Are you feeling overwhelmed by your credit score and looking for ways to improve it? You're not aloneâmany people face challenges when it comes to their credit, but the good news is that there are effective strategies you can implement today. From understanding the importance of timely payments to diversifying your credit mix, each step you take can lead to significant changes in your financial health. Join us as we explore actionable tips and insights to boost your credit scoreâlet's dive in!

Image cover: Letter Template For Credit Score Improvement Strategies

Letter Template For Credit Score Improvement Strategies Samples

Personal Financial Analysis

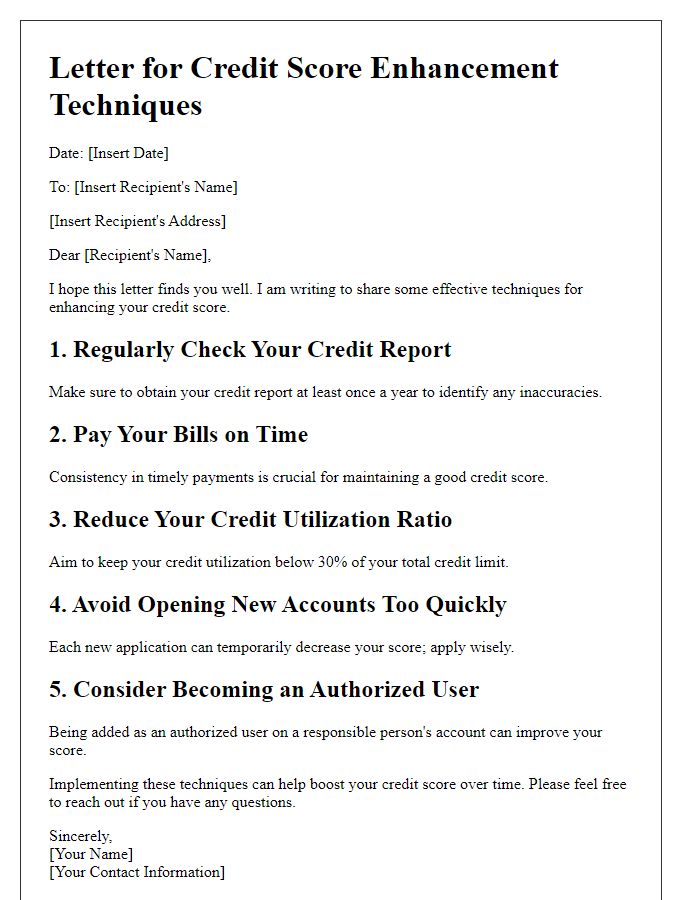

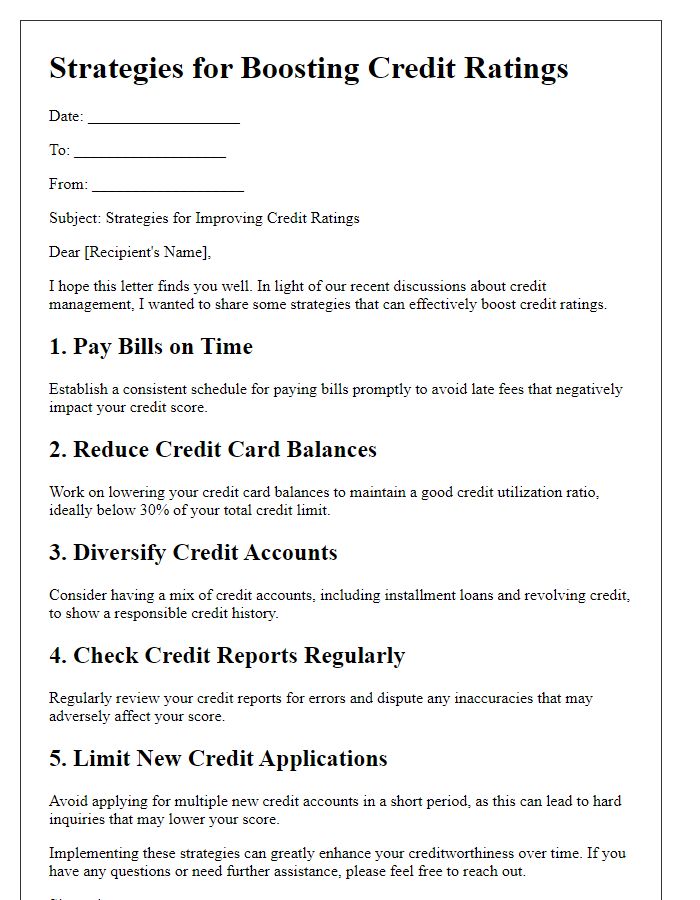

Understanding personal financial analysis is crucial for improving credit scores. Credit scores, often ranging from 300 to 850, represent an individual's creditworthiness, impacting loan approvals and interest rates. Key factors include payment history, which accounts for 35% of the score, significantly influenced by on-time payments for credit cards and loans. Credit utilization, the ratio of credit used to available credit, should ideally stay below 30%. A detailed cash flow review can identify spending habits, revealing areas to reduce debts. Regularly checking credit reports from agencies like Equifax, Experian, and TransUnion ensures there are no errors or fraudulent activities affecting scores. Establishing a mix of credit types, such as installment loans and revolving credit, can also enhance scores over time. Consistent monitoring of financial goals and adjustments based on market trends can further contribute to a healthier credit profile.

Payment History Review

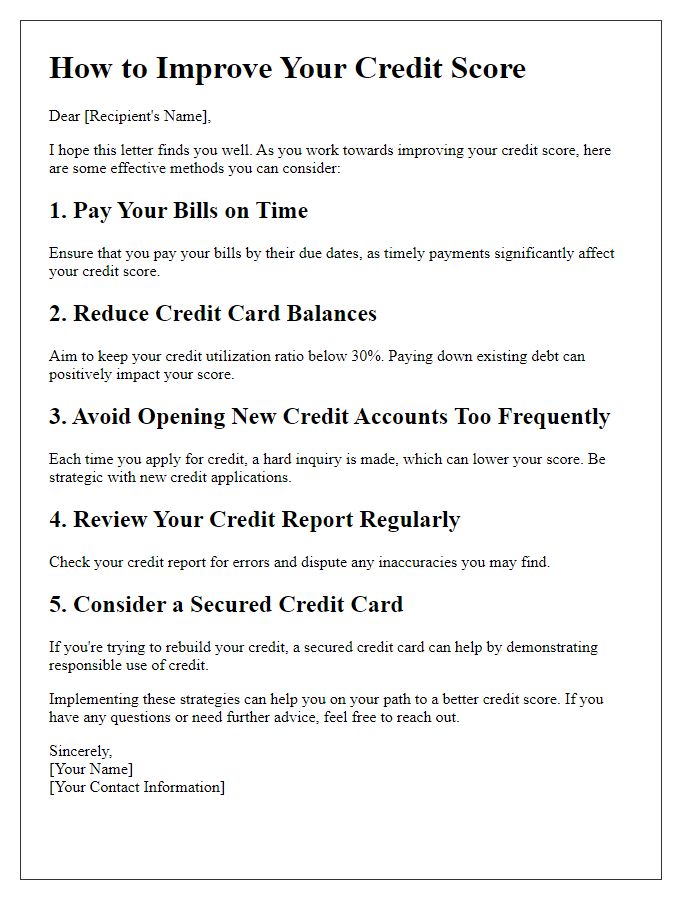

Examining payment history serves as a crucial strategy in enhancing credit scores, which are numerical representations of creditworthiness, typically ranging from 300 to 850. Each on-time payment contributes positively, underscoring responsible credit usage. Late payments, which can remain on credit reports for up to seven years, adversely impact scores significantly, often resulting in drops of 100 points or more. Reviewing credit reports from major bureaus like Experian, TransUnion, and Equifax can reveal discrepancies or outdated information, providing opportunities for dispute and correction. Consistent, timely payment habits foster better credit scores, providing individuals with access to lower interest rates and better loan terms.

Credit Utilization Management

Credit utilization management involves strategically maintaining credit card balances to improve overall credit scores. Ideally, experts recommend keeping utilization below 30% of the total available credit limit to positively impact credit history. High utilization rates can signal risk to lenders, potentially leading to declines in credit applications. Regularly monitoring accounts through reputable credit report services can help track usage patterns over time. Paying down outstanding balances, making multiple payments within a billing cycle, and opting for credit limit increases without increasing spending are effective strategies. These practices not only enhance credit health but also empower individuals to secure better interest rates for future loans or mortgages in financial marketplaces.

Dispute Inaccuracies Protocol

Inaccuracies in credit reports significantly impact credit scores, which are vital for obtaining loans and favorable interest rates. The Fair Credit Reporting Act (FCRA) mandates consumers to report discrepancies to credit reporting agencies such as Experian, Equifax, and TransUnion. A structured dispute protocol involves gathering evidence of inaccuracies, such as bank statements or payment receipts, and drafting a dispute letter that outlines errors clearly. Submission methods include certified mail, ensuring delivery confirmation, and allowing traceability. The credit bureau is required to investigate the claim, typically within 30 days, and the result must be communicated to the consumer. Successful disputes can enhance credit scores, leading to improved financial opportunities such as lower mortgage rates and better insurance premiums.

Future Credit Planning

Effective credit planning requires understanding core strategies to enhance credit scores. Monitoring credit reports regularly is essential; individuals should obtain reports from major credit bureaus like Experian, TransUnion, and Equifax. Payment history, constituting 35% of the credit score, plays a crucial role, hence timely payments on credit cards and loans is vital. Reducing credit utilization, ideally below 30%, can significantly boost scores; this involves managing credit card balances effectively. Maintaining a mix of credit, including installment loans and revolving credit, can demonstrate responsible borrowing behavior. Engaging in responsible credit inquiry practices, limiting hard inquiries, ensures that the credit profile remains attractive to lenders. Additionally, seeking professional guidance from credit counselors can provide personalized strategies for long-term credit health.

Read Also: Our Financial consultancy's Blogs

Comments