Hey there! As life keeps moving, it's easy to lose track of important dates, especially when it comes to mortgage payments. This article will provide you with a handy letter template that you can use to remind yourself or others about upcoming mortgage payment schedules. Whether it's for personal use or to assist a friend, we've got you coveredâread on to discover how to stay on top of those payments and maintain your financial peace of mind!

Image cover: Letter Template For Mortgage Payment Schedule Reminder

Letter Template For Mortgage Payment Schedule Reminder Samples

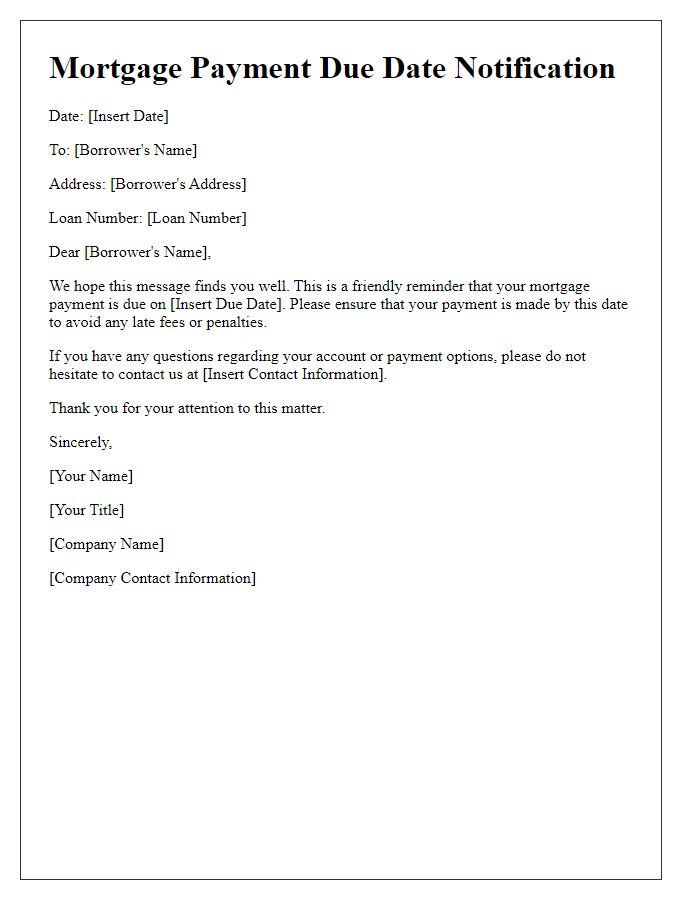

Loan account details

A mortgage payment schedule reminder typically includes critical details about the loan account, ensuring borrowers remain aware of their financial obligations. The loan account number, such as 123456789, provides a unique identifier for tracking and communication purposes. The mortgage lender's name, like XYZ Financial Services, may also be included, along with their contact number (1-800-555-0199) for any inquiries. Payment amounts, for instance, $1,200 due on the first of each month, highlight the financial commitment, while the loan term, such as 30 years, indicates the duration of repayment. Additionally, important dates, including the upcoming payment deadline of November 1, 2023, remind borrowers of their schedule. Special mentions of interest rates, like a fixed rate of 4.5%, and possible late fees--typically around $50--serve to emphasize the importance of timely payments.

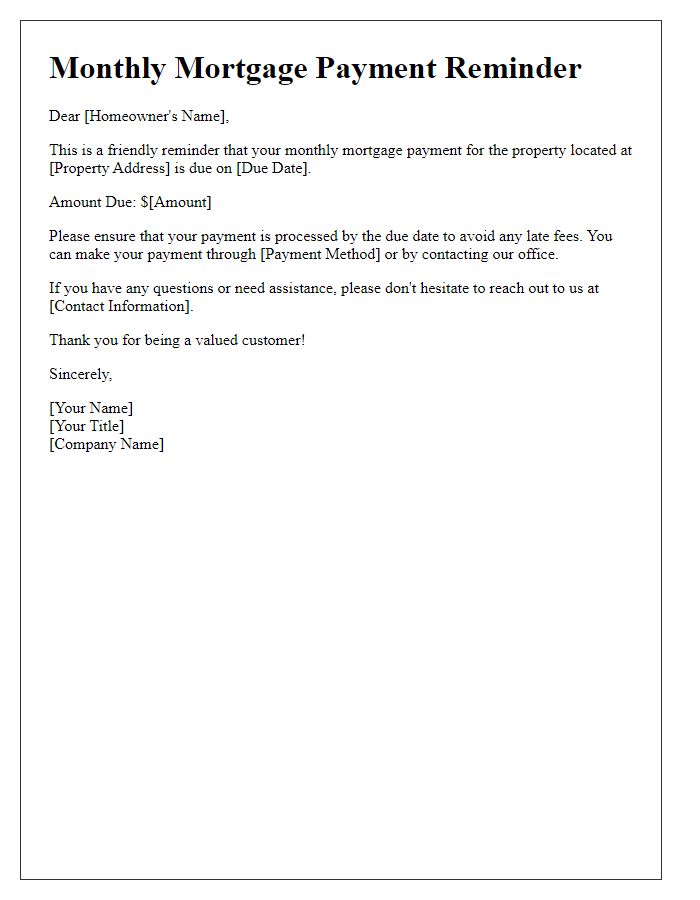

Payment due date

The mortgage payment schedule is crucial for homeowners to maintain financial stability and avoid late fees. The payment due date, typically the first of every month, is the established deadline for submitting mortgage payments. Timely payments contribute to a positive credit score, impacting loan eligibility in the future. Lenders often offer various payment methods, such as online transfers through secure banking apps or checks sent through postal services, ensuring ease of transaction. Homeowners should consider setting reminders or automatic payments to ensure compliance with the schedule and avoid any potential penalties. This proactive approach helps in managing ongoing financial obligations effectively.

Outstanding balance

An outstanding balance on mortgage payments can result in additional fees and interest accumulation for homeowners, leading to long-term financial strain. For instance, a homeowner with a $300,000 mortgage might face increased monthly payments due to missed deadlines. Failure to address these payments within a specified grace period, which typically ranges from 15 to 30 days, can result in default notices sent by financial institutions, such as banks or credit unions. This situation can further complicate credit scores, potentially dropping it below 650, which can hinder future borrowing opportunities. Regular reminders for scheduled payments can help maintain a healthy financial standing and ensure compliance with the mortgage agreement.

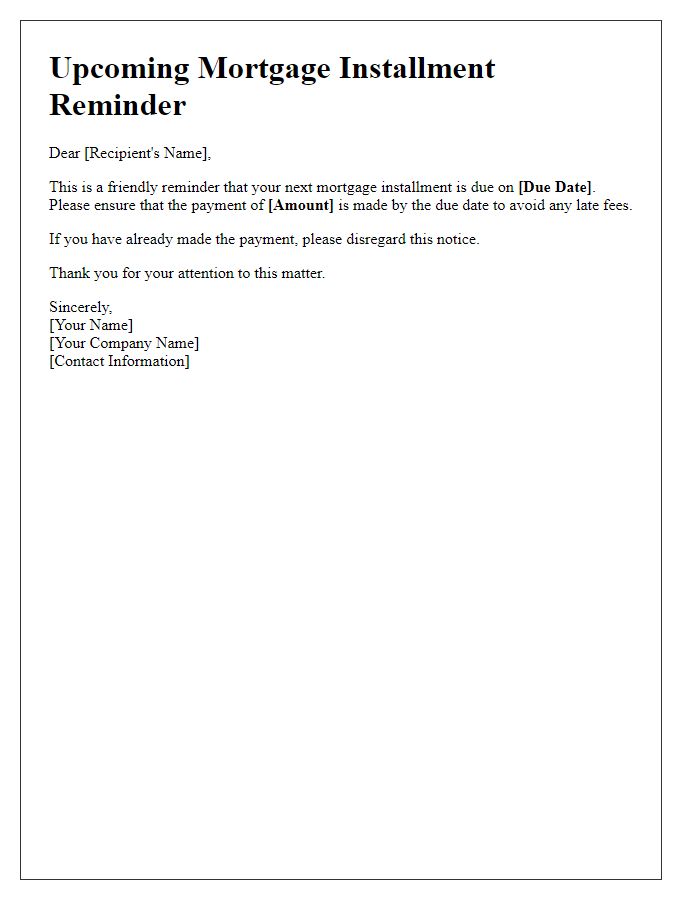

Payment methods available

Mortgage payment schedules play a crucial role in managing home financing effectively. Various payment methods, including online banking, automatic payments, and traditional check methods, are available for homeowners. Online banking allows for seamless transactions and real-time tracking of payment dates while automatic payments ensure timely deductions from checking accounts without manual intervention. Traditional checks remain a reliable option, although they may prolong transaction processing times, especially with the postal service. Homeowners must be aware of specific due dates, often set for the first of each month, to avoid late fees and maintain a good credit standing. Understanding these payment methods facilitates better financial planning and improves the overall mortgage repayment experience.

Late payment consequences

Late mortgage payments can result in significant financial repercussions for borrowers. A missed payment on a mortgage loan, often associated with real estate properties, can incur late fees, typically ranging from 3% to 5% of the overdue amount. Continued delinquency may lead to negative impacts on credit scores, potentially decreasing by as much as 100 points, which can hinder future borrowing opportunities. Additionally, lenders may initiate foreclosure proceedings, a legal process that can take several months to years, threatening the borrower's ownership of the property. It is crucial to communicate with the lender to explore options such as payment plans or forbearance to mitigate these consequences.

Read Also: Our Reminder's Blogs

Comments