Are you navigating the complex world of deferred tax assets and their realization? Understanding how to accurately assess and communicate these financial nuances is crucial for effective tax strategy planning. In this article, we'll explore essential components of a letter template tailored for deferred tax asset realization, ensuring clarity and compliance in your communication. So, let's dive deeper into this vital topic together!

Image cover: Letter Template For Deferred Tax Asset Realization

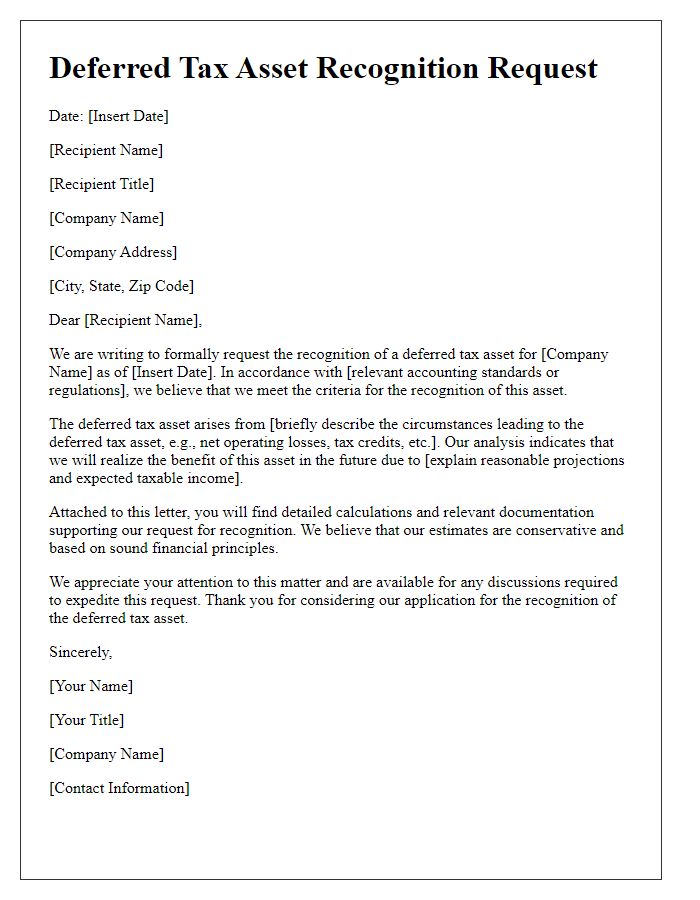

Letter Template For Deferred Tax Asset Realization Samples

Introduction and Purpose

Deferred tax assets serve as important financial tools for companies, representing potential tax savings anticipated from future taxable income. This document aims to clarify the rationale and intention behind the recognition of deferred tax assets on financial statements, particularly within the context of accounting standards such as IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles). These assets often arise from temporary differences, such as net operating losses (NOLs) or differences in depreciation methods, which can ultimately influence cash flow management and financial planning. Understanding their realization is crucial for stakeholders, allowing for an informed assessment of a company's future financial position and profitability potential. Proper assessment involves evaluating the likelihood of generating sufficient taxable income within the carryforward period, as this can lead to a more accurate representation of the company's financial health.

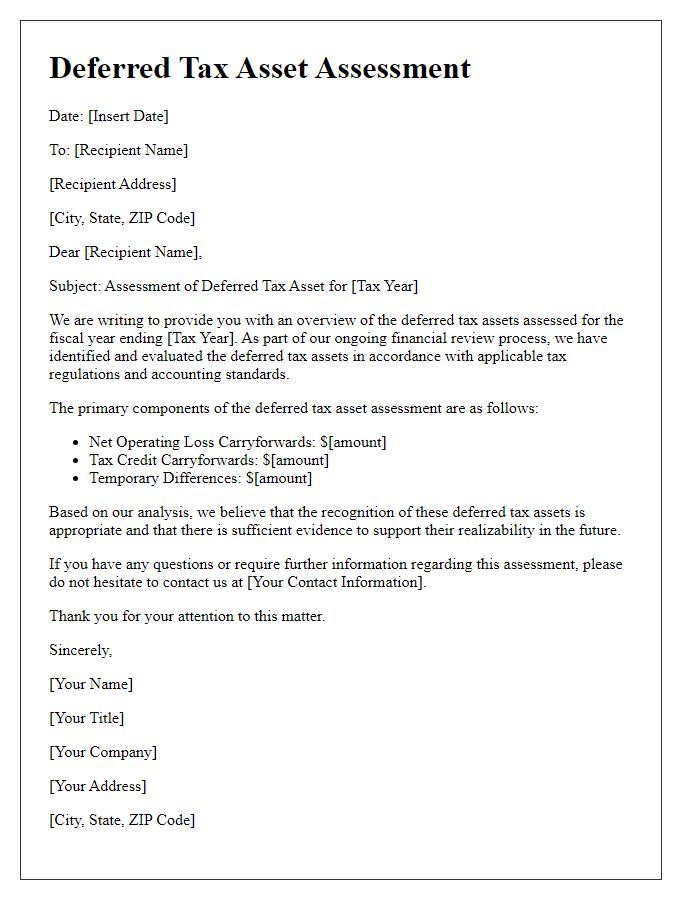

Explanation of Deferred Tax Asset

Deferred tax assets represent future tax benefits that arise when taxable income is greater than accounting income. Examples include losses carried forward that can reduce future tax liabilities. This situation might occur due to temporary differences in asset valuations or when expenses are recognized on financial statements before the tax return reflects them, like research and development expenditures. Deferred tax assets can significantly impact financial statements and cash flow, especially when companies expect to generate sufficient taxable income in the future to utilize these assets effectively. A thorough assessment of the realizability of deferred tax assets is essential, particularly considering the applicable jurisdiction's tax regulations, as outlined in relevant accounting standards like ASC 740 and IFRS 12.

Justification for Realization

A deferred tax asset (DTA) realization involves evaluating the likelihood of future taxable income to support the recognition of a DTA on the balance sheet. If a company, such as XYZ Corp, has incurred significant losses over prior years (e.g., $3 million loss in 2022), this loss can be carried forward to offset future taxable income. According to IRS regulations, XYZ Corp can utilize these net operating losses (NOLs) for future tax returns, thus impacting the company's effective tax rate. Additionally, projections for 2024 indicate a rebound in revenue with anticipated income of $5 million, greatly increasing the probability of realizing the DTA. On a balance sheet, a DTA of approximately $1.2 million can be justified given the expected future profits and the continuity of business operations in key markets such as technology and retail. Regular assessments of tax positions and ongoing financial forecasts are crucial for ensuring that the DTA reflects realistic expectations of income generation and a positive tax environment.

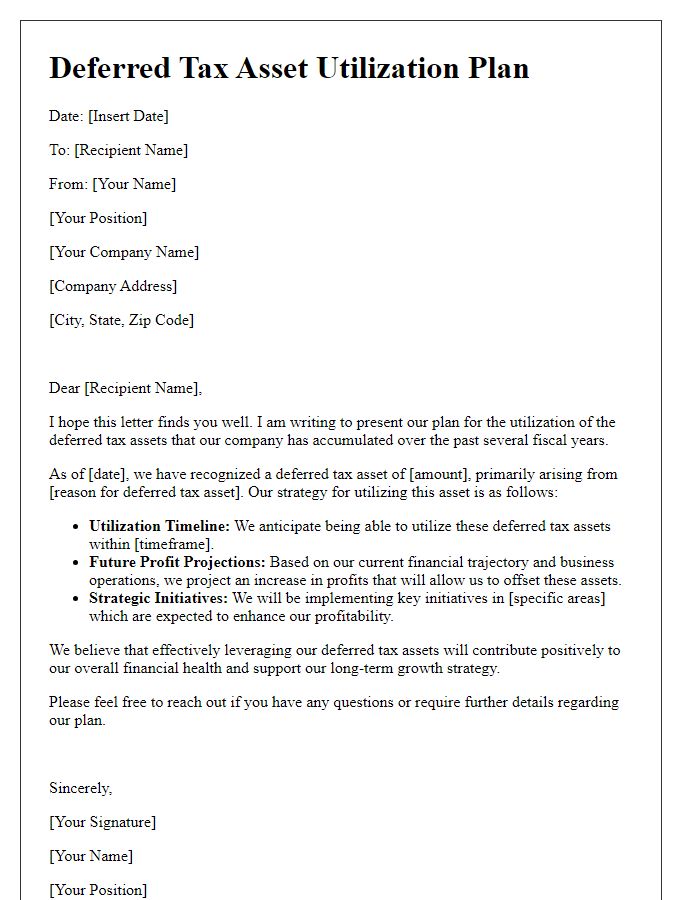

Future Profit Projections

Deferred tax assets (DTAs) represent future tax benefits arising from temporary differences between the book value and tax value of assets and liabilities. Proper realization of DTAs relies heavily on accurate future profit projections, which necessitate a meticulous analysis of potential revenue streams and market conditions. Companies must consider their historical financial performance, industry trends, economic indicators, and competitive landscape while forecasting profitability. For instance, a technology firm projecting growth in annual revenue by 20% over the next five years should evaluate factors such as product innovation cycles and consumer demand. Achieving profitability within the projected period is critical for realizing DTAs, which can subsequently influence tax savings and cash flow.

Risk Management and Contingencies

Deferred tax assets can significantly impact financial statements of corporations, particularly in sectors subject to fluctuating earnings, such as technology or finance. Realization of these assets depends on future taxable income projections, which must consider regulations set by the Internal Revenue Service (IRS) as well as state-specific tax codes. Effective risk management strategies must be implemented to assess the likelihood of realizing deferred tax assets, taking into account various contingencies, such as market downturns or changes in tax laws. Additionally, potential reversal of these assets could occur if the company does not meet the necessary income thresholds in subsequent fiscal periods. Regular evaluations and adjustments to this asset's valuation allowance are crucial to ensure compliance with accounting standards, such as Generally Accepted Accounting Principles (GAAP), thereby minimizing financial risks associated with uncertain future profitability.

Read Also: Our Accounting department's Blogs

Comments