When it comes to protecting your valuable van, understanding your insurance options is essential. In this article, we'll break down the key components of van insurance coverage, highlighting what you need to look out for and how policies can vary. From liability to comprehensive coverage, we'll make sense of the jargon and help you find the best fit for your needs. So, stick around and let's dive deeper into the details to ensure you're fully informed!

Image cover: Letter Template For Van Insurance Coverage Details

Letter Template For Van Insurance Coverage Details Samples

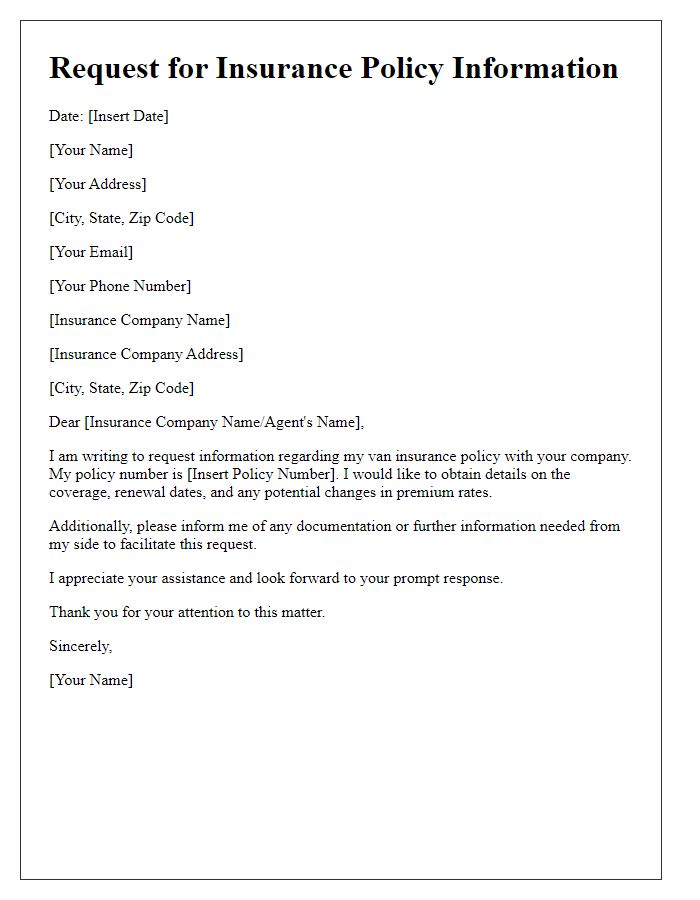

Policyholder Information

Van insurance coverage provides essential protection for vehicle owners against various risks, ensuring peace of mind on the road. The policyholder information includes key details such as the name of the individual or business entity (e.g., John Doe or ABC Logistics Ltd.), the contact information (address, phone number, email), and the registration number of the van (e.g., ABC 1234). Coverage typically encompasses liability insurance, protecting against damages to other vehicles or property up to a specific limit (e.g., $1 million), comprehensive coverage against theft and vandalism, and collision coverage to repair or replace the insured van after an accident. Additional features may include roadside assistance services (available 24/7) and coverage for personal belongings within the vehicle, enhancing the overall value of the insurance policy. The premium payment schedule, often monthly or annually, also plays a vital role in managing insurance costs effectively. Always check the terms and conditions for specific exclusions or limitations to understand fully what is covered under the policy.

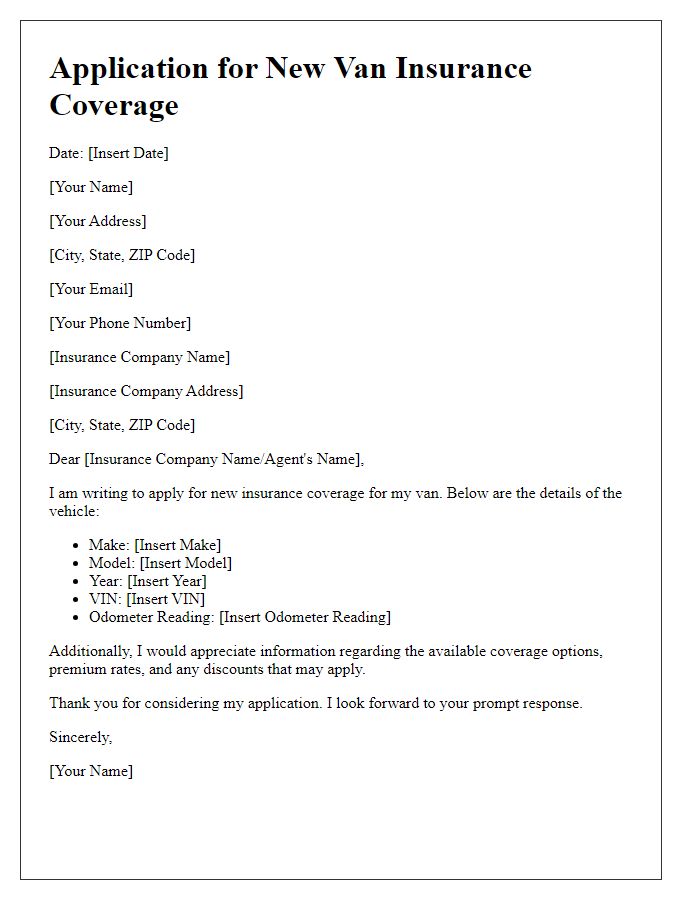

Vehicle Description

The vehicle description for van insurance coverage should include specific details such as the make and model of the vehicle, for example, a 2020 Ford Transit. Additionally, the year of manufacture plays a crucial role in determining the premium, while the vehicle identification number (VIN) provides a unique identifier for registration. Engine size, typically measured in liters (e.g., 2.0L turbocharged), influences performance and insurance rates. It is also vital to note the payload capacity, which for certain vans can be 1,500 pounds, impacting both utility and risk profile. Finally, include any modifications that may alter the van's original specifications, such as custom shelving or specialized equipment, as these can affect insurability.

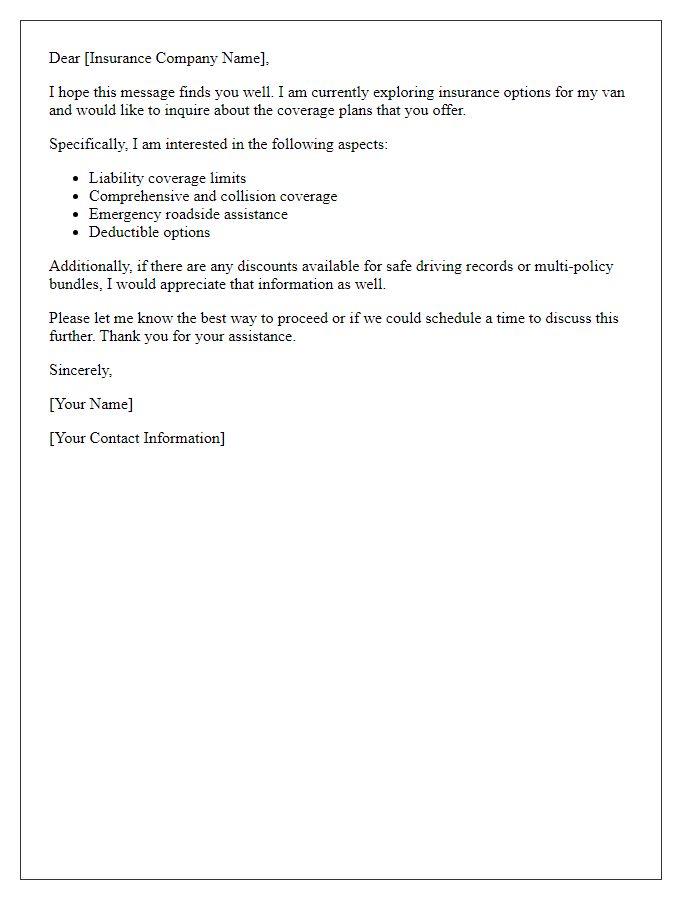

Coverage Types and Limits

Comprehensive van insurance policies provide various coverage types and limits that protect against financial loss. Collision coverage addresses damages from accidents involving other vehicles or objects, usually with a deductible ranging from $500 to $1,000. Liability coverage, essential in the United States, includes bodily injury and property damage with limits often starting at $100,000 per person and $300,000 per accident. Uninsured/underinsured motorist coverage safeguards against accidents with drivers lacking sufficient insurance, typically covering up to $100,000. Additionally, personal injury protection (PIP) covers medical expenses regardless of fault, with limits varying by state. Finally, comprehensive coverage protects against non-collision incidents like theft or natural disasters, often with varying deductibles based on the vehicle's value.

Premium and Deductible Details

Van insurance coverage involves critical components like premium rates and deductibles. Premiums, which can range from $300 to $1,500 yearly based on factors like the van's make, model, and the driver's history, are the amount you pay for coverage. This amount can vary greatly by region, for instance, urban areas might see higher premiums due to increased theft rates. Deductibles, typically between $500 and $1,000, represent the out-of-pocket amount you must cover before your insurance company pays a claim. Higher deductibles usually result in lower premium costs, which can be beneficial for responsible drivers who prefer to manage smaller risks themselves. Understanding these figures is essential for making informed insurance decisions.

Contact Information for Claims and Inquiries

Van insurance coverage includes essential details for claims and inquiries, including the insurance provider's contact information. Policyholders should have access to a dedicated claims hotline for immediate assistance. Additionally, the customer service email address facilitates communication for non-urgent inquiries. The insurance policy number, often found on the documentation, is critical for claims processing. Local office addresses allow for in-person consultations if needed. Furthermore, a claims tracking system may be available online for real-time updates on the status of claims.

Read Also: Our Insurance agent's Blogs

Comments