Are you feeling the pinch of high interest rates on your credit card or loan? Requesting a reduction in your Annual Percentage Rate (APR) could be the key to easing your financial burden and making your monthly payments more manageable. In this article, we'll guide you through a simple yet effective letter template that can help you make this request with confidence. Join us as we delve into tips and strategies to successfully lower your APR!

Image cover: Letter Template For Requesting Apr Reduction

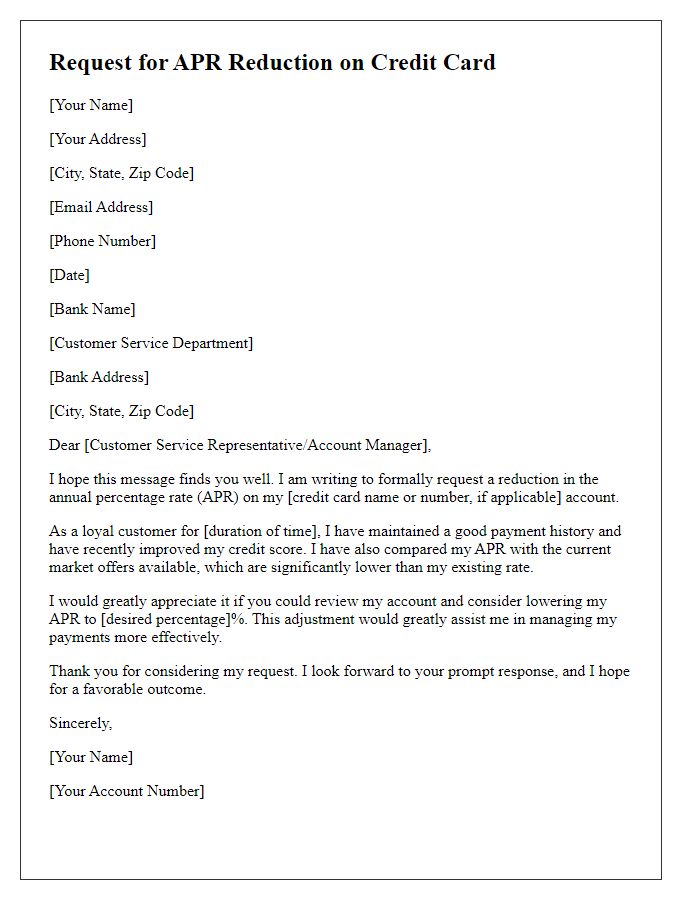

Letter Template For Requesting Apr Reduction Samples

Account Information

Requesting an APR (Annual Percentage Rate) reduction can potentially lead to significant savings for account holders. Many credit card issuers, such as Visa and Mastercard, allow consumers to negotiate their rates based on factors like payment history and credit score (which typically ranges from 300 to 850). Providing account details, including the current balance (which may average around $5,000 for consumers), payment history (ideally on-time for the last 12 months), and any relevant financial changes, can strengthen your case. Furthermore, clarifying your loyalty to the brand and any competing offers in the market, such as those from Discover or American Express, may enhance the request's effectiveness. This strategic approach demonstrates commitment and provides a rationale for the desired rate adjustment.

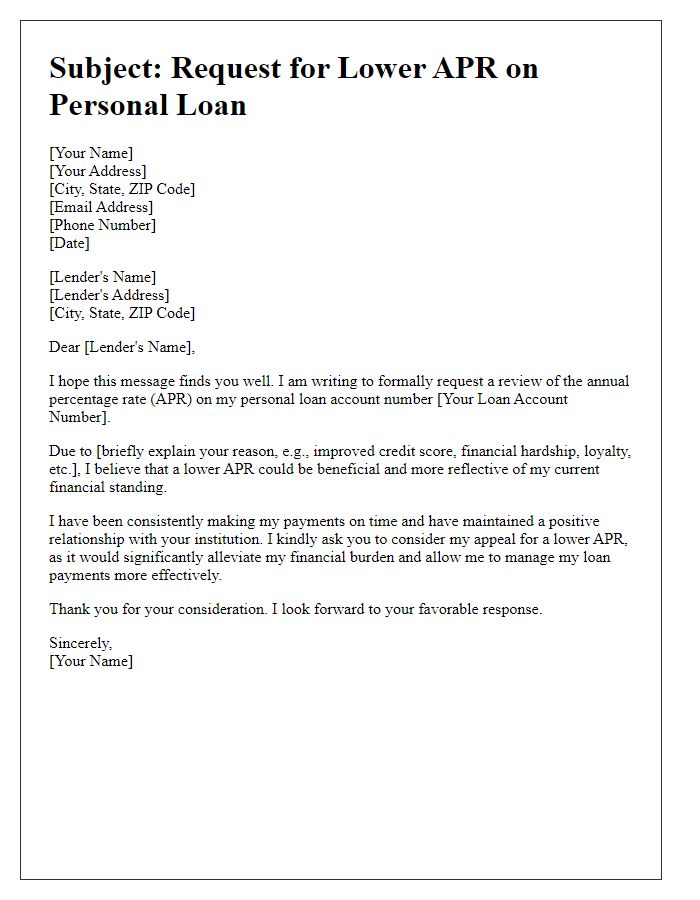

Reason for Request

Consumers often seek an APR (Annual Percentage Rate) reduction on credit cards to alleviate financial burdens caused by high-interest rates. High APRs can result from various factors such as credit score fluctuations, market interest rates, or even promotional periods ending. For example, a credit card with an APR of 24% can significantly increase the amount of interest paid on an outstanding balance, leading to difficulties in repayment. A formal request for a reduction might outline a consistent payment history over the last 12 months, a stable income, or an improved credit score, all of which can strengthen the case for negotiation. In many cases, similar requests have been granted by financial institutions, such as those in New York that follow regulations established by the Consumer Financial Protection Bureau (CFPB), promoting fair lending practices and consumer rights.

Credit History Highlights

Credit history provides a comprehensive overview of an individual's borrowing behavior and repayment patterns over time, showcasing significant events such as the opening of credit accounts, payment punctuality, and overall debt management. In the United States, a FICO score (ranging from 300 to 850) serves as a key indicator, with higher scores reflecting more responsible credit usage. Consistent on-time payments, typically defined as payments made within 30 days of the due date, positively impact this score. Major creditors, such as nationwide banks and credit unions, regularly assess this score during routine account evaluations, determining interest rates for loans and credit cards. A strong credit history, including a low credit utilization ratio--ideally below 30%--and fewer recent hard inquiries, can strengthen the case for a favorable APR reduction, enhancing borrowing affordability.

Financial Responsibility

To achieve financial stability, individuals often seek methods to lower their Annual Percentage Rate (APR) on existing loans or credit cards. A significant portion of consumers grapple with high-interest rates, particularly those exceeding 20%. By contacting financial institutions, such as national banks or credit unions, borrowers can formally request APR reductions based on timely payment history and improved credit scores--often above 700. Strategic timing, such as initiating requests during promotional periods or milestones like anniversaries of accounts, can enhance the likelihood of approval. Personal financial management plays a crucial role in demonstrating responsibility, ultimately fostering healthier credit profiles and minimizing long-term debt burdens.

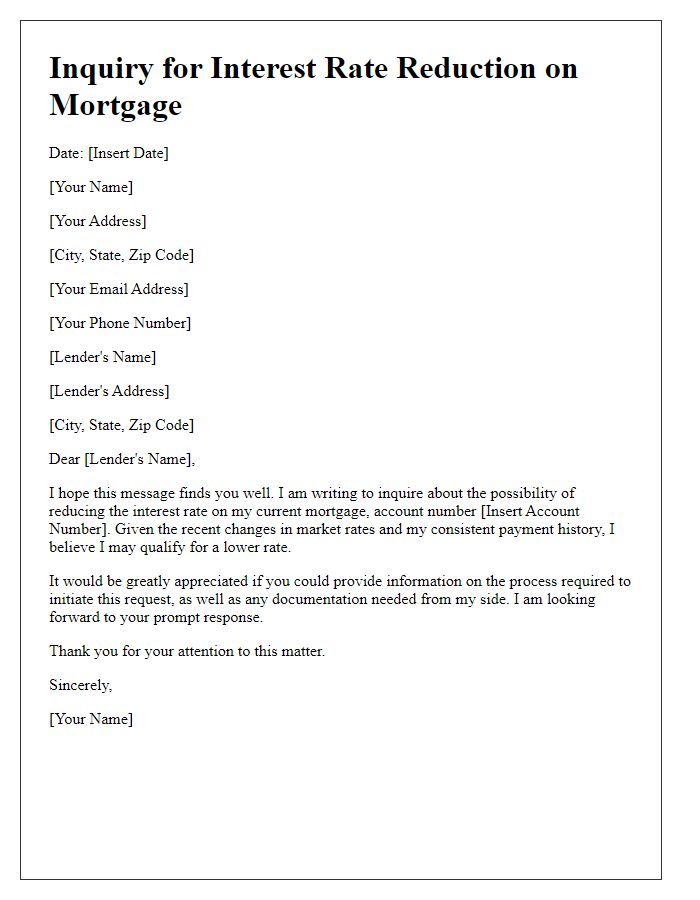

Contact Information

A request for an Annual Percentage Rate (APR) reduction can be made effectively by including essential details such as personal identification (full name, address), account number (unique identifier for the creditor), contact number (best way to reach you), and email address (for written communication). Clearly stating the specific loan type (credit card, auto loan, mortgage) and current APR percentage (e.g., 19.99%) assists in outlining the request. Highlighting relevant financial milestones, such as timely payment history (a specific number of months, for example, 12 continuous payments) and improved credit score metrics (an increase from 680 to 720), strengthens the reasoning for the rate reduction. Including a reference to competitive rates (average market APR for similar loans, around 12% to 15%) adds weight to the appeal.

Read Also: Our Credit applicant's Blogs

Comments