As you approach this exciting chapter of your life, crafting a solid retirement plan can feel overwhelming, but it doesn't have to be. With the right guidance and resources, you can set yourself up for a secure and fulfilling future. In this article, we'll explore tailored retirement plan recommendations that cater to your unique needs and aspirations. So, grab a cup of coffee and let's dive into strategies that can help you enjoy the retirement you've always dreamed of!

Image cover: Letter Template For Retirement Plan Recommendations

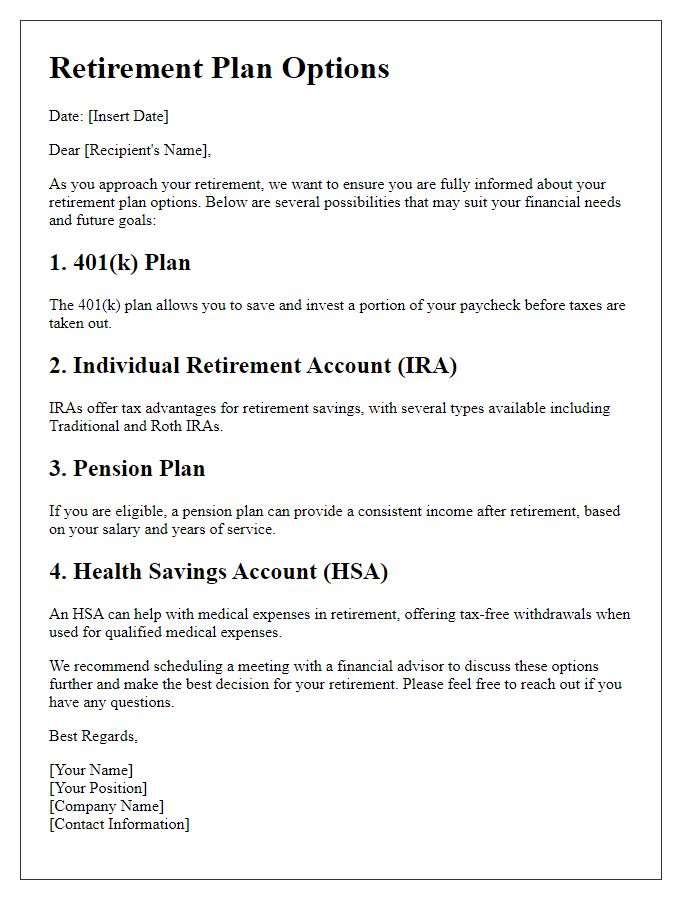

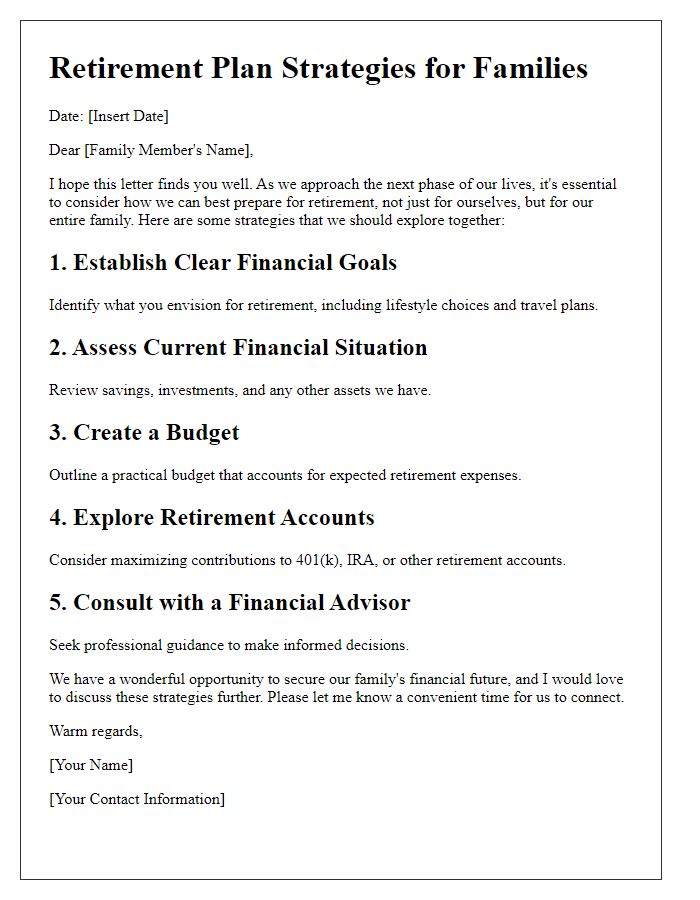

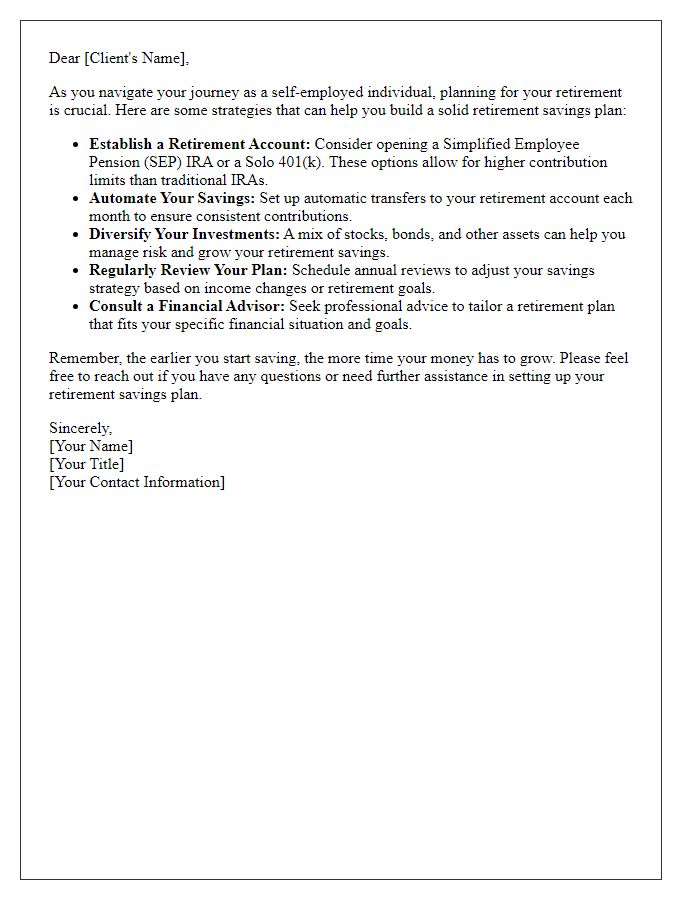

Letter Template For Retirement Plan Recommendations Samples

Client's Financial Goals

A comprehensive retirement plan should align with the client's financial goals, such as maintaining lifestyle choices, achieving stable income, and preparing for healthcare costs. Clients often aim for a retirement income approximately 70-80% of their pre-retirement earnings to sustain their preferred lifestyle. Calculating desired retirement age, usually between 62-67 years, and expected lifespan, up to 90 or beyond, is crucial in determining the savings needed. Utilizing investment vehicles like 401(k) accounts, IRAs, and annuities should factor into the strategy to maximize tax benefits and compound growth. Regular assessments of market performance, inflation rates (averaging around 2% annually), and Social Security benefits (providing an average of $1,500 per month) are essential to adapt the plan as needed. Understanding these dynamics empowers clients to make informed decisions while preserving their financial security during retirement years.

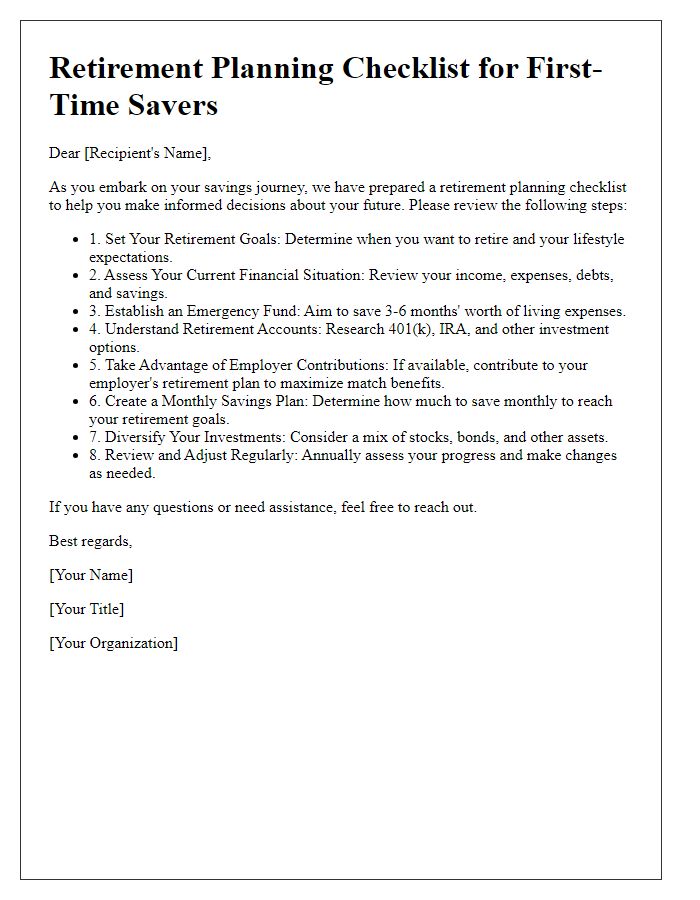

Retirement Timeline

Creating an effective retirement plan requires a clear timeline that outlines key milestones. Start by identifying retirement age, commonly between 65-70 years, as a target. Calculate the total savings needed to maintain desired lifestyle, considering average annual expenses of $60,000 in the U.S. Factor in Social Security benefits, typically beginning at age 62, with the average monthly benefit around $1,300. Establish milestones for saving contributions, suggesting a 15% savings rate from income, including employer match, starting as early as age 25 for maximum impact. Include checkpoints at age 30, 40, 50, and 60 to assess progress and adjust investments based on shifting market conditions. Emphasize the importance of healthcare costs, estimated to reach $200,000 for a couple during retirement, and the necessity of long-term care insurance, often sought around age 55. Encourage regular consultations with financial advisors to refine investment strategies and ensure alignment with evolving goals.

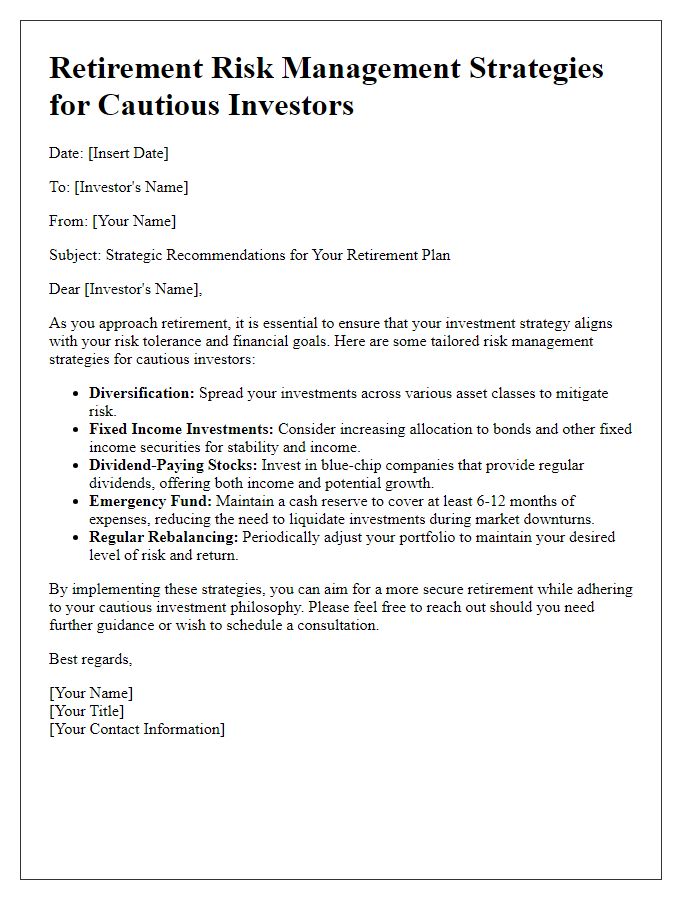

Risk Tolerance

Effective retirement planning necessitates a deep understanding of individual risk tolerance, which influences investment choices and asset allocation. Risk tolerance, defined by an investor's comfort level with market volatility and potential financial loss, varies significantly among individuals. Age, financial goals, and personal circumstances, such as dependent children or healthcare needs, play crucial roles in determining this tolerance. For example, younger investors in their 30s may afford to take greater risks as they have time to recover from market downturns, while individuals nearing retirement should prioritize capital preservation. Insightful evaluations of historical market performance, such as the S&P 500, can further aid in making informed decisions. Balancing equities, bonds, and alternative investments can create a diversified portfolio tailored to meet specific risk tolerance levels and ultimately lead to achieving financial security during retirement years.

Investment Options

Diversifying investment portfolios is essential for effective retirement planning. Target-date funds, which automatically adjust asset allocation based on retirement date, offer a hands-off approach for investors. Municipal bonds, known for their tax-exempt status, provide stable income streams for retirees. Stock index funds, tracking market indices such as the S&P 500, present long-term growth potential; over the last decade, the average annual return has been approximately 14%. Real estate investment trusts (REITs) typically yield higher dividends than traditional stocks, making them appealing for income-oriented portfolios. Furthermore, annuities, particularly fixed indexed annuities, can guarantee regular income in retirement, mitigating longevity risk. Balancing these options according to risk tolerance and investment horizon is crucial for maximizing retirement savings.

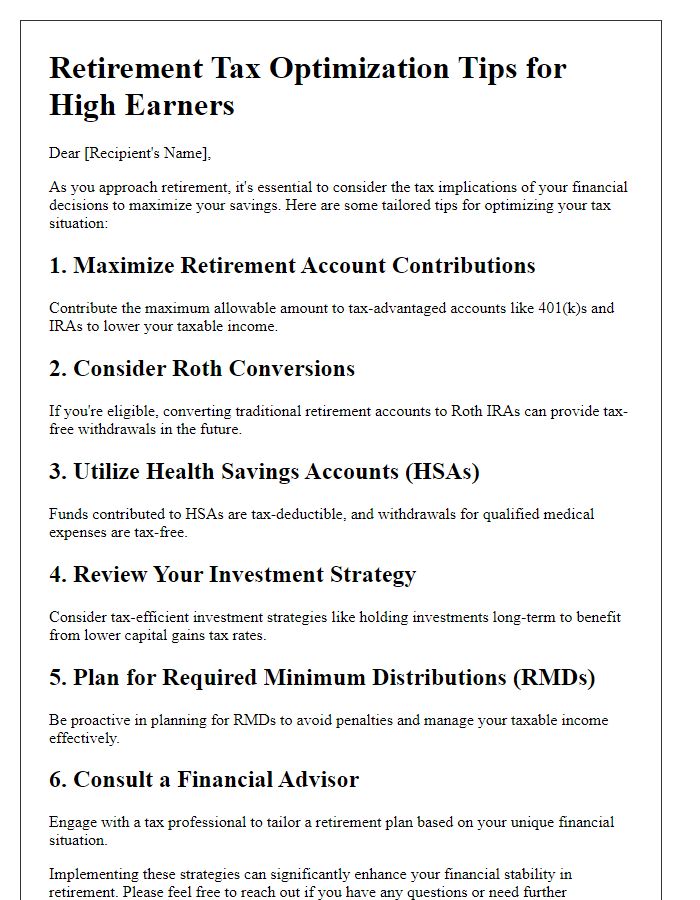

Tax Implications

Creating a comprehensive retirement plan requires an understanding of tax implications, which can significantly impact an individual's retirement savings. The most common retirement accounts include 401(k) plans and Individual Retirement Accounts (IRAs), each with distinct tax treatments. Contributions to a traditional 401(k) are tax-deferred, meaning individuals do not pay taxes on contributions until withdrawal. This could result in significant tax savings during high-income years. Roth IRAs, however, require contributions to be made post-tax, allowing for tax-free withdrawals in retirement, provided certain conditions are met. Understanding federal tax brackets and potential state taxes is crucial, as these will influence how much tax individuals might owe upon retirement income distribution. Strategies like tax-loss harvesting from taxable accounts may also be beneficial, as well as considering the timing of withdrawals to minimize tax burdens. Estate taxes can further complicate retirement planning, especially for high-net-worth individuals, making professional guidance essential for optimizing tax efficiency throughout retirement.

Read Also: Our Accountant's Blogs

Comments