Are you thinking about protecting your coastal property? Understanding the ins and outs of coastal property insurance is crucial for keeping your investment safe from unpredictable weather and natural disasters. This guide will walk you through the essential coverage options tailored for properties near the shore. Dive into the details and discover how you can secure your coastal haven by reading more!

Image cover: Letter Template For Coastal Property Insurance Information

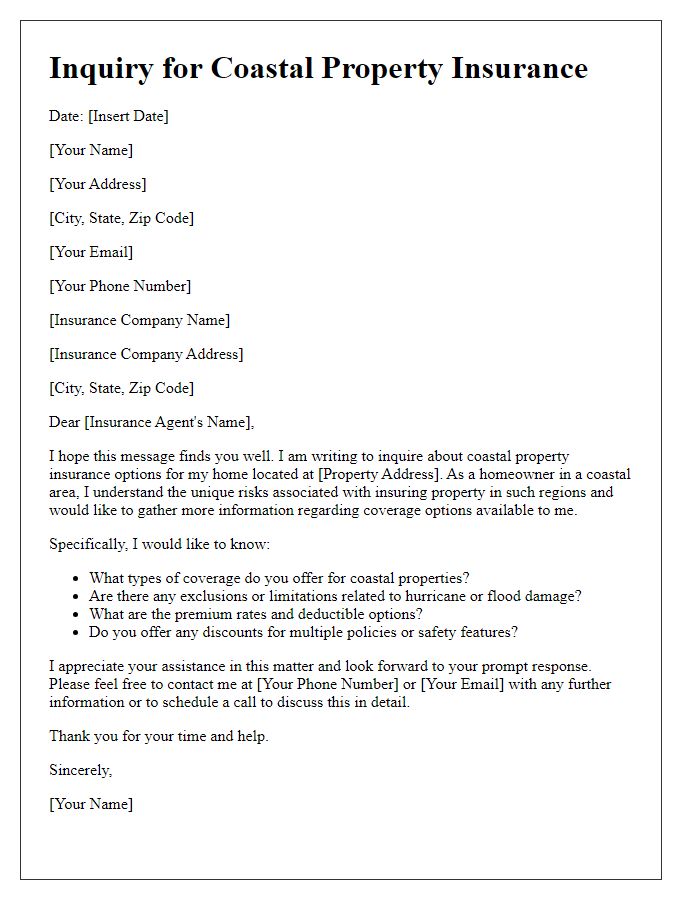

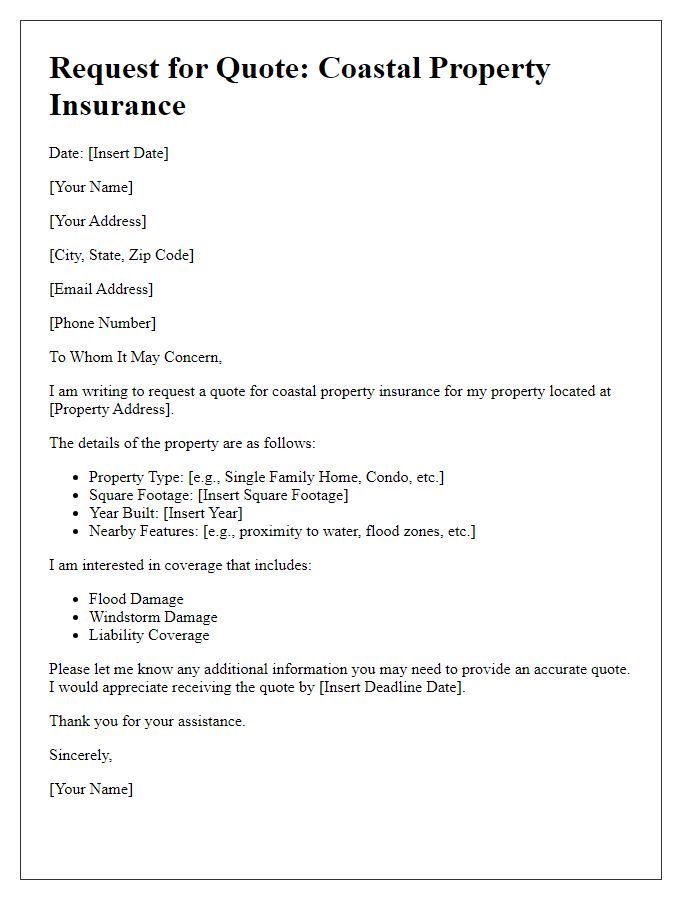

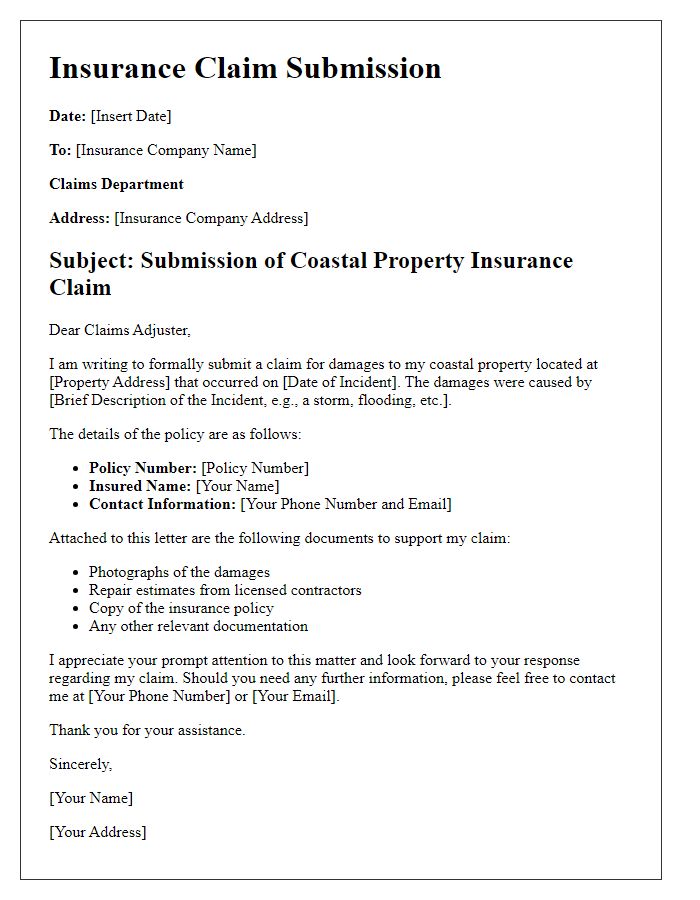

Letter Template For Coastal Property Insurance Information Samples

Coverage Overview

Coastal property insurance provides essential protection for properties located near coastlines, such as beachfront homes in places like Florida and California. This type of insurance typically covers various risks associated with coastal living, including wind damage from hurricanes (with winds exceeding 74 miles per hour), flooding caused by storm surges or heavy rainfall, and erosion due to sea-level rise. Policies often include special endorsements for additional risks, ensuring proper coverage for valuable assets like homes, boats, and personal belongings. Regular assessments of property values are necessary to maintain adequate coverage limits, particularly given fluctuating market conditions. Coastal property insurance is crucial for safeguarding investments against the unpredictable impacts of the ocean and severe weather events.

Property Details

Coastal property insurance provides essential coverage for homes located in vulnerable coastal regions, such as the Gulf Coast in the United States. These areas are susceptible to severe weather events, including hurricanes and tropical storms, which can result in significant property damage. Premium rates can vary dramatically based on factors including property age, construction type, and proximity to the shoreline. For instance, homes built before 2000 may have higher premiums due to outdated building codes, whereas modern properties with elevated foundations may enjoy reduced rates due to improved resilience against flooding. Additionally, insurance policies typically cover elements such as wind damage, storm surge flooding, and erosion, ensuring comprehensive protection for property owners in regions like Florida, Texas, and North Carolina. Understanding the specific terms of coverage is crucial for maintaining financial security and safeguarding valuable coastal investments.

Risk Assessment

Coastal property insurance undergoes rigorous risk assessment to gauge vulnerabilities associated with geographic features, such as hurricane-prone areas along the Atlantic Ocean, or flood zones identified by Federal Emergency Management Agency (FEMA) maps. These assessments consider factors like elevation, which affects potential water intrusion, proximity to the shoreline, and historical data on storm surges and tidal flooding. Properties located within designated special flood hazard areas (SFHAs) face increased premiums due to higher risk levels, often exceeding 2 feet above base flood elevation in severe storm scenarios. Insurance policies typically require detailed inspections to evaluate structural integrity, material resilience against high winds (potentially up to 150 miles per hour during severe weather events), and compliance with local building codes. Additionally, risk assessments factor in mitigation measures such as installation of storm shutters and elevated foundations, which can influence coverage options and premium rates.

Policy Premiums

Coastal property insurance policies offer crucial coverage for homes located in proximity to oceans, seas, or large lakes, addressing specific risks such as flooding and hurricanes. Annual policy premiums can vary significantly based on factors like geographic location, with Gulf Coast states often seeing higher rates due to frequent storm activity. The average premium across coastal regions can range from $1,000 to over $3,000, heavily influenced by property value, elevation above sea level, and structural characteristics. Additionally, insurers may consider local regulations and historical data on natural disasters, resulting in tailored policies that provide essential financial protection against the devastating impacts of severe weather events. Understanding these factors is vital for homeowners in securing appropriate levels of insurance coverage.

Claim Process and Contacts

Coastal property insurance encompasses critical components for homeowners near oceanic regions, such as coastal flooding and storm damage. The claims process typically starts with documenting damages through detailed photographs and notes. Homeowners must report incidents to their insurance provider, often within a specific timeframe (usually within 30 days). Essential contact numbers for local claims adjusters, emergency service providers, and the National Flood Insurance Program (NFIP) should be readily available. Review local regulations and consult the policy's fine print regarding deductibles and limits, especially for windstorm-related claims, which can significantly impact the settlement amount. Additionally, understanding factors like the region's risk ratings and historical storm data can help in making informed decisions during the claims process.

Read Also: Our Real estate agent's Blogs

Comments