Are you feeling a bit anxious as your loan term comes to an end? It's important to understand the implications of a balloon payment, which can catch many borrowers off guard. This type of payment often requires a larger sum due at the end of the loan period, and it's crucial to be prepared for it. Dive into our article to learn more about balloon payments and how to navigate them effectively!

Image cover: Letter Template For Balloon Payment Warning

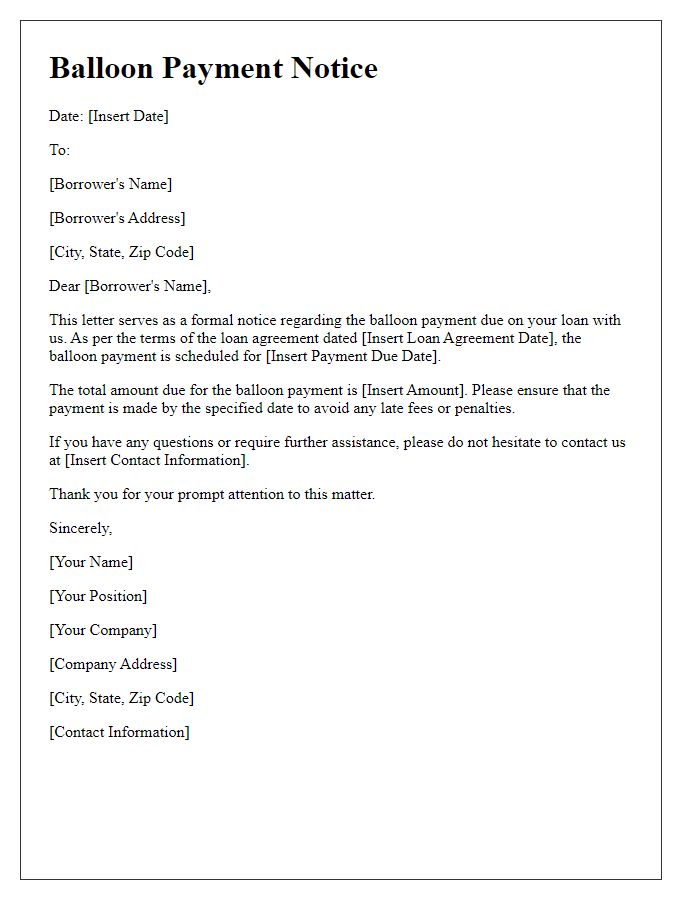

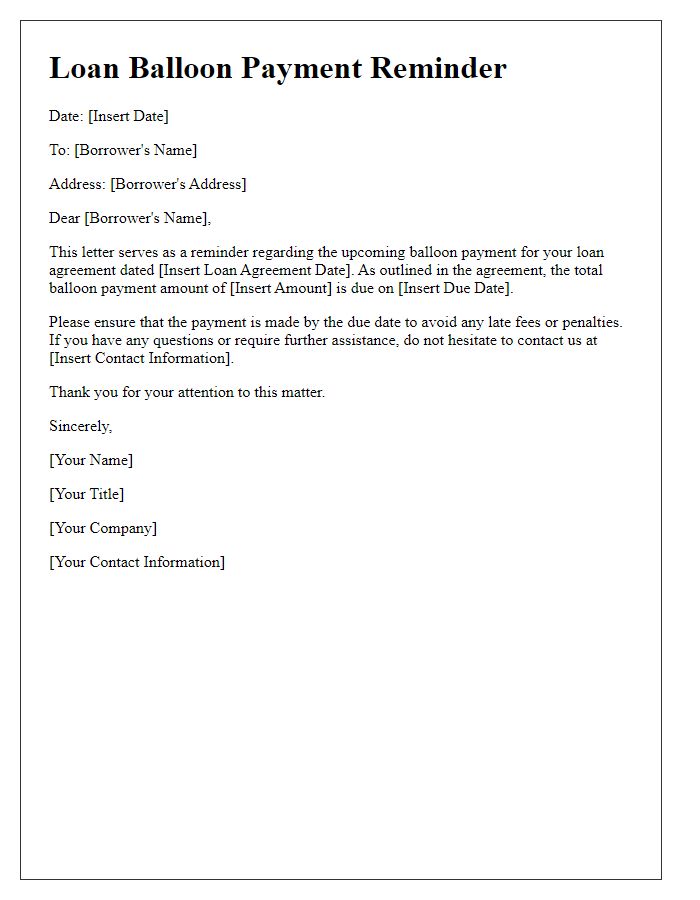

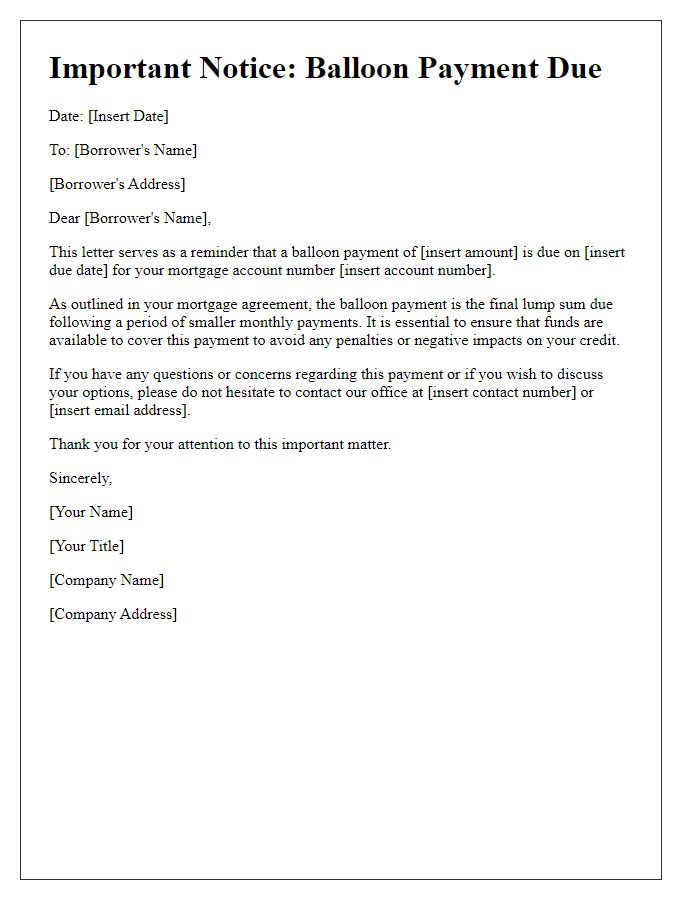

Letter Template For Balloon Payment Warning Samples

Clear subject line

Balloon payments represent a significant financial obligation at the conclusion of loans, typically associated with mortgages or auto loans. A balloon payment occurs when a borrower must pay a larger than usual final payment after a series of smaller installment payments. In the context of a $200,000 home mortgage with an initial 30-year term but only a 5-year fixed rate, the borrower might face a balloon payment of approximately $180,000 due at the end of the 5-year period. Such payments can lead to financial strain if the borrower has not adequately planned for this eventuality or if property values in the area (for instance, the housing market in Phoenix, Arizona, as of 2022) have been volatile. It is essential for borrowers to communicate with their lenders well in advance, ensuring they understand the full implications and options available when approaching the due date of a balloon payment.

Detailed payment information

A balloon payment, often associated with loans or financing agreements, represents a large final payment due at the end of a loan term. Typically, this payment occurs after a series of smaller, regular payments that cover only interest or principal for a predetermined period. For example, a five-year auto loan could require minimal monthly payments, culminating in a substantial final payment that covers the remaining balance, potentially amounting to thousands of dollars. This final payment must be accounted for in financial planning, especially for borrowers with fixed incomes or tight budgets. Additionally, borrowers should be aware of any refinancing options, penalties for non-payment, and the potential risk of losing collateral, such as a vehicle or property, if they cannot meet the balloon payment obligation.

Consequences of non-payment

Balloon payments, common in various types of loans, represent a significant final payment that can pose challenges for borrowers. Failure to fulfill these substantial obligations, often amounting to large sums (potentially exceeding tens of thousands of dollars), can lead to serious financial repercussions. Lenders, including banks or credit unions, may initiate collections processes, resulting in damage to credit scores, which may fall below 600, thus affecting future borrowing capabilities. Additionally, legal actions could arise, with borrowers potentially facing lawsuits or foreclosure on property tied to the loan. The potential stress and financial strain can lead to challenges in meeting other obligations, thereby creating a cycle of debt and impacting overall financial stability.

Contact information

A balloon payment is a large final payment due at the end of a balloon loan, such as a commercial real estate mortgage or a vehicle loan. This payment can significantly impact an individual or business's financial situation, often requiring careful budgeting and planning. The balloon payment can be due at the end of a specific term, usually ranging from three to seven years. It is crucial to review loan agreements, understand payment schedules, and prepare for this substantial financial obligation. Contact information, including email and phone numbers, should be readily available for inquiries regarding payment arrangements or refinancing options.

Financial planning advice

A balloon payment, a lump sum due at the end of a loan term, can significantly impact borrowers financially. For example, a mortgage loan of $300,000 with a five-year term may require a large balloon payment of $250,000 at maturity, creating potential financial strain. Homeowners in areas like California, where housing markets fluctuate, may face difficulties securing refinancing options. Financial planning advice becomes crucial in such scenarios, encouraging borrowers to set aside funds periodically or consider alternative loans with amortization schedules. Being proactive can help manage balloon payment risks, ensuring stability when the payment is due.

Read Also: Our Lender's Blogs

Comments