Are you looking for a straightforward way to communicate essential information to your board through internal audits? Crafting an effective letter can streamline the process and ensure that everyone is on the same page. By setting out clear objectives and key findings, you can enhance transparency and foster trust within your organization. Join us as we explore the nuances of creating the perfect letter template for board internal audits and elevate your communication strategy!

Image cover: Letter Template For Board Internal Audit

Letter Template For Board Internal Audit Samples

Purpose and Objectives

An internal audit serves a critical function within an organization, ensuring adherence to regulations and operational efficiency. Key objectives include evaluating the effectiveness of governance processes, assessing risk management strategies, and verifying compliance with applicable laws and policies. The purpose encompasses providing an independent assessment of internal controls, identifying potential areas for improvement, and enhancing accountability across departments. An internal audit also aims to stimulate organizational learning, guiding management to make informed decisions that drive sustainable performance and operational excellence. Engaging stakeholders, including the audit committee, is vital for fostering transparency and trust throughout the audit process.

Scope and Responsibilities

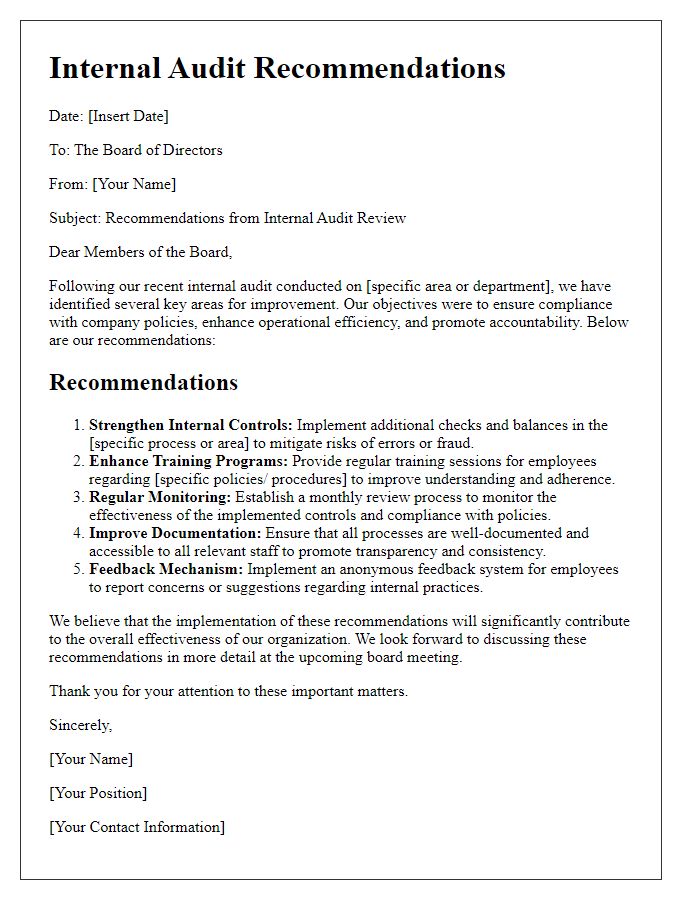

The internal audit scope encompasses various critical areas within the organization, focusing on assessing operational efficiency and compliance with established regulations. Key responsibilities include evaluating financial reporting processes, examining internal controls, and identifying potential risks (both operational and financial). The audit will also analyze adherence to policies, ensuring alignment with organizational objectives and industry standards. Additionally, the internal audit team will provide recommendations for improvement, facilitating enhanced governance and accountability across departments. This comprehensive approach aims to ensure that resources are utilized effectively and that the organization remains resilient against challenges, ultimately supporting long-term sustainability and success.

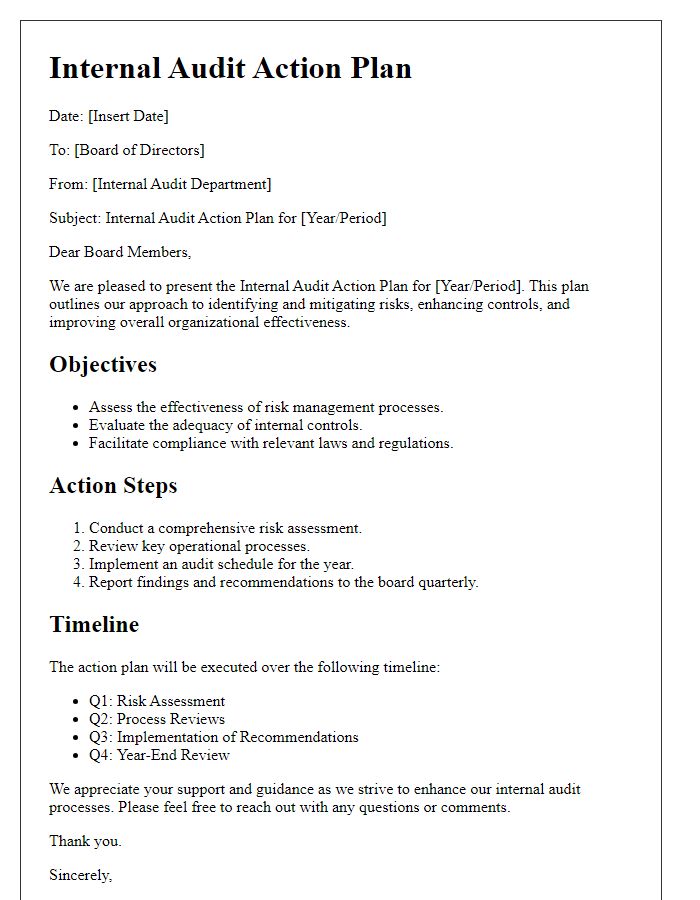

Audit Methodology

The audit methodology is a crucial framework guiding the internal audit process within organizations. This systematic approach consists of several key components, including risk assessment, planning, execution, and reporting. Risk assessment identifies potential areas of concern that may impact organizational integrity and compliance. The planning phase involves developing a detailed audit plan, determining the scope, objectives, and timeline, which may span several months. During the execution phase, auditors gather evidence through interviews, document reviews, and data analysis to assess compliance with policies and regulations, such as the Sarbanes-Oxley Act, which imposes strict auditing standards on publicly traded companies. Finally, the reporting stage presents findings and recommendations to the board, ensuring transparency and accountability in financial practices and governance. Overall, an effective audit methodology enhances organizational performance and promotes risk mitigation.

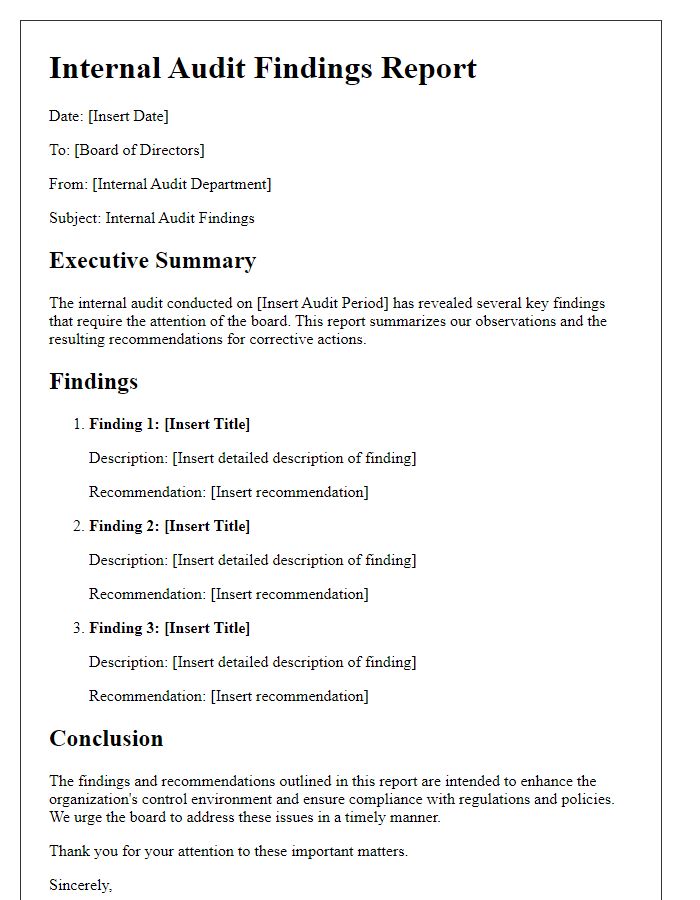

Reporting and Communication

Internal audits serve as essential tools for organizations to ensure compliance, efficiency, and transparency within operations. Effective reporting during an internal audit provides stakeholders, such as board members and executives, with clear insights into financial performance, risk management, and operational effectiveness. Documentation must encompass thorough evaluations of processes, highlighting key findings and areas for improvement. Furthermore, maintaining open lines of communication throughout the audit process fosters a culture of accountability and enhances cooperation among departments. Implementing a structured reporting framework, which includes timelines, review protocols, and action plans, is vital for addressing shortcomings discovered during the audit, ensuring prompt corrective measures. Regular updates and feedback sessions also facilitate stakeholder engagement, allowing the board to make informed decisions based on the audit's outcomes.

Follow-up and Resolution Procedures

The board's internal audit committee emphasizes the importance of following up on audit findings to ensure compliance and efficiency within the organization's operations. The established follow-up procedures include a timeline for addressing each audit recommendation, typically within 30 to 90 days, depending on the severity of the issue. The designated personnel responsible for implementation will document their actions and resolutions in a formal report. This report is then reviewed during quarterly board meetings, ensuring transparency and accountability. Additionally, a tracking system will monitor progress on each recommendation, with a designated auditor assigned to verify the effectiveness of implemented changes. Regular communication with department heads will facilitate ongoing improvement and adherence to best practices in organizational governance.

Read Also: Our Board member's Blogs

Comments