cost-effective. This methodology supports the auditor's ability to provide reasonable assurance that the financial statements are free from material misstatement, reinforcing the credibility of financial reporting.

Sample Size Determination and Rationale

Determining sample size in audit sampling methodology involves statistical analysis and risk assessment. Sample size should reflect the population size, typically defined by transaction volume or dollar amount, as seen in financial audits performed for companies with revenue exceeding $1 million annually. Confidence levels, often set at 95%, establish the degree of certainty in the sample results, while tolerable error rates (commonly around 5%) dictate the acceptable threshold for discrepancies in the sample findings. Moreover, audit risks, including inherent and control risks, are critical in shaping the size; higher risks may necessitate a larger sample. Utilizing tools like the AICPA sampling tables or software can streamline calculations, ensuring adherence to professional standards established by the International Auditing and Assurance Standards Board (IAASB). Consequently, proper sample size determination not only enhances audit effectiveness but also strengthens stakeholder confidence in the financial reporting process.

Documentation and Reporting Requirements

Audit sampling methodology plays a crucial role in ensuring rigorous examination and compliance with standards. Auditors must adhere to specific documentation requirements, including retaining records of sample selections, population definitions, and sample sizes. Reporting should clearly outline audit objectives, sampling techniques, and findings. Various approaches, such as statistical sampling (e.g., random selection) or non-statistical sampling (e.g., judgmental selection), affect reporting outcomes. For financial audits, sampling could involve transactions from entities like Corporations (e.g., Fortune 500 companies), while operational audits might focus on departmental procedures within organizations. Each methodology must comply with regulatory frameworks (such as GAAP or IFRS), ensuring transparency and reliability in audit reports. Effective methodology enhances the audit's credibility, providing stakeholders with insight into compliance, risk management, and operational efficiency.

Read Also: Our Auditor's Blogs

Comments