Are you worried about the potential lapse in your insurance policy? It's a common concern, and understanding how to prevent it is crucial for maintaining your coverage. In this article, we'll explore some effective strategies to ensure that your policy remains active and protects you when you need it most. Keep reading to discover tips that can help you stay ahead of policy lapses!

Image cover: Letter Template For Policy Lapse Prevention

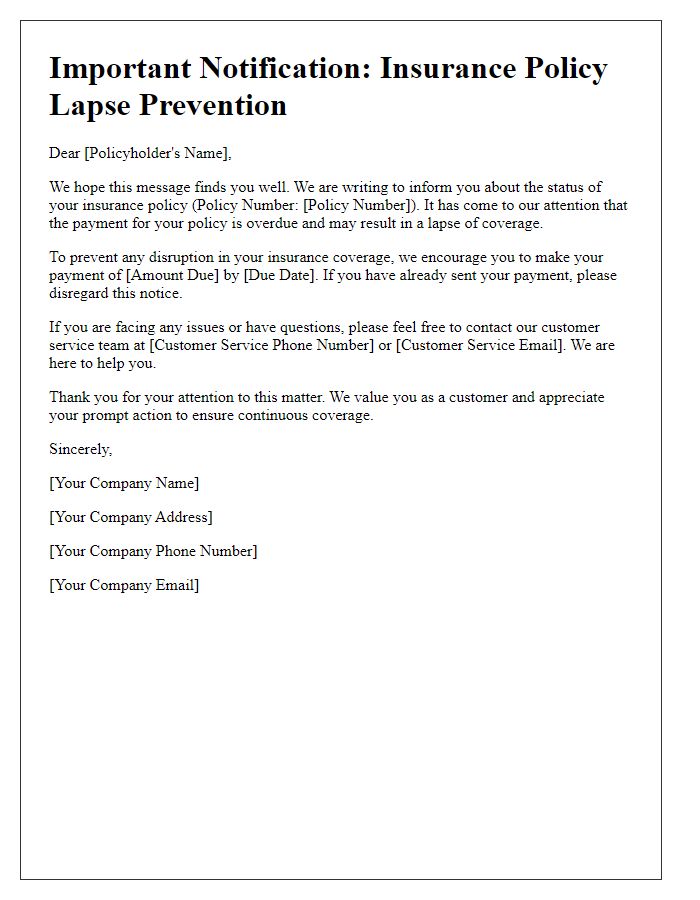

Letter Template For Policy Lapse Prevention Samples

Personalized Greeting

A personalized greeting enhances customer engagement for policy lapse prevention strategies. Addressing the client by name, such as "Dear Mr. Smith," creates a connection and acknowledges their importance. Utilizing personalized details, like referencing their specific policy type--such as a life insurance policy or auto insurance coverage--also reinforces the message's relevance. Additionally, mentioning the policy's anniversary date or highlighting any upcoming payment due dates fosters a sense of urgency while demonstrating attentiveness to their needs and situation. Engaging clients with kindness and care could encourage timely payments and minimize policy lapses.

Policy Details

Preventing a policy lapse is crucial for maintaining coverage and ensuring financial protection. Policy details such as the policy number (e.g., 12345-67890), type of insurance coverage (e.g., health, life, auto), and premium payment schedule (monthly, quarterly, annually) play a significant role in the process. Timely premium payments must be noted since a delay beyond the grace period (typically 30 days) can result in coverage termination. Policyholders should remain informed about changes in terms and conditions that can impact their coverage. Regular review of policy benefits, exclusions, and renewal terms ensures continued protection and compliance with insurer requirements. Effective communication with the insurance provider (via phone number or official website) is essential for addressing any questions regarding payment or coverage adjustments.

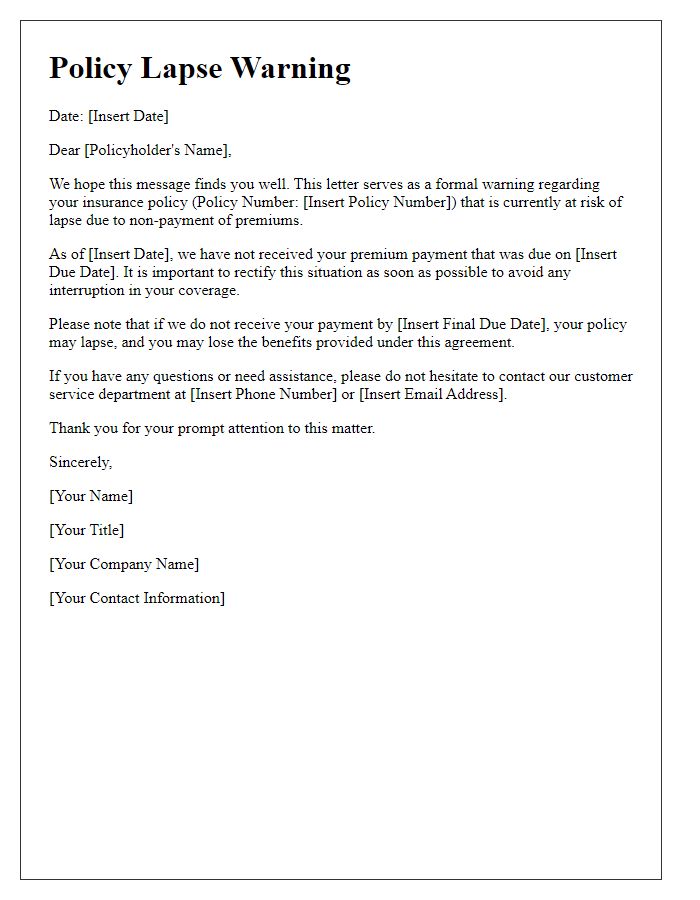

Consequences of Lapse

A policy lapse can significantly impact coverage and financial stability, resulting in a complete loss of benefits associated with the insurance contract. Lapsed policies, particularly in life insurance contracts, often leave beneficiaries without critical financial support during unforeseen events, such as a policyholder's sudden passing. Additionally, reinstatement may require navigating complex processes, including potential health examinations and higher premiums due to age increases or health changes. Essential benefits like cash value accumulation in permanent life insurance may be forfeited entirely, leading to unexpected financial strains or loss of savings. Furthermore, gaps in coverage can expose individuals to significant risks, especially in health-related incidents or property damage. Organizations and policyholders should prioritize regular reviews of their policy status to avert these severe consequences.

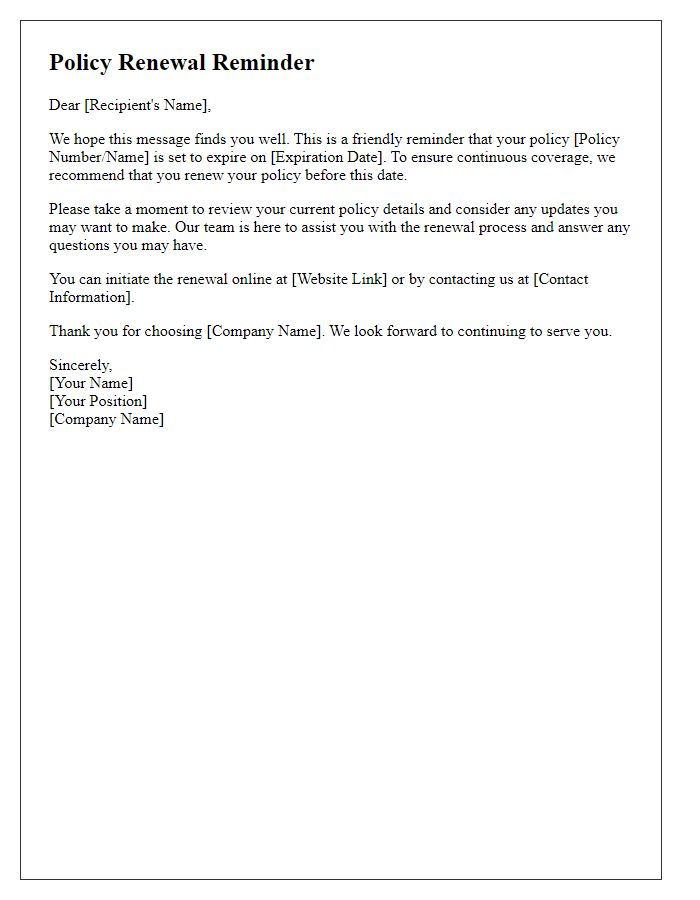

Payment Options

Policy lapse prevention strategies focus on ensuring continuous coverage by providing flexible payment options tailored to policyholders' needs. Monthly payments often enable better budgeting, while annual premiums may offer discounts for commitment. Automated payment systems, such as ACH (Automated Clearing House), ensure timely transactions directly from bank accounts, reducing the risk of lapses. Additionally, courtesy reminders via email or SMS help remind policyholders of upcoming due dates, enhancing awareness. Offering a grace period, typically 30 days, provides a safety net, allowing policyholders to fund overdue amounts without immediate loss of coverage. Engaging customer service representatives for personalized payment plans can further enhance retention, ensuring policyholders remain protected.

Contact Information

Policy lapse prevention strategies are crucial for maintaining continuous coverage and protecting policyholders. Policyholders should regularly update contact information, including email addresses, phone numbers, and mailing addresses, to ensure timely communication from insurers. Regular reminders (such as those sent 30 days prior to payment due dates) can reduce the risk of unintentional lapses. Payment methods should be reviewed to confirm adequate funding sources, including bank accounts or credit cards, which are necessary for automatic payments. Engaging with insurance agents or customer service can provide clarity on the specific terms of policies and any applicable grace periods. Establishing a scheduled review of coverage can help assess the relevance of each policy, making necessary adjustments to meet changing needs.

Read Also: Our Insured party's Blogs

Comments