Are you considering retirement and feeling overwhelmed by the choices available for your financial future? Planning for retirement is more than just saving money; it involves strategic decisions that can significantly impact your lifestyle in your golden years. Advanced retirement strategies can help you navigate complex tax implications, diversify your investments, and optimize your income streams. If you're curious to learn more about these transformative approaches, keep reading to discover how to secure the retirement you've always dreamed of!

Image cover: Letter Template For Advanced Retirement Strategies

Letter Template For Advanced Retirement Strategies Samples

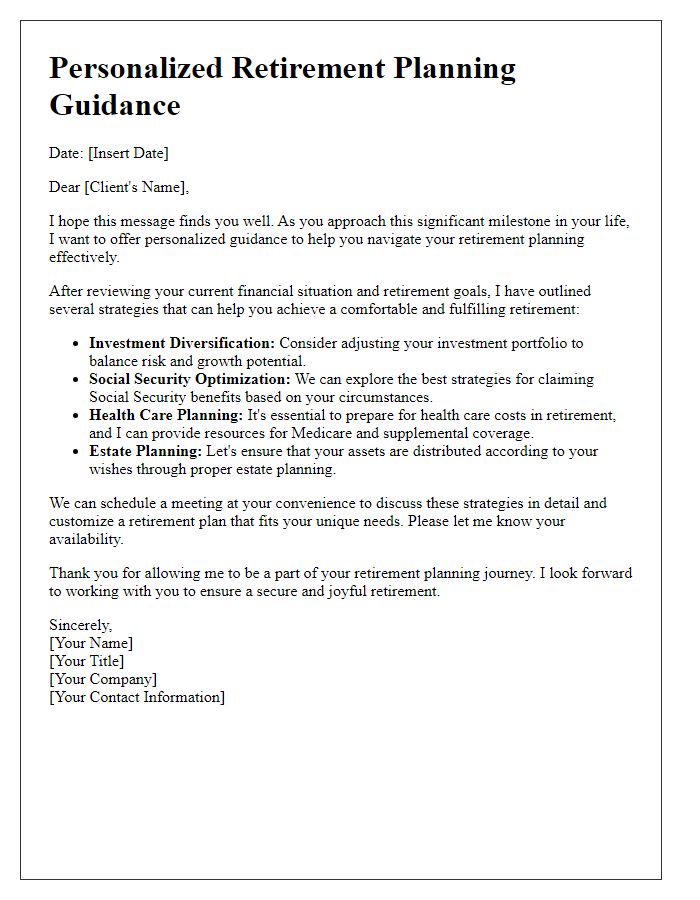

Personalized Retirement Goals

Personalized retirement goals involve assessing various factors such as lifestyle preferences, financial needs, and life expectancy to develop a tailored plan. Individuals often consider their desired retirement age, health care costs, and travel plans when mapping out their ideal future. For instance, a retiree aiming for a lifestyle resembling their current income of $75,000 per year must strategize to accumulate adequate savings through investments and pensions. Areas like investment portfolios, tax-efficient withdrawal strategies, and estate planning play critical roles in ensuring financial security. Additionally, utilizing tools such as 401(k) plans and IRAs can maximize saving potential and reduce tax burdens. Evaluating these elements continuously, especially with changing economic landscapes, is essential for a successful and fulfilling retirement.

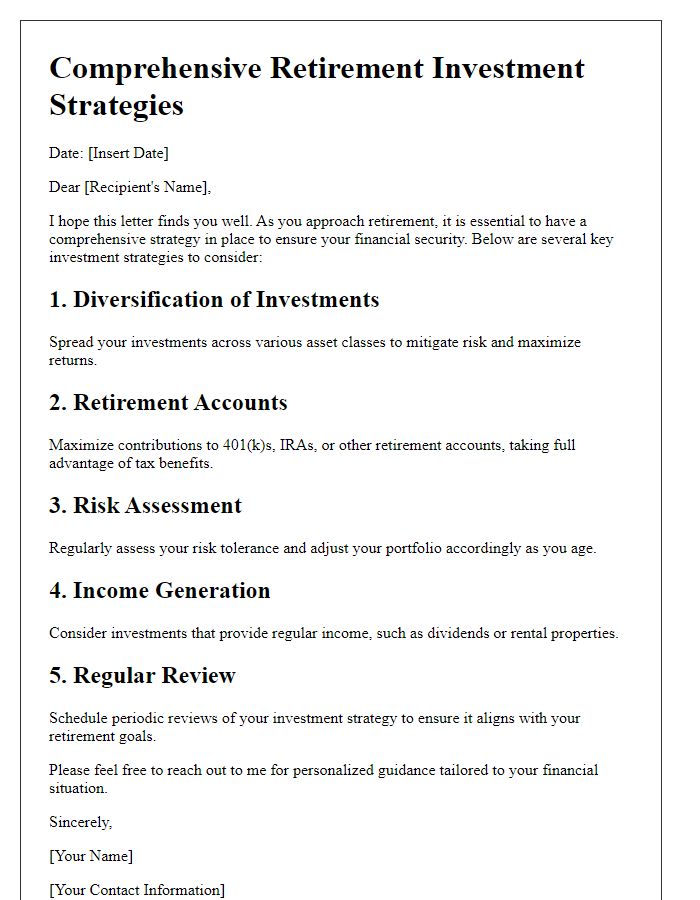

Diversified Investment Portfolio

Creating a diversified investment portfolio is essential for advanced retirement strategies. A diversified investment portfolio, comprising various asset classes such as stocks, bonds, and real estate, minimizes risk while maximizing potential returns. Historical data indicates that a balanced allocation can yield returns averaging around 7% annually, crucial for ensuring long-term financial stability in retirement. For example, investing in low-cost index funds within a 401(k) plan can provide broad market exposure while benefiting from tax advantages. Incorporating international investments also diversifies geographic risk, with emerging markets like India and Brazil showing significant growth potential. Regular rebalancing ensures alignment with changing market conditions, maintaining optimal risk levels. Additionally, exploring alternative investments, such as commodities or private equity, can enhance portfolio resilience against market volatility.

Tax-Efficient Withdrawal Plans

Tax-efficient withdrawal plans are essential for retirees looking to maximize their income while minimizing tax liabilities. Various strategies exist, such as the "bucket strategy," which involves categorizing assets into short-term, medium-term, and long-term buckets for different time horizons. Retirees aged 59 1/2 can utilize tax-advantaged accounts like Traditional IRAs or Roth IRAs, which offer unique tax benefits. The option to withdraw from taxable accounts first can help mitigate tax impacts, especially for those in higher income brackets during the early retirement years. A comprehensive withdrawal strategy should consider required minimum distributions (RMDs) starting at age 72, which can significantly impact tax situations. Additionally, understanding how different income sources--like Social Security and pensions--interact with tax brackets is crucial for effective planning. Regular reviews and adjustments to the withdrawal strategy can help adapt to changes in tax laws and personal financial situations, ensuring sustainable income throughout retirement.

Risk Management and Insurance

Advanced retirement strategies often encompass risk management and insurance to safeguard financial well-being in later years. One key element is long-term care insurance, which can cover significant healthcare costs starting around $50,000 annually for nursing home care, ensuring retirement savings remain intact. Another vital component is life insurance, providing financial support for dependents and covering outstanding debts; policies may range from $200,000 to millions based on individual needs. Annuities also play a crucial role in risk management, offering guaranteed income streams from $500 to several thousand monthly, depending on investment size and contract type. Portfolio diversification reduces risks associated with market volatility, with reallocations towards bonds, equities, and alternative investments tailored to personal retirement timelines, typically aimed for age 65 or beyond. These strategies form a comprehensive approach to maximizing retirement security and mitigating unforeseen challenges.

Estate Planning Considerations

Advanced retirement strategies encompass various estate planning considerations that significantly impact wealth management and asset distribution. Significant factors include the establishment of trusts, such as revocable living trusts, which provide seamless probate avoidance and efficient management of assets in states like California or New York, where probate processes can take months. Additionally, tax implications such as estate taxes must be meticulously analyzed; for instance, the federal estate tax exemption stands at $12.92 million as of 2023, necessitating proactive strategies for high-net-worth individuals. Incorporating advanced gifting strategies enables individuals to transfer wealth to beneficiaries, minimizing tax burdens. Considering charitable donations, such as through donor-advised funds, can provide tax deductions while supporting philanthropic goals. Properly addressing health care directives and power of attorney documents ensures that personal and financial decisions align with one's wishes during incapacity, further safeguarding family welfare. Comprehensive estate planning involves regular reviews and updates to reflect changes in personal circumstances, tax laws, or family dynamics, ensuring that the retirement strategy remains robust and effective over time.

Read Also: Our Financial consultancy's Blogs

Comments