Are you considering a property insurance evaluation but unsure where to start? Understanding your coverage is essential for protecting your valuable assets and ensuring peace of mind. In this article, we'll break down the key elements of a property insurance evaluation and provide helpful tips to make the process seamless. So, let's dive in and empower yourself with the knowledge you need to safeguard your property effectively!

Image cover: Letter Template For Property Insurance Evaluation

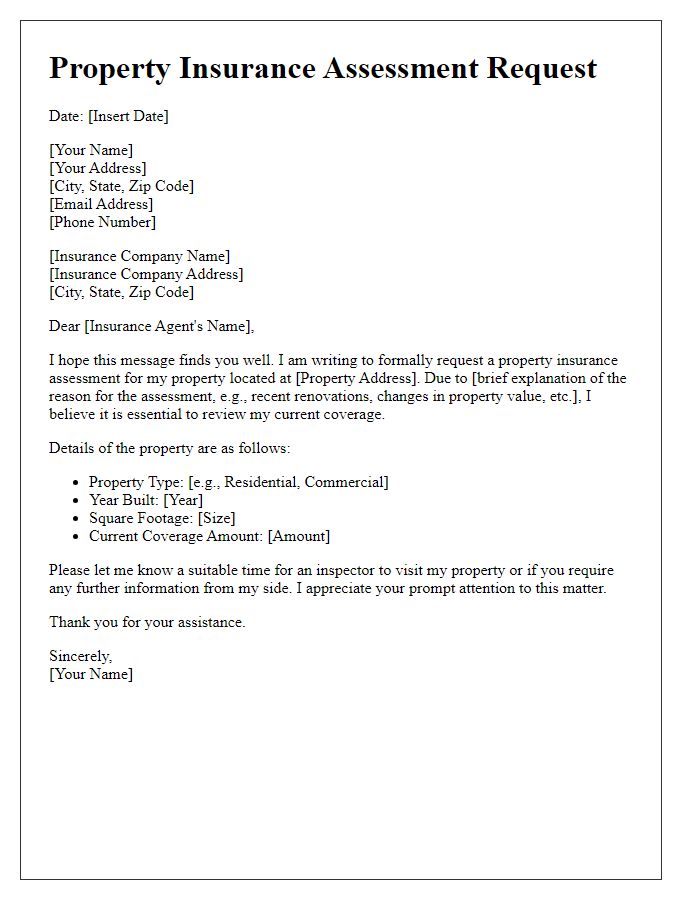

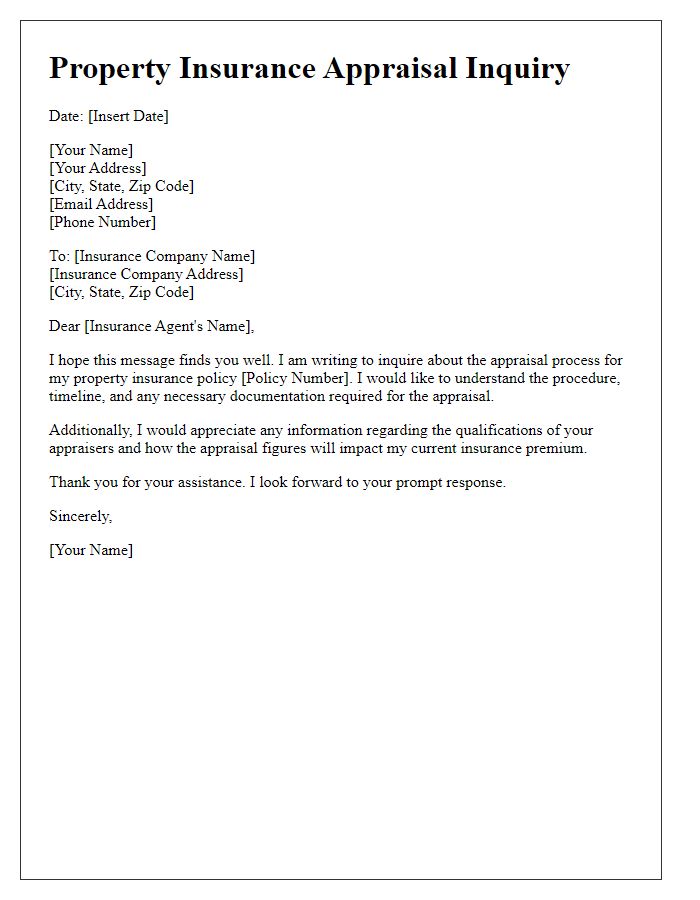

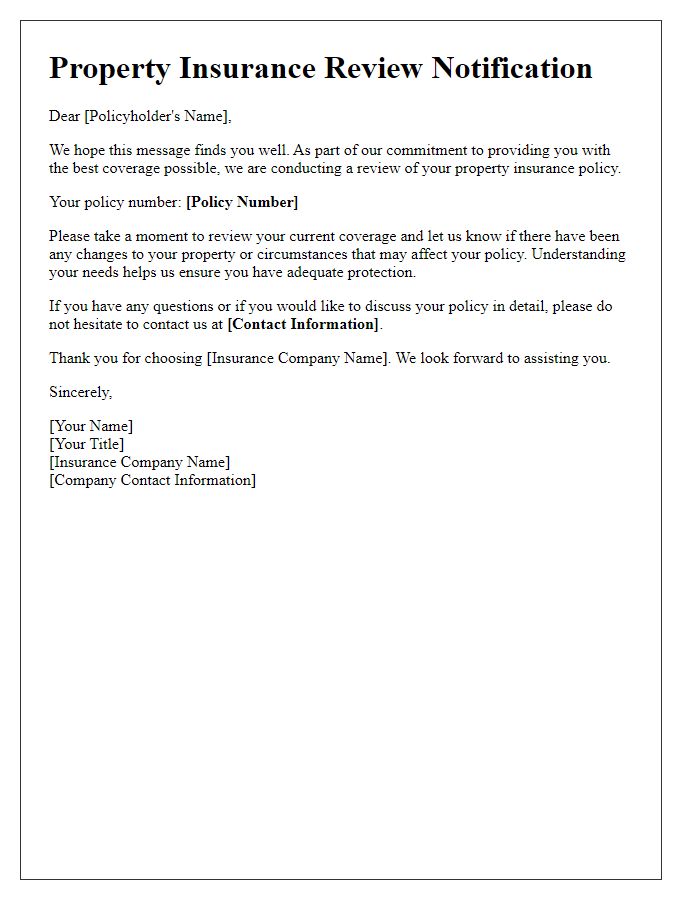

Letter Template For Property Insurance Evaluation Samples

Accurate Property Description

Accurate property description plays a crucial role in property insurance evaluation. Detailed information regarding the property type, such as single-family home, condominium, or commercial property, affects premium calculations. Including exact square footage (for example, 2,500 square feet) provides essential context for assessing value. Location specifics, such as the property's proximity to coastal areas vulnerable to hurricanes or urban settings prone to theft, are vital for risk assessment. Year built (e.g., 1995), renovation history, and types of building materials (such as brick or wood) influence the rebuild cost. Features like swimming pools, detached garages, and security systems, further enhance understanding of the property's unique characteristics and potential liabilities. Complete documentation with photos can significantly improve the accuracy of the insurance evaluation process.

Policy Coverage Details

A property insurance evaluation requires a comprehensive review of policy coverage details, including various key aspects such as dwelling coverage, personal property coverage, liability protection, and additional living expenses. Dwelling coverage typically encompasses the structure of the home, with limits often set at the replacement cost or actual cash value, depending on the policy type. Personal property coverage generally covers the items within the home, including furniture and electronics, with limits varying based on valuation methods. Liability protection serves to protect homeowners from legal claims resulting from injuries or property damage, with typical coverage limits ranging from $100,000 to $1 million. Additional living expenses coverage assists policyholders in covering costs associated with temporary housing when the insured property is uninhabitable due to a covered event, with limits based on the policy agreement. Understanding these components ensures adequate protection against financial loss in case of unforeseen incidents.

Risk Assessment Summary

Risk assessment in property insurance often involves a thorough evaluation of various factors that can influence insurance premiums. For residential properties, aspects such as location can play a significant role, especially areas prone to natural disasters like hurricanes (Florida hosts annual seasons) or floods (New Orleans' historical vulnerability). Property age and condition also factor into evaluations, with older structures, particularly those built before 1980 (often lacking modern safety codes), possibly facing higher premiums due to outdated electrical and plumbing systems. Further analysis includes assessing security features like alarm systems and sprinkler systems, which can significantly mitigate risks. Additionally, nearby amenities such as fire departments (response times measured in minutes) and local crime rates contribute to an overall risk profile. Statistical models often aggregate these variables to predict the likelihood of claims, influencing the insurer's decision-making process.

Valuation of Property and Contents

Property insurance evaluations play a crucial role in determining the financial protection offered by insurance policies for personal and commercial properties. Accurate valuation ensures that the insured property, including the structure, land, and contents (such as furniture, electronics, and appliances), reflects an appropriate replacement cost, which can vary based on location, condition, and market trends. For instance, properties in high-demand urban areas may require reassessments of values every few years (often every 3-5 years) to align with fluctuating real estate prices. Comprehensive evaluations often include professional appraisals, itemized assessments of personal belongings, and detailed records of renovations or improvements, ensuring that policyholders receive adequate compensation in case of disasters like fire, theft, or natural disasters. This proactive approach mitigates financial risks and promotes peace of mind for property owners.

Claims History and Analysis

Property insurance evaluation requires a comprehensive review of claims history and analysis to assess risk exposure. A claims history, often recorded in a claims database, provides critical information about previous incidents related to property damage, theft, or liability claims. This data, typically covering the last five years, helps underwriters determine patterns, such as frequency and severity of claims. Additionally, the analysis may include geographic factors, such as location in high-risk areas like flood plains or zones prone to wildfires, which significantly impact insurance premiums. Furthermore, specific details like the type of property (residential vs. commercial), construction materials, and installed safety features (security systems, smoke detectors) play pivotal roles in mitigating risks and can influence the overall evaluation of property insurance policies.

Read Also: Our Real estate agency's Blogs

Comments