Are you in the market for a mortgage lender and feeling overwhelmed by the options? Choosing the right lender can significantly impact your home-buying journey, and it's crucial to find someone who understands your needs. In this article, we'll share some key recommendations and insights from experts in the field to help you make an informed decision. So, grab a cup of coffee and dive in to learn how to choose the perfect mortgage lender for your needs!

Image cover: Letter Template For Mortgage Lender Recommendation

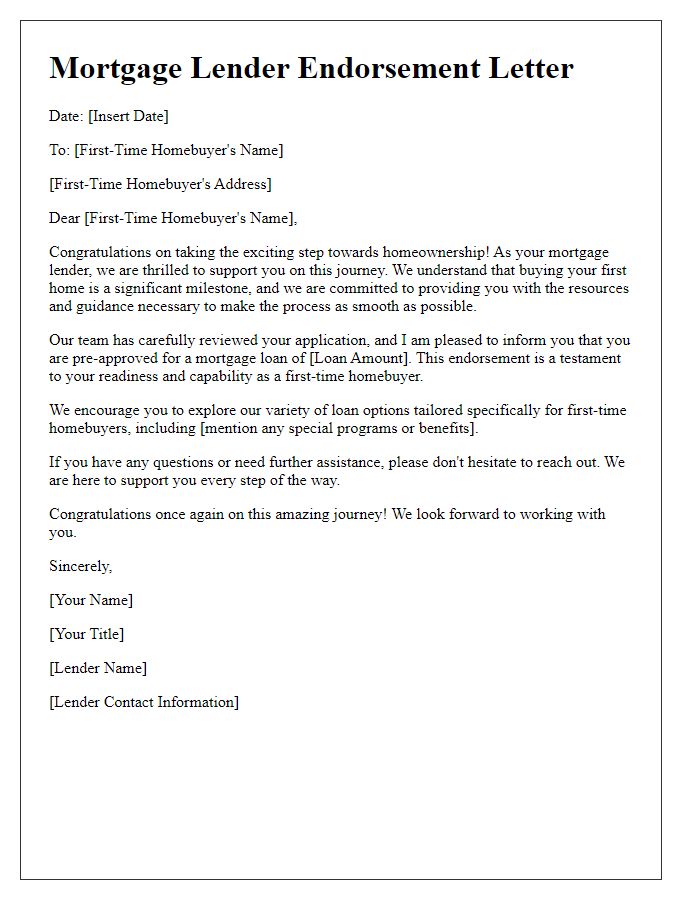

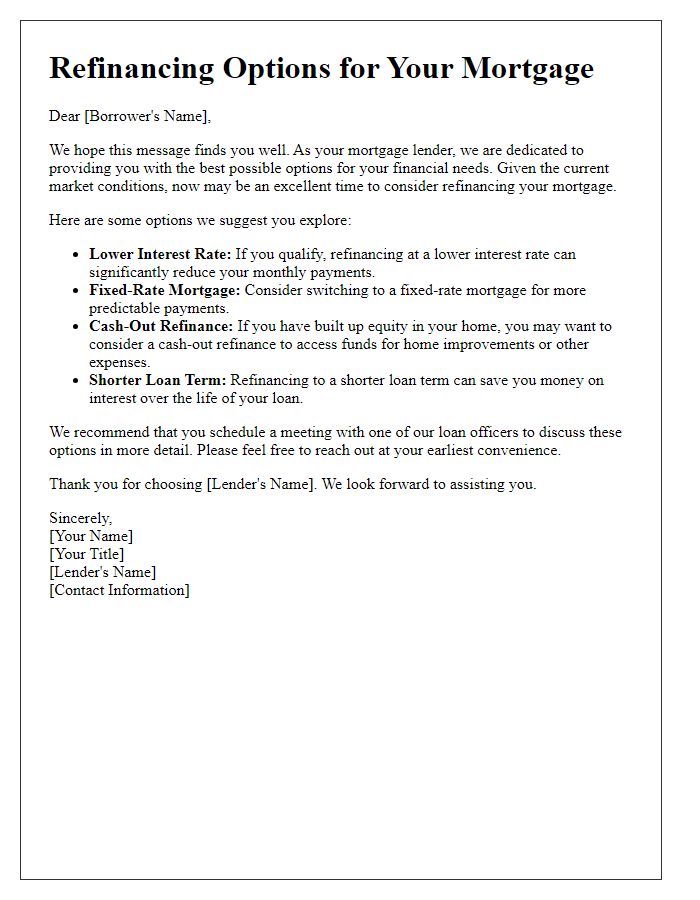

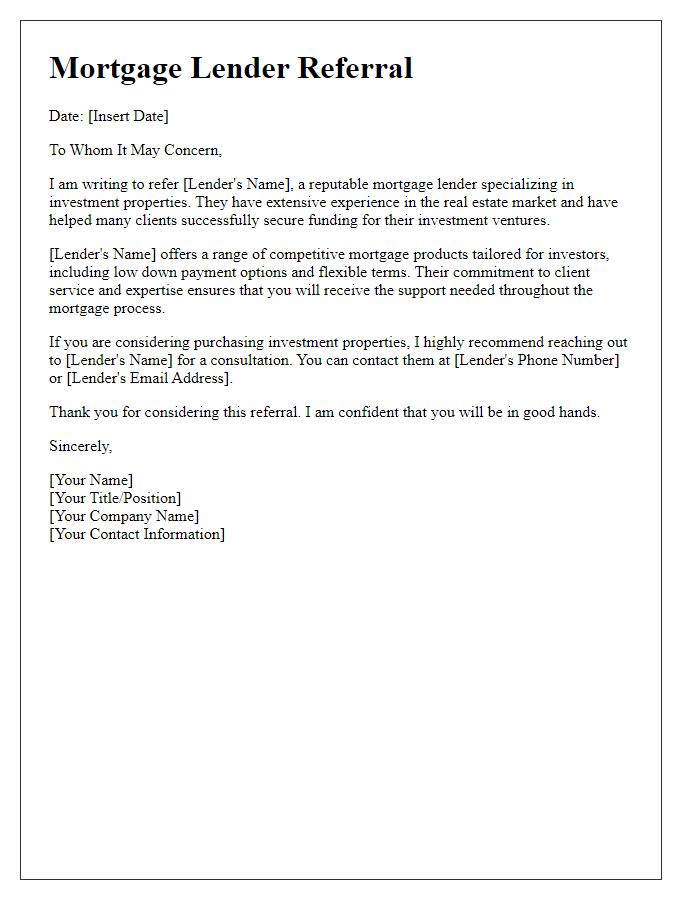

Letter Template For Mortgage Lender Recommendation Samples

Borrower's Financial Stability

A borrower's financial stability is a critical factor in determining their mortgage eligibility, especially when assessing factors such as income, debt-to-income ratio, and credit score. Consistent employment history, ideally spanning over two years, in reputable organizations is vital, as it showcases reliability. A gross annual income of at least $75,000 can support mortgage applications for properties valued at approximately $300,000, while maintaining a debt-to-income ratio below 36% indicates responsible financial management. Additionally, a credit score above 700, as provided by major credit bureaus like Experian, TransUnion, and Equifax, reflects good credit habits. Savings reserves, ideally covering three to six months of mortgage payments, enhance a borrower's profile, providing reassurance to lenders about their ability to manage unexpected expenses.

Credit History and Score

A strong credit history and favorable credit score are crucial for securing a mortgage with lenders like Wells Fargo or Bank of America. Typically, a credit score above 740 is considered excellent and can open the door to lower interest rates. Credit reports contain detailed records of payments, outstanding debts, and public records such as bankruptcies or liens, which can significantly influence lender decisions. Consistent punctual payments demonstrate reliability, while a low credit utilization ratio (ideally below 30%) showcases responsible credit management. Regularly reviewing credit reports from agencies like Experian or TransUnion can help borrowers identify and rectify any errors, further strengthening their application for a mortgage.

Property Details and Appraisal

A comprehensive appraisal is essential in assessing the value of real estate properties, especially in the context of mortgage lending. Properties located in urban areas, such as New York City, may experience valuation fluctuations based on market trends, with average home prices reaching approximately $1 million in 2023. An appraisal typically includes an evaluation of comparable property sales, also known as "comps," which refer to similar real estate transactions within the same neighborhood. Factors influencing property value include the overall condition of the property, square footage (often measured in thousands of square feet), and location-specific attributes such as proximity to schools, parks, and public transportation. This detailed analysis helps lenders make informed decisions when considering mortgage applications, ensuring responsible lending practices while protecting their investment portfolios.

Loan-to-Value Ratio

The Loan-to-Value (LTV) ratio is a critical metric in mortgage lending, representing the relationship between the amount of the loan and the appraised value of the property, expressed as a percentage. For instance, an LTV of 80% indicates that a borrower is financing 80% of the property's value while providing a 20% down payment, which is typically considered favorable by lenders. High LTV ratios, exceeding 80%, often result in additional costs such as private mortgage insurance (PMI) to mitigate lender risk. The LTV ratio significantly influences mortgage interest rates, loan terms, and overall approval likelihood. Lenders generally prefer lower LTV ratios, viewing them as indicative of a borrower's reduced risk profile in competitive housing markets, like San Francisco or New York City, where property values can fluctuate dramatically.

Income Verification and Documentation

Income verification is a crucial aspect of the mortgage application process, as lenders, such as Wells Fargo or Quicken Loans, require comprehensive documentation to assess a borrower's financial stability. Essential documents include recent pay stubs, typically covering the last 30 days, and W-2 forms from the previous two tax years to verify employment and income sources. Self-employed applicants may need to provide additional paperwork, such as profit and loss statements and 1099 tax forms, often spanning two years to illustrate consistent revenue streams. This verification process not only ensures that borrowers can reliably meet loan repayment terms but also helps lenders, including Bank of America or Chase, mitigate risk during the lending process. Properly organized income documentation enhances approval chances, leading to a smoother mortgage acquisition experience.

Read Also: Our Real estate agent's Blogs

Comments