Are you curious about how credit cards can influence your credit score? It's a topic that often raises more questions than answers, especially with so many myths floating around. Understanding the relationship between your credit card usage and your credit score can empower you to make smarter financial decisions. Dive into our guide to unravel the intricacies of credit and boost your financial literacy!

Image cover: Letter Template For Credit Card Credit Score Impact Guide

Letter Template For Credit Card Credit Score Impact Guide Samples

Purpose of the Guide

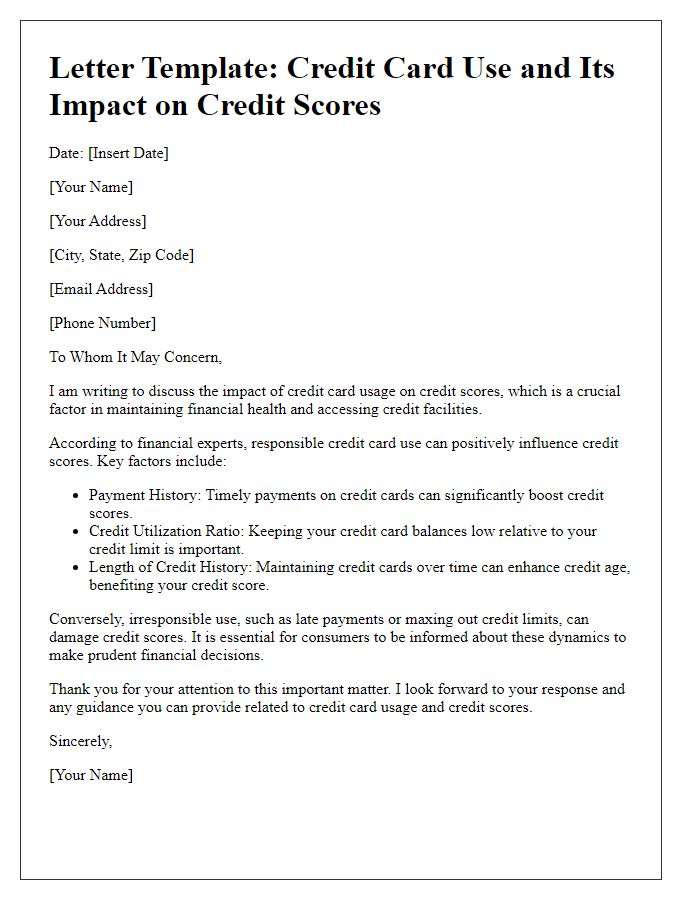

Understanding the purpose behind the guide on credit card credit score impact is essential for financial wellness. This guide aims to educate consumers about how credit card usage directly influences their credit scores, which typically range from 300 to 850. It highlights factors such as credit utilization ratio (ideally below 30%), payment history (one of the most significant factors), and the length of credit history. By examining specific scenarios, such as late payments, applying for multiple cards in a short time frame, and maintaining low balances, readers can gain insights into how these behaviors affect their overall creditworthiness. This knowledge empowers individuals to make informed decisions, potentially leading to better interest rates and improved financial opportunities.

Understanding Credit Scores

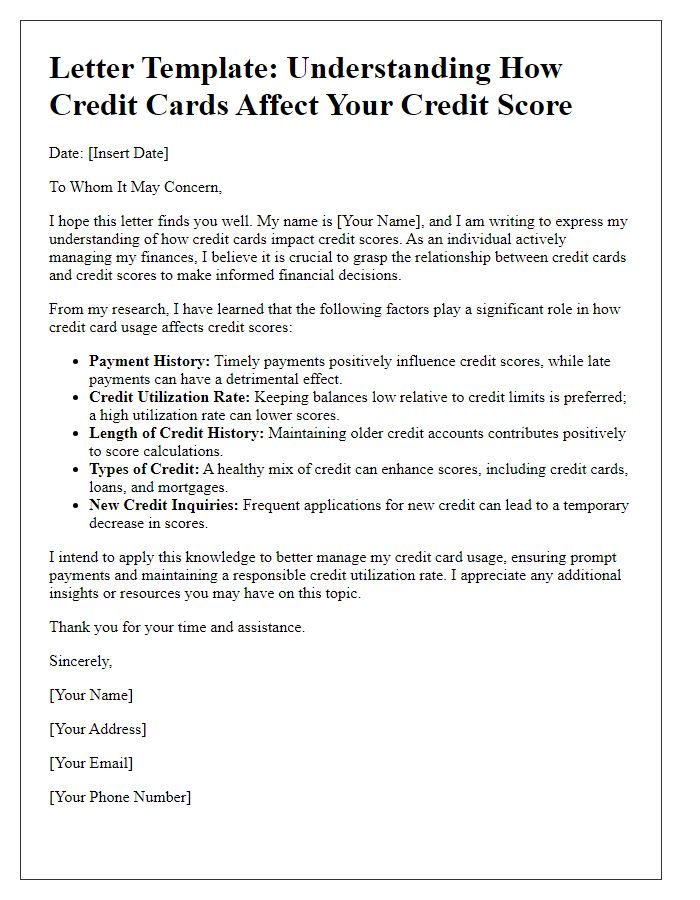

Credit scores play a crucial role in financial health, influencing loan eligibility, interest rates, and even employment opportunities. The scoring system, primarily represented by three major credit bureaus--Equifax, Experian, and TransUnion--ranges from 300 to 850. Factors such as payment history (35% of the score), credit utilization ratio (30%), length of credit history (15%), types of credit in use (10%), and recent credit inquiries (10%) shape this number. For example, maintaining a credit utilization ratio below 30% can significantly boost a score, while late payments can drop a score by over 100 points, adversely affecting purchases like homes or vehicles in cities such as Los Angeles or New York. Understanding these components enables individuals to make informed financial decisions and improve overall creditworthiness.

Factors Affecting Credit Scores

Credit scores, numerical representations of creditworthiness, can significantly influence lending decisions. Key factors affecting these scores include payment history, which accounts for approximately 35% of the score, reflecting punctuality in repaying debts. Credit utilization ratio, the percentage of available credit currently being used, is another critical factor, typically recommended to remain below 30% to maintain a healthy score. Length of credit history plays a role as well, with longer credit accounts positively impacting scores, suggesting reliability. Additionally, types of credit--such as revolving accounts like credit cards and installment loans like mortgages--contribute to the diversity of the credit mix, beneficial for a robust score. Lastly, numerous recent credit inquiries may negatively affect scores, as they suggest increased credit risk to lenders.

Tips for Improvement

Credit card management plays a vital role in influencing an individual's credit score. Payment history constitutes 35% of the FICO score, highlighting the importance of timely payments. Credit utilization, the ratio of current credit card balances to credit limits, should ideally remain below 30% to prevent negative impacts. Regularly reviewing credit reports from agencies like Experian or TransUnion can uncover inaccuracies that may adversely affect the score; consumers are entitled to one free report annually per agency. Moreover, maintaining a mix of credit types--such as revolving credit and installment loans--can enhance the overall credit profile. Lastly, avoiding excessive new credit inquiries, which can lead to temporary score drops, is crucial for long-term credit health.

Contact Information for Support

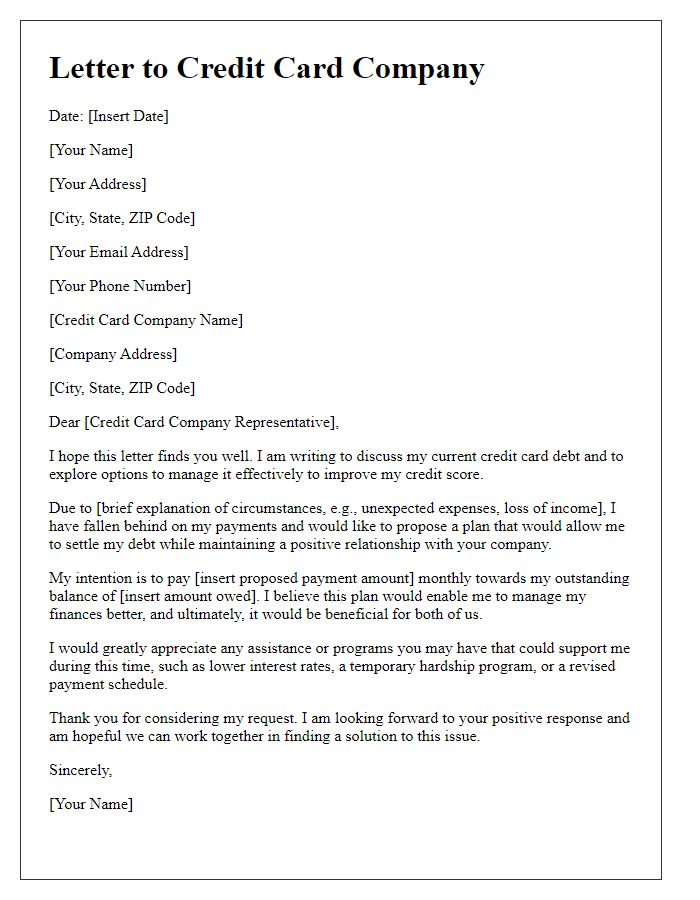

Credit card utilization significantly influences credit scores, impacting financial health and lending capability. High credit card balances (ideally under 30% utilization) negatively affect scores, causing potential denials for loans or mortgages (e.g., home loans averaging $250,000). Payment history, including late payments (over 30 days), also plays a crucial role, as even one late payment can lower scores by 100 points or more. Credit inquiries from applications can temporarily reduce scores, especially from hard inquiries (involving a full credit check), which can stay on reports for two years. Regular monitoring of credit reports from agencies like Experian, TransUnion, and Equifax is essential for maintaining a healthy credit score (generally ranging from 300 to 850).

Read Also: Our Credit card company's Blogs

Comments