In today's fast-paced world, understanding the economic impact of our decisions is more crucial than ever for stakeholders. Whether you're a business leader, community organizer, or policy maker, grasping the nuances of economic assessments can significantly influence your strategies and outcomes. This article will dive into the essential elements of conducting a thorough economic impact assessment and how it can benefit you and your stakeholders. Join us as we explore the fundamental concepts that can help you make informed decisionsâlet's get started!

Image cover: Letter Template For Stakeholder Economic Impact Assessment

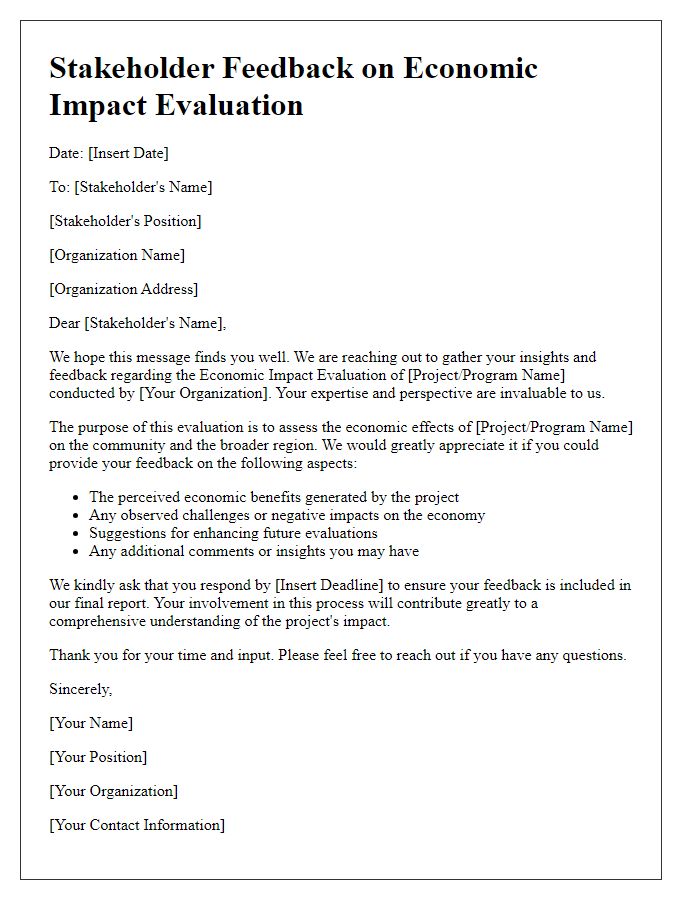

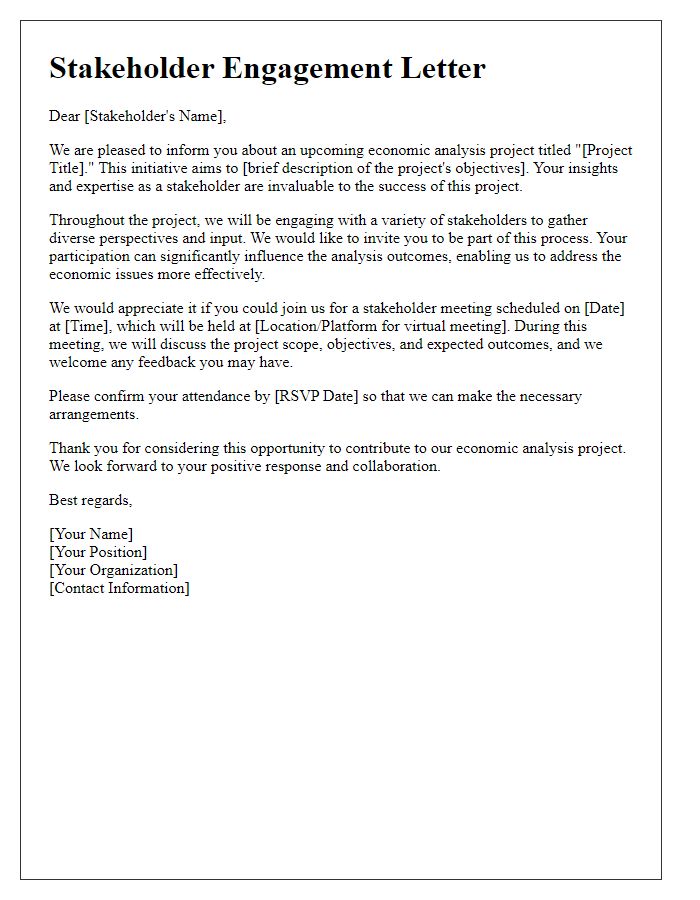

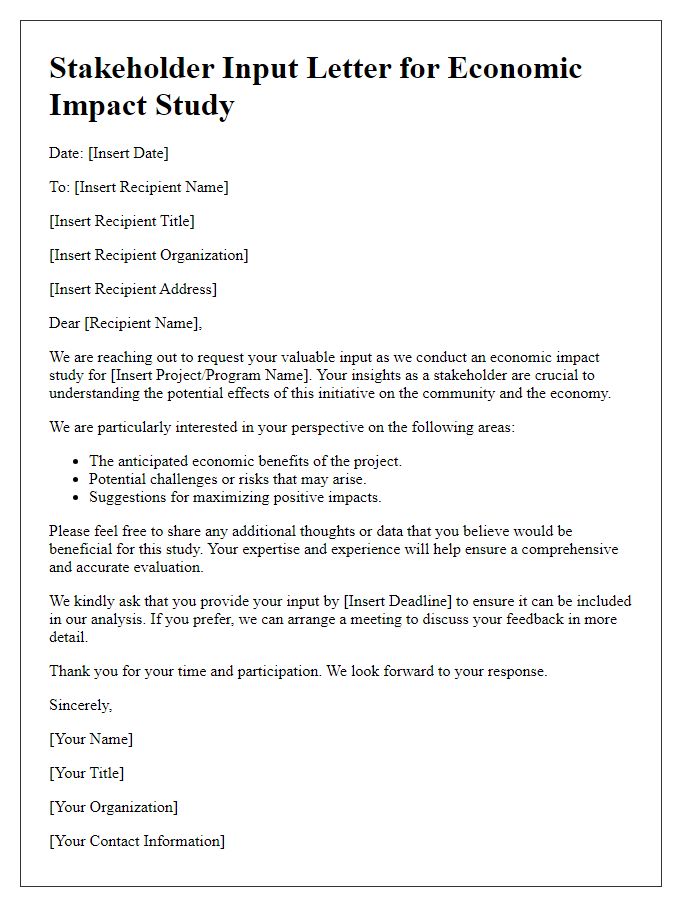

Letter Template For Stakeholder Economic Impact Assessment Samples

Stakeholder identification and categorization

Stakeholder identification is crucial in assessing the economic impact of projects in various sectors, including infrastructure development and community programs. Key stakeholders include local governments, such as city councils or regional authorities, which regulate land use and economic activity. Community members, representing socio-economic groups, influence project acceptance and sustainability, while businesses in the area, such as small retailers or major corporations, are vital for economic growth and job creation. Non-profit organizations play a role in advocacy, ensuring that marginalized populations are considered in impact assessments. Academic institutions contribute research and analysis, providing evidence-based insights into potential economic outcomes. Finally, government agencies at the state level, such as the Department of Economic Development, monitor regulations and provide funding. Proper identification and categorization enable a comprehensive understanding of potential economic impacts and stakeholder interests.

Key economic variables and indicators

An economic impact assessment involves analyzing key economic variables and indicators that provide insight into the financial health and sustainability of a project or investment. Important variables include Gross Domestic Product (GDP) growth rates, unemployment rates, inflation rates, and consumer confidence indices. Regional indicators such as labor market statistics, average income levels, and industry performance metrics also play a crucial role. Additionally, investment in infrastructure projects, job creation numbers, and tax revenue projections can indicate the potential long-term economic benefits. Changes in these variables can significantly influence stakeholder decisions and overall economic viability of initiatives, making it essential to monitor and evaluate them throughout the assessment process.

Long-term sustainability and effects

Stakeholder economic impact assessments focus on evaluating the long-term sustainability and effects of projects or initiatives. Comprehensive analyses consider various factors, including potential job creation, revenue generation, and community development in targeted regions, often involving local economies such as those in urban centers or rural areas. Data collection strategies may include surveys, interviews, and financial reports, providing quantitative metrics such as return on investment (ROI) percentages and employment statistics. Environmental considerations, like resource management or carbon footprint reduction, also play significant roles in determining sustainability. Long-term projections, typically extending over a decade, help stakeholders understand possible scenarios, including economic resilience against downturns or shifts in market dynamics. Engagement with community stakeholders, including local government bodies and business leaders, ensures that assessments reflect diverse perspectives and foster collaborative strategies for sustainable growth.

Data collection and analysis methodologies

Stakeholder economic impact assessments utilize diverse data collection and analysis methodologies to evaluate the effects of projects on local economies. Quantitative methods include surveys administered to businesses within specific regions, such as Los Angeles County, measuring revenue changes, employment statistics, and investment levels. Qualitative assessments often involve focus groups with community members to understand sentiments regarding job creation and infrastructure improvements. Secondary data from government sources, like the Bureau of Economic Analysis, provides critical benchmarks for comparison, enabling analysts to create an economic model that reflects direct, indirect, and induced impacts. Key metrics, such as multiplier effects--typically ranging from 1.5 to 2.5--highlight how initial investments stimulate further economic activity. Furthermore, Geographic Information Systems (GIS) technology can visually represent data patterns, promoting a clearer understanding of spatial economic dynamics. Overall, rigorous methodologies ensure comprehensive assessments that support informed decision-making by stakeholders.

Reporting and communication strategies

An effective stakeholder economic impact assessment requires a strategic approach to reporting and communication. Key methodologies might include quantitative assessments, such as economic modeling (e.g., input-output analysis) and qualitative insights derived from stakeholder surveys. Regular reporting schedules, ideally quarterly, should provide updates on economic indicators, such as employment rates (for example, changes in local job creation statistics) and revenue impacts (like variations in local business sales). Utilizing online platforms, such as dedicated project websites or social media channels, can enhance stakeholder engagement by providing real-time updates. Effective visuals, including infographics and charts, can help convey complex data in an understandable format. Ensuring accessibility of reports in multiple languages (e.g., English and Spanish) fosters inclusivity among diverse stakeholder groups. Finally, establishing feedback mechanisms, such as community forums or stakeholder interviews, creates an ongoing dialogue, promoting transparency and trust among all parties involved.

Read Also: Our Stakeholder's Blogs

Comments