Are you looking to navigate the complexities of estate taxes with ease? Understanding how to effectively manage your estate can save your heirs significant amounts and ensure that your hard-earned wealth is preserved for generations to come. By utilizing strategic planning techniques, you can enhance tax efficiency and mitigate potential liabilities. Dive in as we explore essential strategies that can help you maximize your estate's value and minimize tax burdensâread on to discover more!

Image cover: Letter Template For Estate Tax Efficiency

Letter Template For Estate Tax Efficiency Samples

Accurate asset valuation

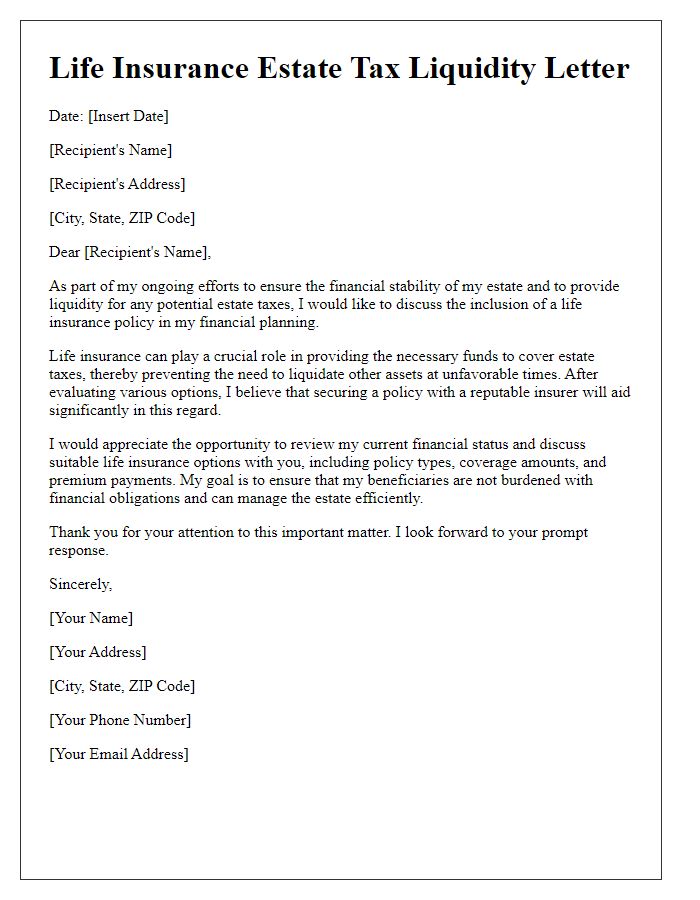

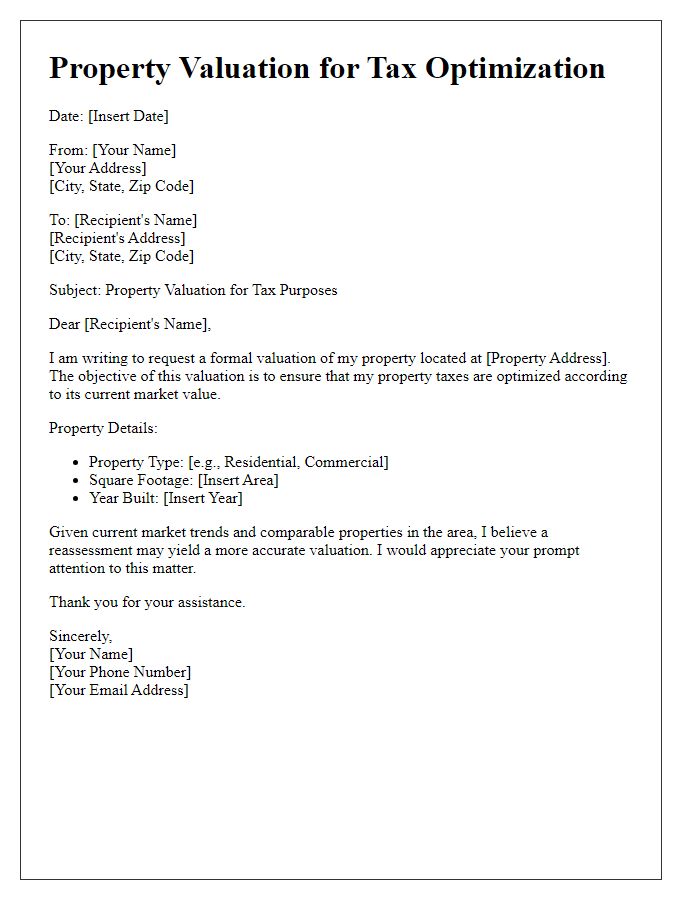

Accurate asset valuation plays a critical role in estate tax efficiency, impacting the estate planning process significantly. Real estate properties must be appraised at fair market value, with recent sales in the area serving as benchmarks, to ensure compliance with IRS regulations. Valuables, such as fine art and collectibles, require expertise from accredited appraisers, and the valuation must consider market trends from the last fiscal year. Financial instruments, including stocks and bonds, should reflect current trading prices to ascertain their worth precisely. Furthermore, businesses must undergo thorough valuation analyses that assess cash flow, market position, and asset-based values, accounting for intangible assets like goodwill. Engaging professionals in the field ensures that all assets are evaluated comprehensively, minimizing potential tax liabilities for beneficiaries and enhancing overall estate management.

Trust and will structuring

Creating an estate plan that maximizes tax efficiency often involves a strategic approach to trust and will structuring. Establishing a revocable living trust allows assets, including real estate and investments, to bypass probate--the legal process for distributing an estate--thus saving on potential delays and costs. Utilizing irrevocable trusts can provide significant estate tax benefits, removing certain assets from the taxable estate while still allowing for income generation. Certain exemptions, such as the federal lifetime estate and gift tax exclusion, which stood at $11.58 million for individuals in 2020, can also be leveraged to minimize taxes owed upon death. Incorporating straightforward wills ensures clarity in asset distribution, while also designating guardians for minor children. Moreover, taking advantage of gifting strategies can further reduce the taxable estate, allowing for annual tax-free gifts under the IRS annual exclusion, which was $15,000 per recipient in 2020. These meticulously structured documents create a comprehensive and tax-efficient estate plan that aligns with the individual's financial goals and family needs.

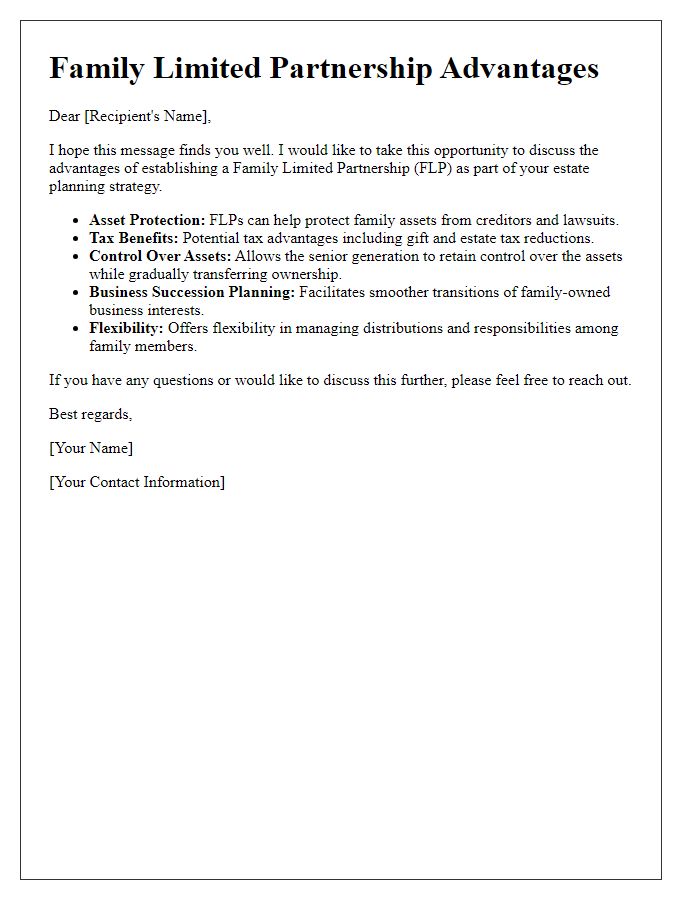

Gifting strategies

Effective gifting strategies can significantly enhance estate tax efficiency for individuals looking to transfer wealth while minimizing tax implications. Annual exclusion gifts allow individuals to give up to $17,000 (as of 2023) per recipient without incurring gift tax, thus reducing the taxable estate. Utilizing the lifetime gift tax exemption, which is approximately $12.92 million for individuals (2023), enables substantial transfers without immediate tax consequences. In addition, gifts made directly to educational institutions or medical providers on behalf of another person are exempt from the gift tax, further facilitating wealth transfer. Establishing a charitable remainder trust (CRT) can provide income during the donor's lifetime while reducing estate taxes through charitable deductions. Furthermore, implementing strategies like family limited partnerships (FLPs) allows for valuation discounts, effectively decreasing the overall estate's value for tax purposes. Each of these strategies showcases sophisticated approaches to estate planning, aiding in tax efficiency and maximizing asset distribution to heirs.

Exemption maximization

Maximizing exemptions can significantly enhance estate tax efficiency for individuals and families in the United States. The federal estate tax exemption, set at $12.92 million per individual for the year 2023, allows wealthy individuals to transfer a substantial amount of wealth without incurring federal estate taxes. Strategically utilizing gifting strategies, individuals can transfer assets during their lifetime, taking advantage of the annual exclusion gift amount of $17,000 per recipient, which further reduces the taxable estate. Additionally, leveraging the marital deduction enables spouses to transfer an unlimited amount of assets to each other without triggering estate taxes, ensuring that estate plans align with the latest estate tax laws. Utilizing tools like revocable living trusts and charitable remainder trusts can also provide further tax benefits while preserving family wealth across generations. Proper planning and consultation with estate planning professionals can ensure that families navigate complex tax implications and maximize their exemptions effectively.

Collaboration with tax professionals

Effective estate tax efficiency often requires collaboration with seasoned tax professionals, notably Certified Public Accountants (CPAs) and estate planning attorneys. These specialists possess in-depth knowledge of the Internal Revenue Code, specifically IRS regulations regarding exemptions, deductions, and alternative valuation dates. Engaging with these experts can uncover strategies to minimize estate taxes, such as utilizing the annual gift tax exclusion of $17,000 per recipient (as of 2023), or establishing irrevocable trusts that can provide significant tax benefits. Additionally, incorporating charitable donations into estate plans can further reduce taxable estate values. By coordinating their expertise, individuals can effectively streamline the estate planning process and optimize their legacy for future generations.

Read Also: Our Financial advisor's Blogs

Comments