Are you looking to make the most of your hard-earned money through tax-efficient investment planning? Navigating the world of finance can be overwhelming, but with the right strategies, you can maximize your returns while minimizing your tax burden. In this article, we'll explore various approaches to smart investing that not only align with your financial goals but also take advantage of tax benefits. Join us as we dive deeper into the essentials of tax-efficient investing and discover actionable tips to enhance your financial future!

Image cover: Letter Template For Tax-Efficient Investment Planning

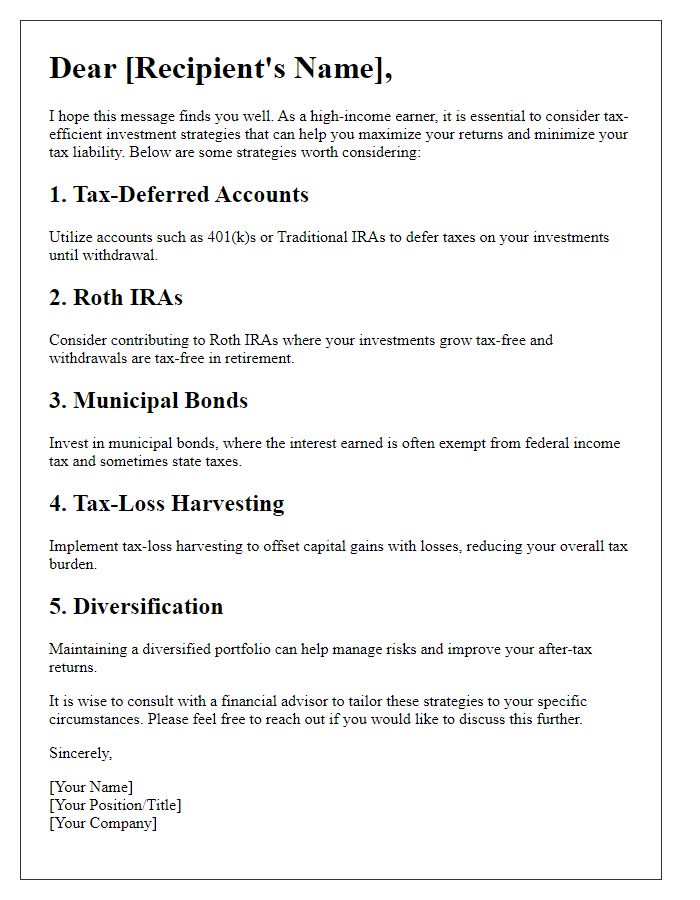

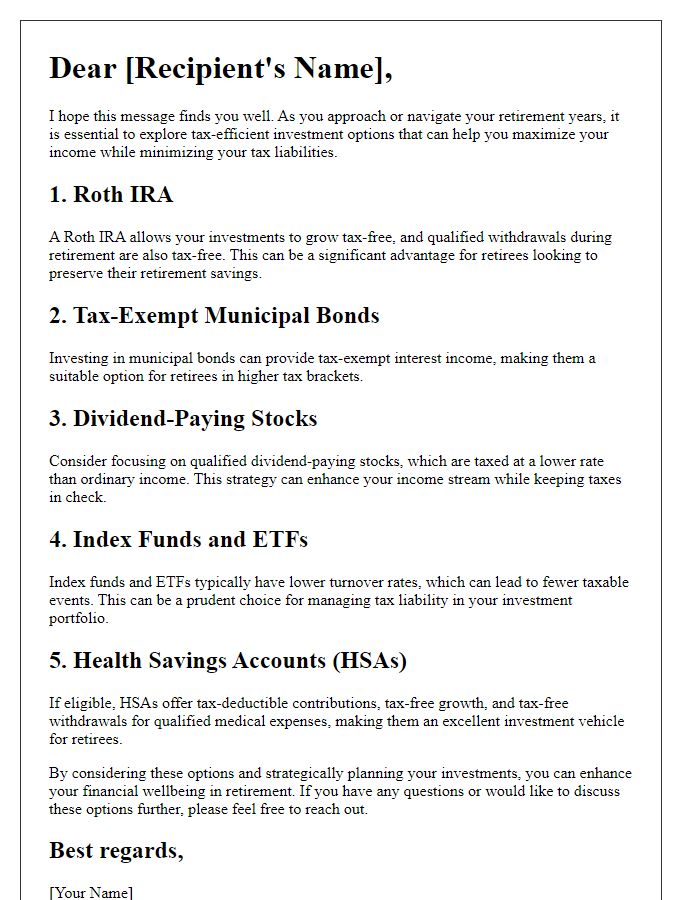

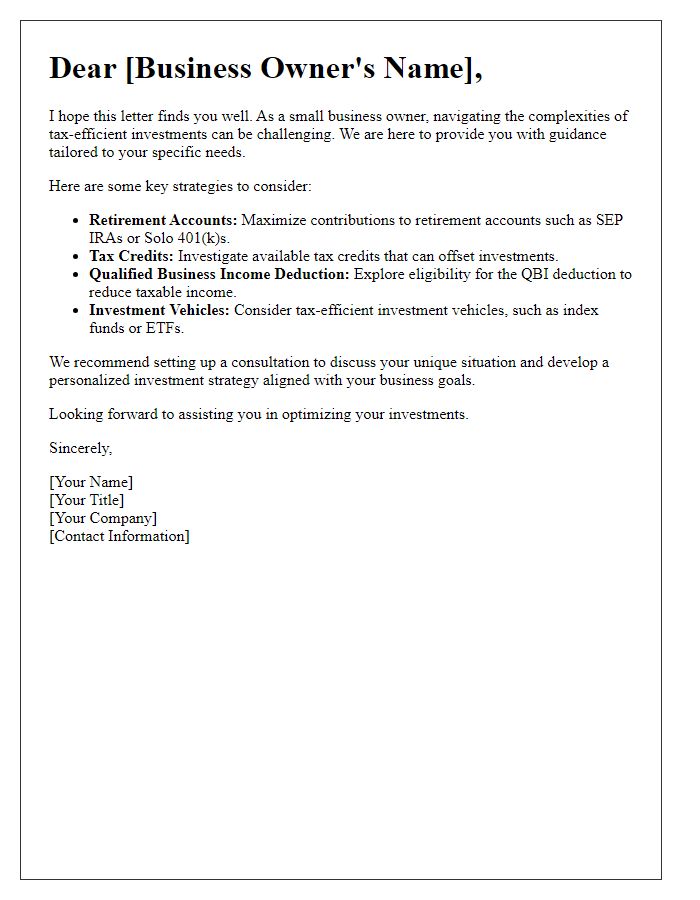

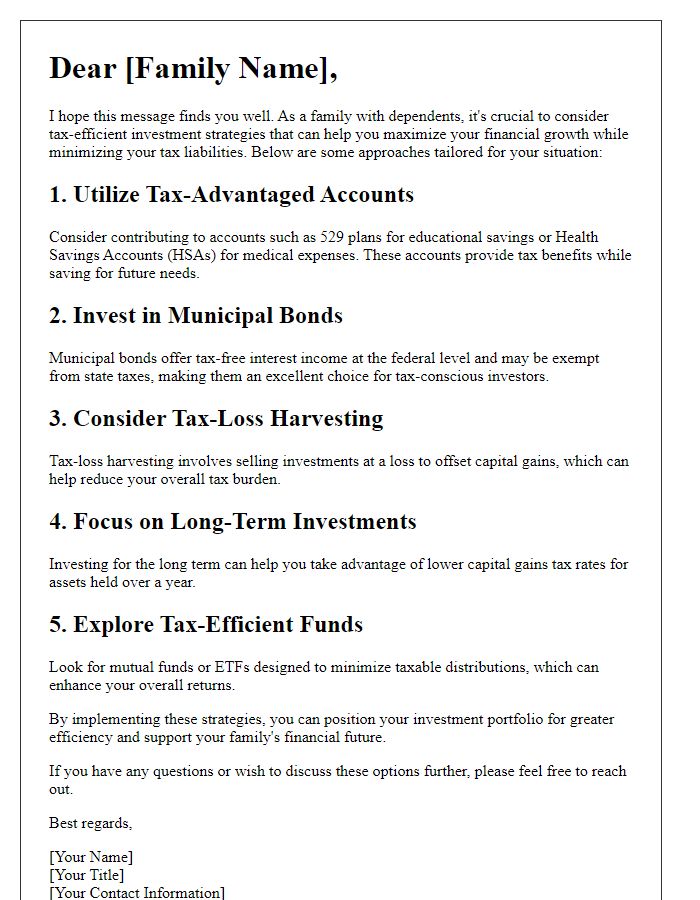

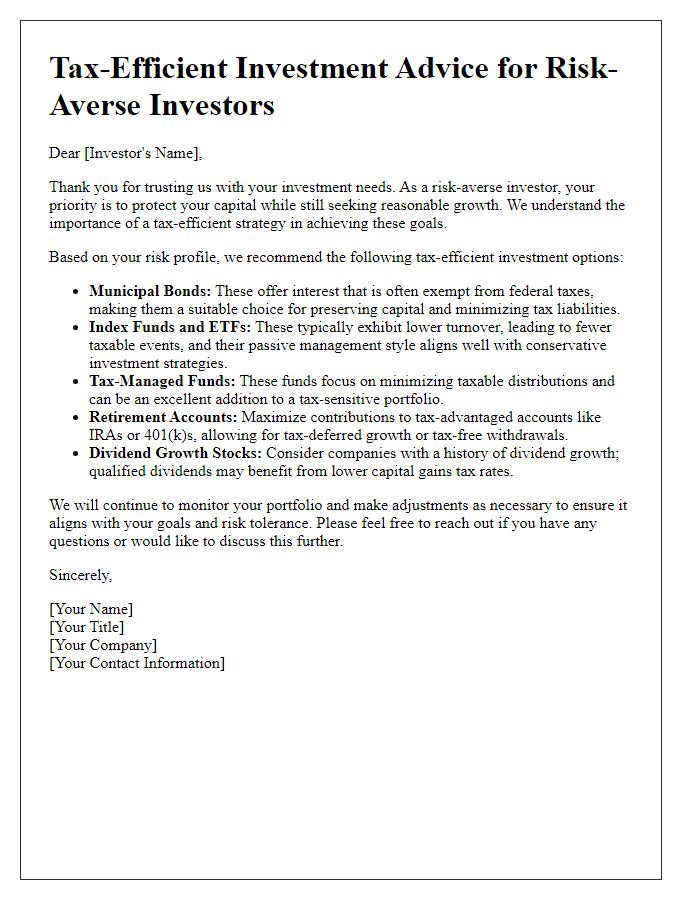

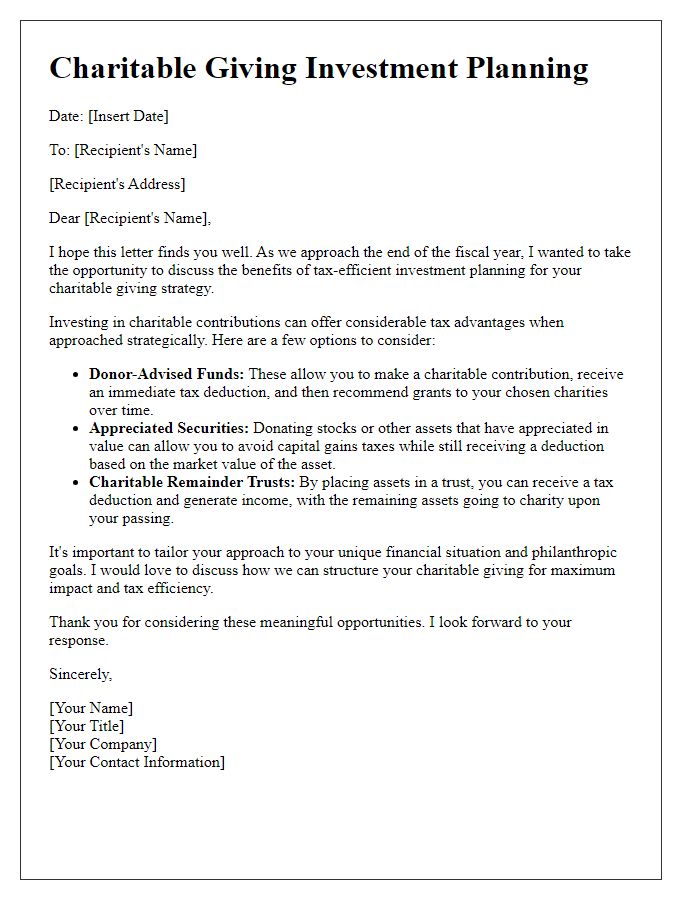

Letter Template For Tax-Efficient Investment Planning Samples

Goal definition and prioritization

Tax-efficient investment planning involves establishing clear financial goals, prioritizing them based on individual circumstances, and considering long-term implications. Key financial objectives, such as retirement savings, children's education funding, or purchasing a primary residence, significantly influence investment strategies. Evaluating timelines for these goals, whether short-term (under five years) or long-term (over twenty years), is crucial for selecting appropriate investment vehicles, such as tax-advantaged accounts (like IRAs or 401(k)s) or taxable brokerage accounts. Understanding the impact of tax brackets, capital gains, and dividend taxes on returns shapes decision-making, ensuring that investments align with both financial aspirations and tax efficiency. Integration of risk tolerance assessments and diversification strategies enhances the ability to achieve these goals while minimizing tax liabilities.

Asset allocation strategies

Effective asset allocation strategies are crucial for tax-efficient investment planning, particularly in the context of individual portfolios in the United States. Diversifying investments across various asset classes, including equities (stocks), fixed-income securities (bonds), and alternative investments (real estate, commodities), typically leads to a more balanced risk-reward profile. Utilizing tax-advantaged accounts such as Individual Retirement Accounts (IRAs) or Health Savings Accounts (HSAs) can enhance tax efficiency by allowing investments to grow tax-deferred or tax-free. For instance, placing high-dividend stocks in tax-advantaged accounts can mitigate taxable income, while allocating municipal bonds, which typically offer tax-free interest, within taxable accounts can maximize returns on investment. Frequent rebalancing (adjusting the proportion of asset classes) ensures that the portfolio remains aligned with the investor's risk tolerance and long-term financial goals.

Tax implications and incentives

Tax-efficient investment planning involves strategies to maximize after-tax returns while minimizing tax liabilities. Common investment accounts, such as Individual Retirement Accounts (IRAs) and 401(k)s, offer tax advantages like deferred taxes or tax-free withdrawals, depending on the account type. Different investment vehicles, such as municipal bonds, provide tax-exempt interest at the federal level, while capital gains from long-term holdings benefit from reduced tax rates compared to short-term trades. Understanding the tax brackets, which range from 10% to 37% in the United States as of 2023, allows investors to strategically place assets to minimize exposure to higher tax rates. Additionally, analyzing local and state tax implications, particularly for residents of high-tax regions like California or New York, is crucial for comprehensive planning. Estate planning strategies may also provide tax incentives, such as the annual gift tax exclusion, allowing individuals to transfer wealth efficiently without significant tax burdens.

Risk management assessment

Tax-efficient investment planning involves a comprehensive risk management assessment to identify potential liabilities and optimize returns. Strategies such as utilizing tax-advantaged accounts (like IRAs or 401(k)s in the United States) can mitigate tax burdens while capitalizing on market opportunities. Understanding personal risk tolerance is crucial, as it influences investment choices across various asset classes, from equities (stocks) to fixed income (bonds). Monitoring economic indicators, such as inflation rates or interest rates, helps in adjusting strategies accordingly. Engage with financial advisors well-versed in tax legislation changes, such as those from the Tax Cuts and Jobs Act, for tailored recommendations. Diversification of investments reduces risks associated with market volatility, ensuring better long-term stability. Regular portfolio reviews will enhance performance tracking and support achieving financial goals effectively.

Portfolio performance monitoring

Monitoring portfolio performance is essential for effective tax-efficient investment planning. Regular evaluations of holdings, including stocks, bonds, and mutual funds, allow investors to assess capital gains and losses, crucial for tax implications. Reviewing performance metrics, such as the return on investment (ROI) percentage relative to market benchmarks like the S&P 500, provides insights into asset allocation efficiencies. Tools like tax-loss harvesting can aid in offsetting gains from profitable investments while optimizing overall tax liabilities. Additionally, keeping abreast of legislative changes affecting investment taxation, such as those introduced in the Tax Cuts and Jobs Act of 2017, ensures adherence to compliance and maximization of financial returns. By implementing these strategies, investors can strategically enhance their portfolios while minimizing tax burdens.

Read Also: Our Financial consultancy's Blogs

Comments