Are you considering securing your child's future with an educational savings plan? With rising tuition costs and the importance of investing in your child's education, choosing the right savings strategy is more crucial than ever. Educational savings plans can offer you the peace of mind that comes from knowing you're preparing for their academic future. Let's dive in and explore the various options available to help you make an informed decision!

Image cover: Letter Template For Educational Savings Plans

Letter Template For Educational Savings Plans Samples

Plan Overview and Benefits

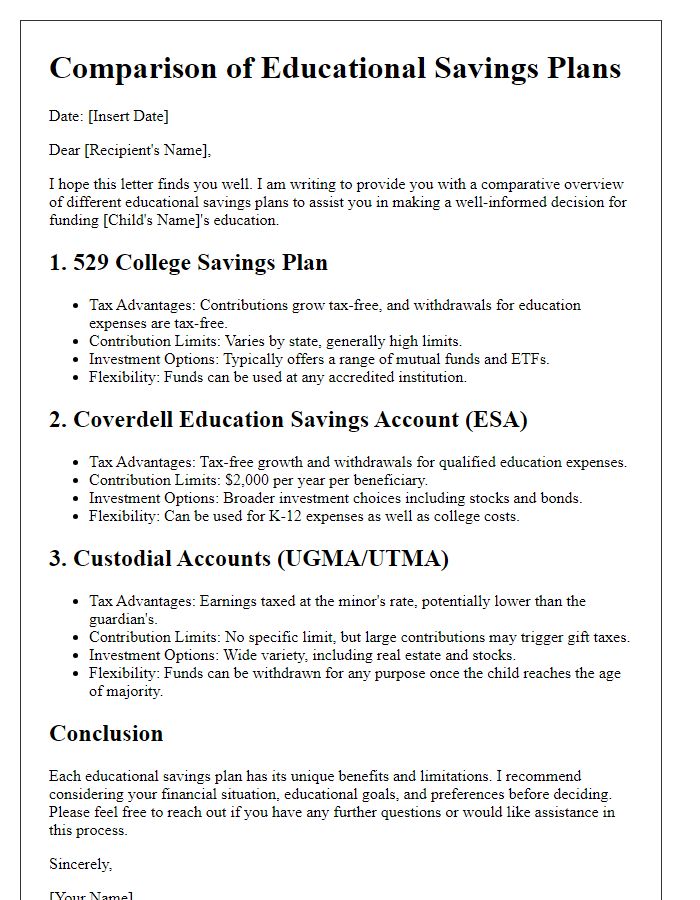

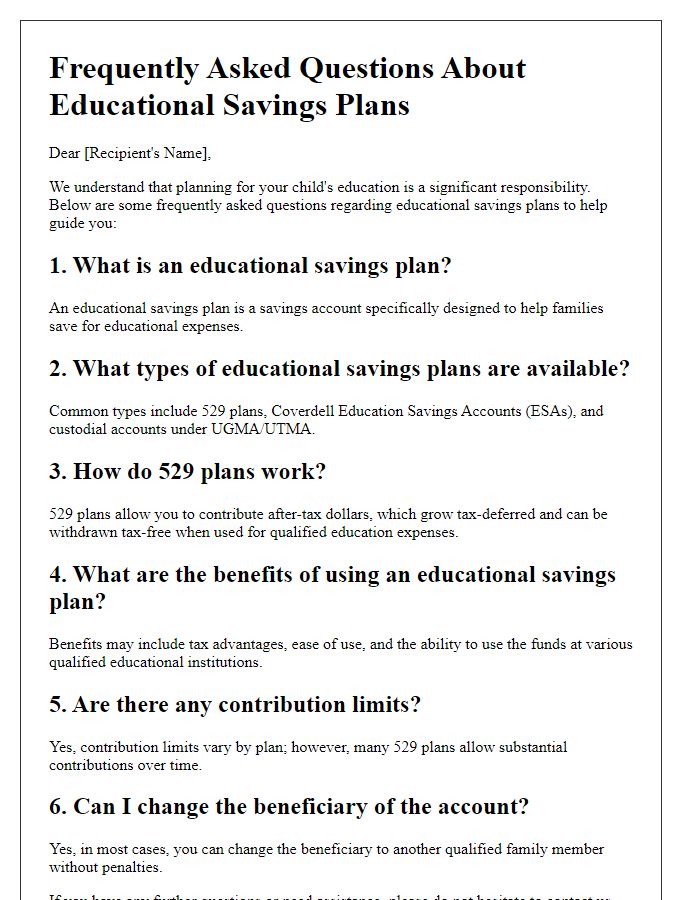

Educational savings plans provide a structured approach for financing future educational expenses, ensuring families can effectively save for college or other higher education costs. These plans, often referred to as 529 plans in the United States, offer tax advantages such as tax-free growth on investments and tax-exempt withdrawals for qualified educational expenses, including tuition, room, and board. With a variety of investment options, including age-based portfolios that become more conservative as the beneficiary approaches college age, families can customize their savings strategies. Many states also offer additional incentives, like matching contributions or state tax deductions, enhancing their appeal. By initiating an educational savings plan early, parents can maximize their savings potential, benefiting from compound interest over time, and ultimately reducing the financial burden associated with higher education.

Contribution Options and Limits

Educational savings plans, specifically 529 plans, offer flexible contribution options and limits that enable families to save for future educational expenses. Individuals can contribute up to $15,000 per year per beneficiary without incurring federal gift tax, allowing for significant long-term investment growth. Some states, such as New York, provide additional state tax deductions, further incentivizing contributions. Additionally, many plans allow for one-time lump-sum contributions or recurring monthly deposits, accommodating a variety of financial strategies. Some plans also permit the transfer of assets between accounts, providing flexibility as children grow and their educational needs evolve. Overall, strategic contributions to these plans can maximize educational funding for higher education institutions, such as universities and community colleges, providing essential financial support for students pursuing degrees.

Investment Strategies and Portfolio Choices

Educational savings plans, such as 529 plans (tax-advantaged savings accounts for education expenses), require careful consideration of investment strategies to maximize future returns. Asset allocation decisions typically involve diversifying between stocks, bonds, and money market funds, which can lead to varying levels of risk and potential growth. For instance, younger investors may opt for aggressive portfolios heavily weighted towards equities, acknowledging that a long investment horizon allows time to recover from market fluctuations. Older beneficiaries may prefer conservative allocations with a higher percentage of fixed-income securities to preserve capital as they approach college age, usually around 18 years old. Regularly reviewing and adjusting the portfolio according to changing market conditions and educational costs, which have risen over 25% over the past decade, ensures that families remain on track to meet financial goals.

Withdrawal Rules and Tax Implications

Educational savings plans, such as 529 plans, have specific withdrawal rules that are crucial to understand for optimal financial planning. Qualified withdrawals, used for expenses like tuition, books, and fees, can be made tax-free; however, expenses must align with IRS guidelines. Non-qualified withdrawals may incur income tax on earnings and an additional 10% penalty, impacting overall savings. Each state may impose differing regulations and tax incentives, creating variability in benefits. For example, in California, contributions to a 529 plan may reduce state taxable income, while New York offers a state tax deduction for contributions up to $5,000 for individuals. Furthermore, understanding the impact on financial aid eligibility is essential, as assets within a 529 plan generally count less against aid calculations than other savings. Families intending to utilize these plans efficiently should stay informed on changing regulations to maximize the financial advantages for higher education expenses.

Beneficiary Designation and Management

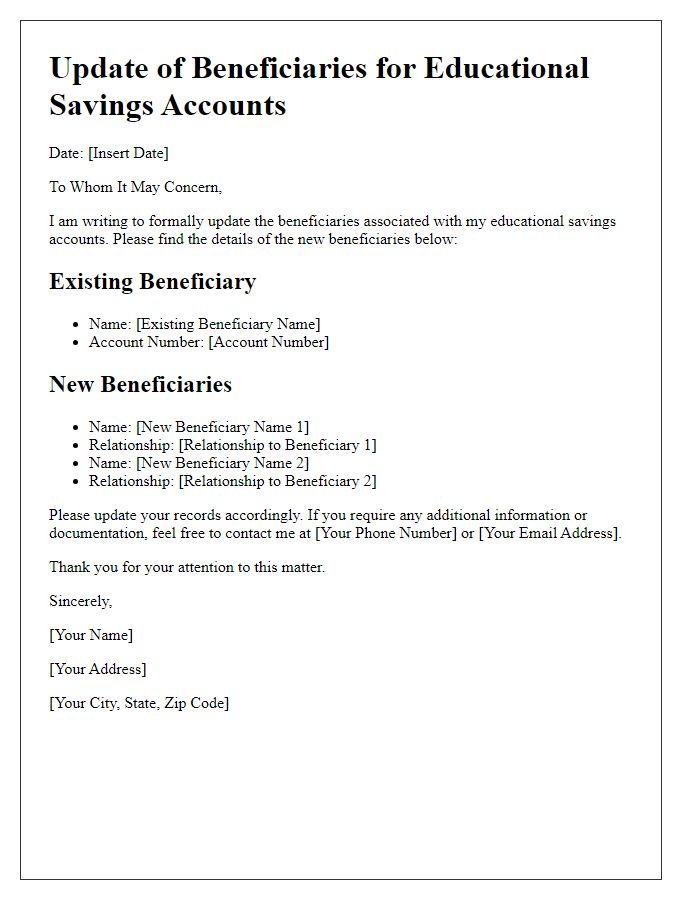

Educational savings plans, such as 529 plans or Coverdell Education Savings Accounts (ESAs), focus on funding higher education for beneficiaries like children or grandchildren. Beneficiary designation allows account owners to specify individuals authorized to receive funds for qualified educational expenses, including tuition, fees, and room and board. Managing these plans involves regular contributions, which can be adjusted annually or when financial situations change, maximizing tax advantages like tax-free growth on earnings and potential state tax deductions. Additionally, transferring the beneficiary designation between family members can provide flexibility, adapting to various educational paths and needs. Compliance with IRS regulations and plan-specific rules ensures optimal use of these savings vehicles, fostering financial preparedness for college expenses.

Read Also: Our Financial consultancy's Blogs

Comments