Transitioning to IAS/IFRS reporting can seem daunting at first, but it opens up a world of opportunities for companies seeking to enhance transparency and comparability in their financial statements. Embracing these international standards not only aligns businesses with global best practices but also fosters greater trust with stakeholders. As organizations navigate this significant change, understanding the processes and benefits involved becomes essential for a smooth transition. If you're ready to learn more about how to make this switch effectively, read on!

Image cover: Letter Template For Ias/Ifrs Reporting Transition

Letter Template For Ias/Ifrs Reporting Transition Samples

Regulatory Compliance

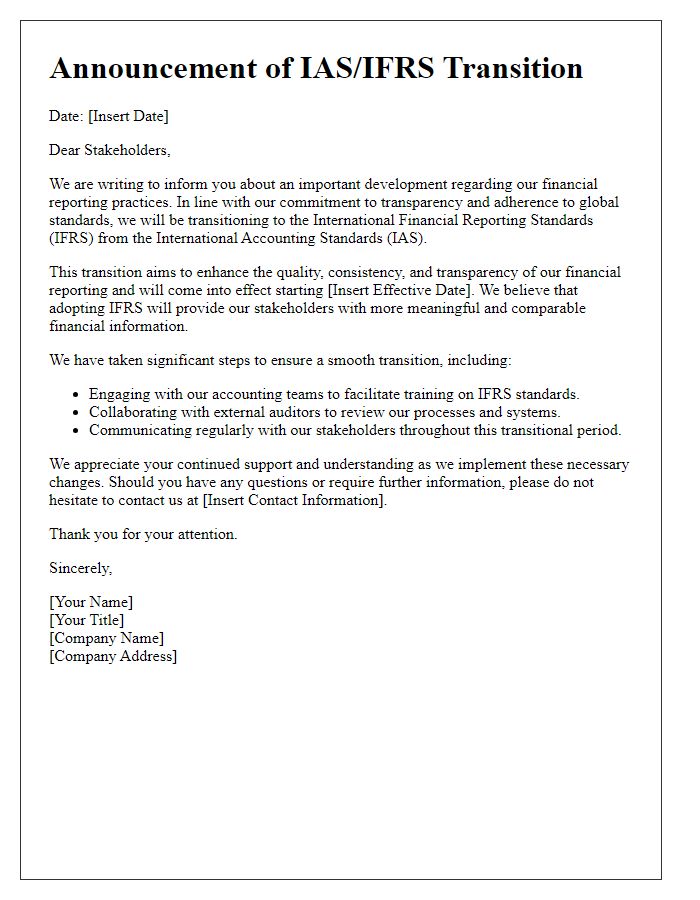

The transition to International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS) mandates comprehensive regulatory compliance, impacting organizations globally. Key regulations (such as IFRS 9 for financial instruments and IFRS 15 for revenue recognition) require entities to adjust their accounting policies and financial reporting practices. This transition process may involve extensive training for finance teams, revised accounting systems, and rigorous internal controls to ensure accuracy. Companies must also review and assess the implications for stakeholders, including investors and regulatory bodies, ensuring transparent communication throughout the transition process. Adherence to deadlines, such as mandatory reporting under IFRS for financial years beginning on or after January 1, 2018, solidifies the importance of meticulous planning and execution in meeting compliance requirements.

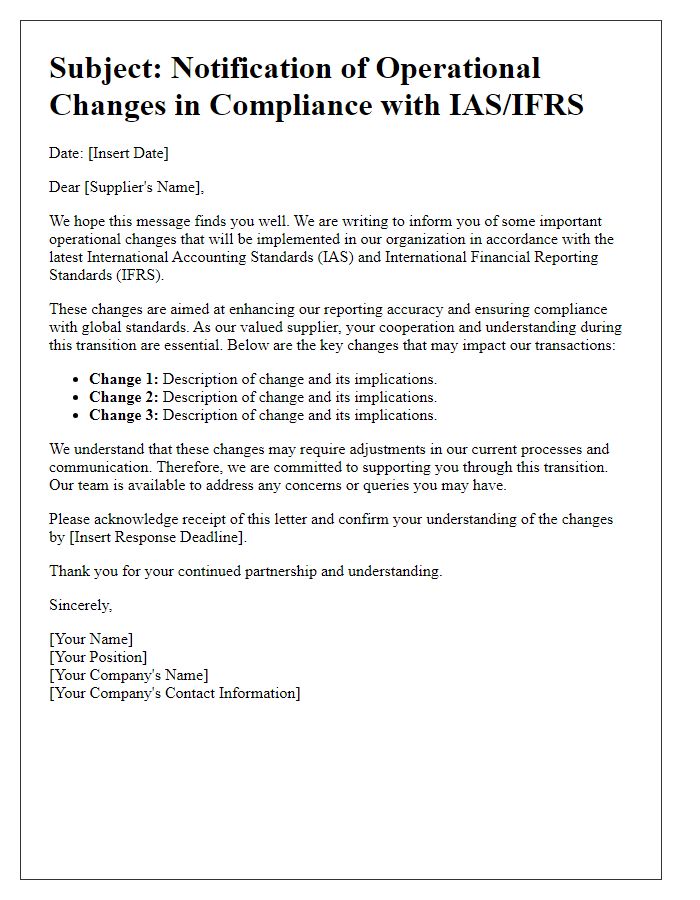

Stakeholder Communication

Effective stakeholder communication during the transition to International Accounting Standards (IAS) or International Financial Reporting Standards (IFRS) is crucial for ensuring transparency and maintaining trust. Stakeholders, including investors, regulatory bodies, and employees, require clear information on changes to financial reporting processes, timelines for implementation, and impacts on financial statements. Detailed updates should include specific transition dates (e.g., January 1, 2024), explanations of key differences between local GAAP and IFRS, and implications for financial metrics such as earnings per share (EPS) and revenue recognition. Ongoing training sessions, webinars, and informational brochures can facilitate understanding of the new reporting requirements. Regular newsletters or emails should outline milestones achieved throughout the transition process, and feedback mechanisms must be established for stakeholders to raise concerns or questions, ensuring continuous engagement and support.

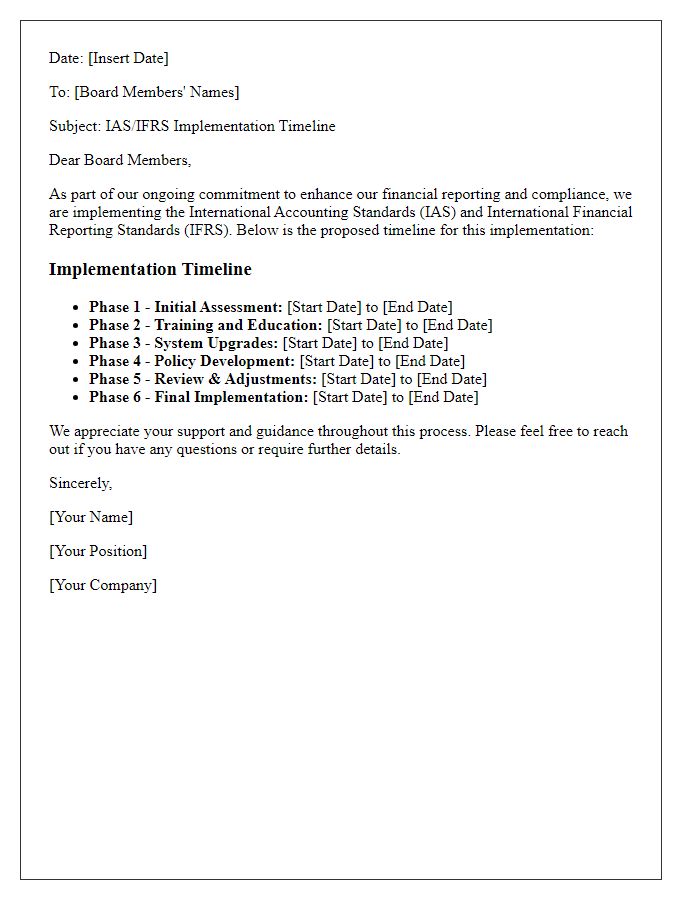

Transition Timeline

The transition timeline for IAS (International Accounting Standards) and IFRS (International Financial Reporting Standards) reporting encompasses several critical milestones ensuring compliance and effective implementation. Initial assessments typically commence six to twelve months before the transition date, allowing organizations to evaluate existing accounting practices against the new standards. By month three, comprehensive training sessions for accounting personnel are crucial, focusing on understanding key changes and their implications for financial statements. A pilot phase follows, usually lasting one to two months, during which sample financial reports are generated to test the new reporting framework. Subsequent months involve rigorous testing and reviewing financial systems for gaps in compliance, leading to final adjustments and the formulation of the full transition report. The actual transition occurs at the designated cutoff date, often aligned with the fiscal year-end, with all financial statements being prepared in accordance with IAS/IFRS guidelines within the following weeks. Effective communication with stakeholders, including regulators and investors, is essential throughout this process to ensure transparency and understanding of the changes being implemented.

Accounting Policy Changes

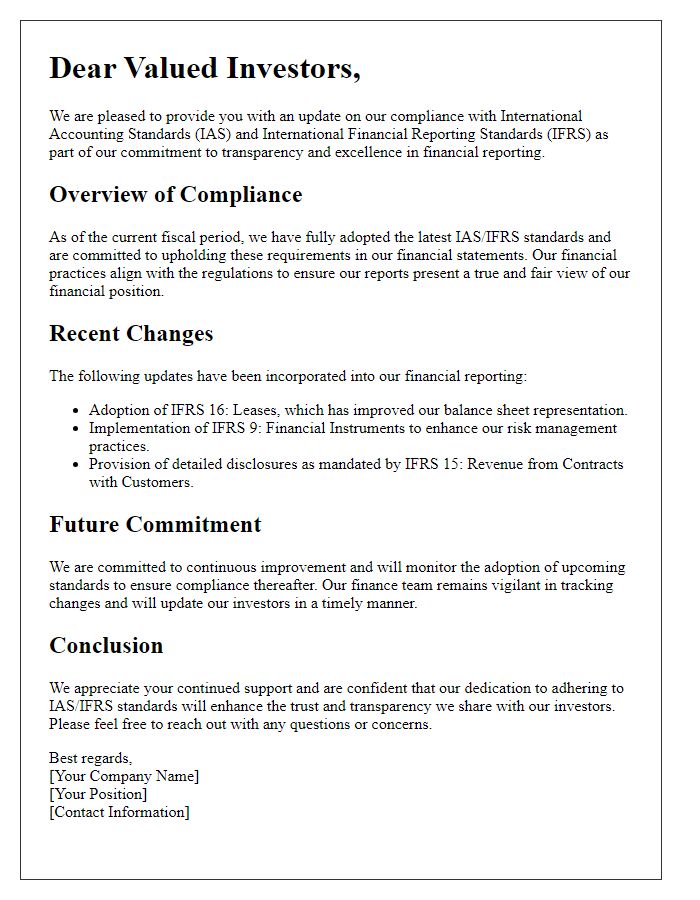

The transition to IFRS (International Financial Reporting Standards) from IAS (International Accounting Standards) requires significant changes in accounting policies. Companies must adopt new standards such as IFRS 15 regarding revenue recognition and IFRS 16 for lease accounting, which affect financial statements and disclosures. For instance, under IFRS 16, companies must recognize lease liabilities and corresponding right-of-use assets on their balance sheets, impacting key financial metrics like total liabilities and asset turnover ratios. Entities should also provide detailed reconciliations of prior period financial information to illustrate the effects of these transitions on net income and equity. It is essential to communicate with stakeholders, preparing them for changes in financial reporting practices and ensuring compliance with the relevant regulatory requirements by deadlines established by governing bodies such as the International Accounting Standards Board.

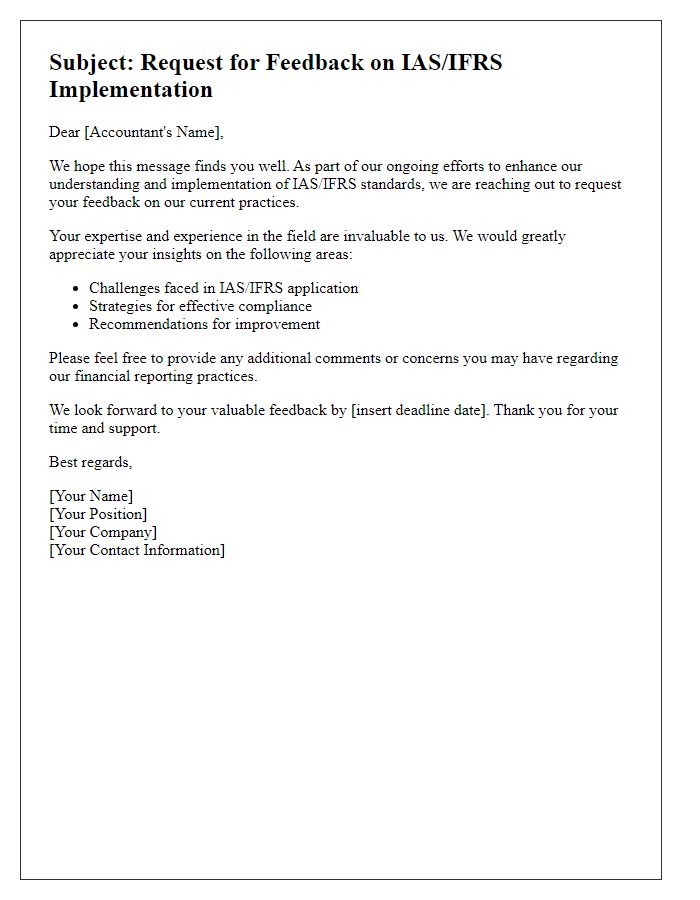

Staff Training and Resources

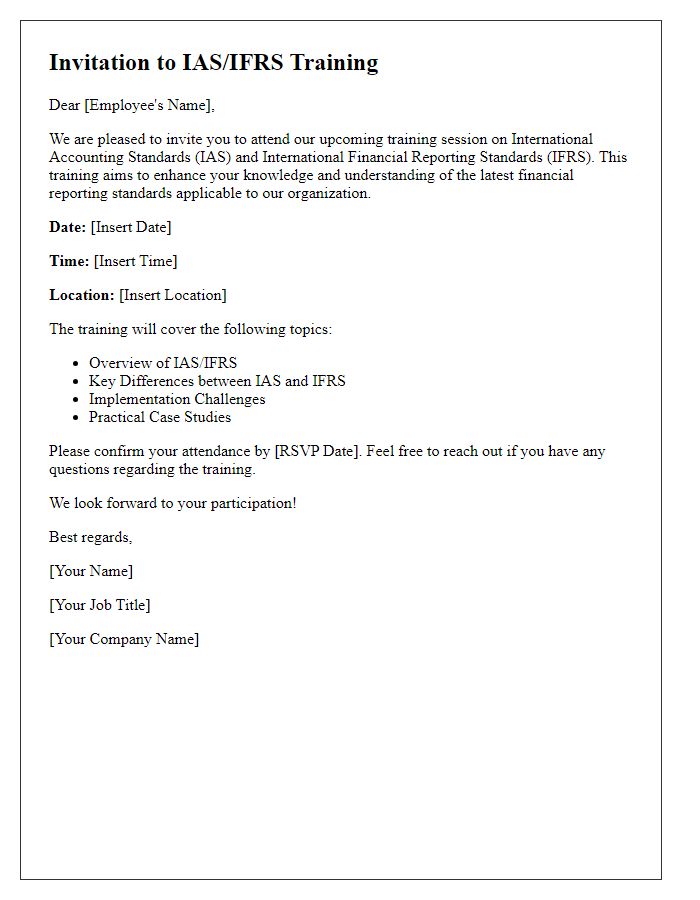

Implementing the transition to International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS) requires comprehensive staff training and access to relevant resources. Training sessions should focus on key principles of IAS/IFRS, such as revenue recognition (IFRS 15), financial instrument measurement (IFRS 9), and lease accounting (IFRS 16). Ideal training durations range from half-day workshops to week-long seminars, ensuring thorough understanding of new standards. Additional resources should include updated financial accounting textbooks, online courses, and access to accounting software supporting IFRS reporting. Regular refresher courses, along with webinars featuring industry experts, will sustain knowledge retention and application. Integration of assessment tools is essential to measure staff proficiency and adherence to the new reporting framework. Tracking progress through performance metrics will aid in identifying training gaps and addressing them promptly.

Read Also: Our Accounting firm's Blogs

Comments