Are you looking to boost your credit score and take control of your financial future? Understanding the key factors that influence your credit score can make all the difference, from timely payments to managing credit utilization wisely. With a few simple strategies and a bit of dedication, you can see significant improvements over time. So, let's dive into these credit score improvement tips and unlock the potential for a brighter financial path!

Image cover: Letter Template For Credit Score Improvement Tips

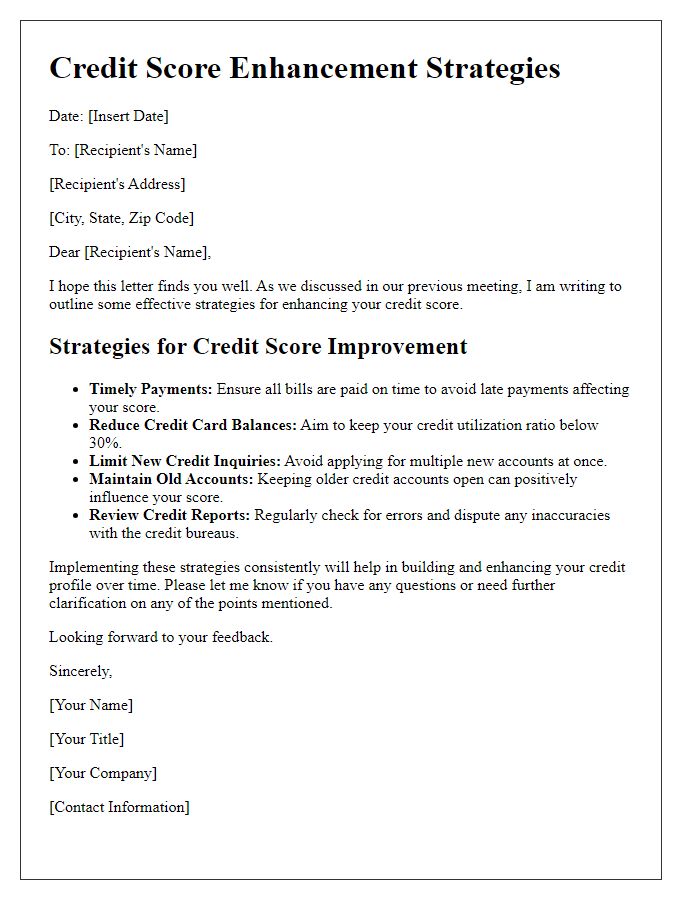

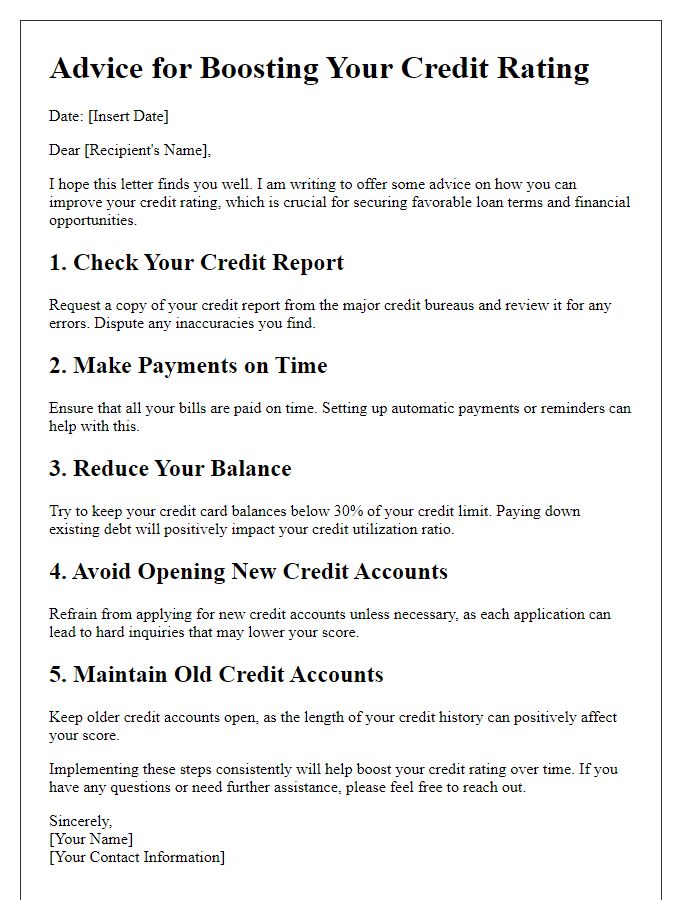

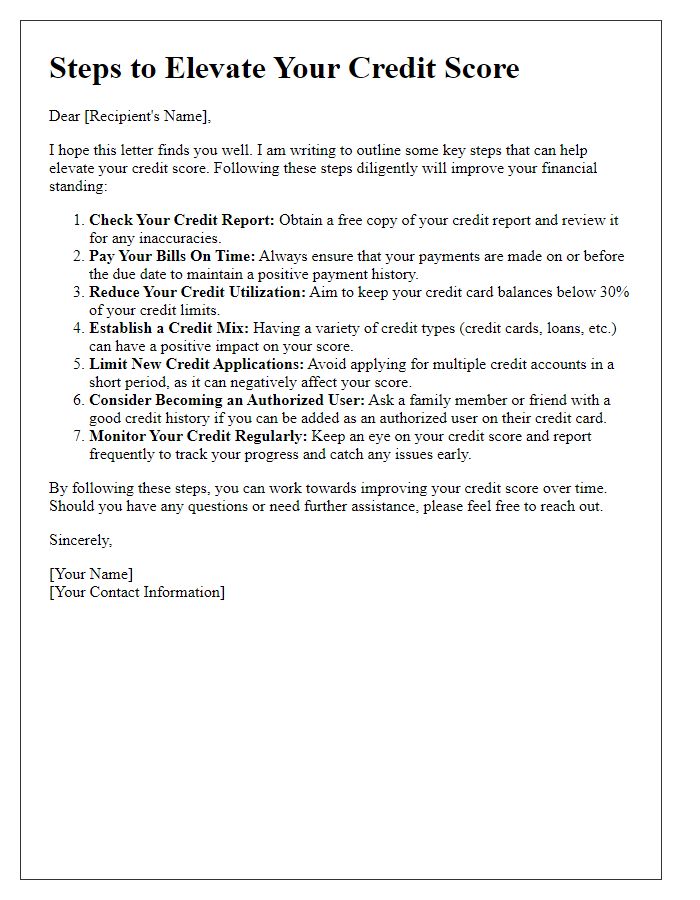

Letter Template For Credit Score Improvement Tips Samples

Personalized Credit Report Assessment

A personalized credit report assessment can significantly enhance an individual's understanding of their credit score dynamics. This assessment involves reviewing key components of the credit report, such as payment history, which accounts for 35% of the credit score and reflects punctuality in bill payments. Another essential factor is credit utilization ratio, ideally kept below 30% of available credit limits, impacting 30% of the overall score. The length of credit history, which typically includes details of accounts open for over 15 years, also plays a critical role in demonstrating creditworthiness. Additionally, a healthy mix of credit types, like revolving accounts and installment loans, can positively influence the score. Regular monitoring of credit inquiries, particularly hard inquiries from loan applications, provides insights into potential impacts on the score. Leveraging these factors can guide individuals in crafting strategies for credit score improvement, maximizing financial opportunities and securing better loan rates in the future.

Payment History Review and Correction

Reviewing and correcting payment history is crucial for improving credit scores, especially for individuals with a credit file consisting of missed payments and late accounts. Payment history accounts for approximately 35% of a credit score, according to FICO scoring models. Regularly checking credit reports from major agencies like Experian, TransUnion, and Equifax can uncover errors that may negatively impact scores. Individuals should focus on identifying late payments, which can significantly drop scores, and make timely corrections. Disputing inaccuracies online through respective agency websites can initiate prompt changes. Moreover, establishing timely payment habits by setting up reminders or automatic payments can foster positive credit history, ultimately leading to better credit scores.

Credit Utilization Optimization Techniques

Credit utilization, a crucial factor in determining credit scores, represents the ratio of a borrower's current credit card balances to their total credit limits. Ideally, maintaining a credit utilization ratio below 30% is recommended for optimal credit health. Techniques to improve credit utilization include paying down existing balances before the statement date, which reduces the amount reported to credit bureaus. Additionally, increasing credit limits on existing accounts, either by requesting a limit increase or applying for new cards, enhances available credit, thereby lowering utilization ratios. Regular reviewing of credit reports through platforms like AnnualCreditReport.com helps identify discrepancies that may affect utilization calculations negatively. Adopting responsible spending habits and making multiple smaller payments throughout each month can also keep balances low and positively influence credit scores over time.

Effective Debt Management Strategies

Effective debt management strategies significantly enhance credit score performance. Prioritizing timely payments (at least 30 days late can negatively impact scores) can substantially aid in elevation of numerical ratings. Utilizing budgeting tools and apps can help track expenses and allocate funds for debt repayment systematically. Implementing the debt snowball method, where smaller debts are paid off first, can build momentum and motivation. Regularly reviewing credit reports from the three major bureaus--Experian, Equifax, and TransUnion--can identify inaccuracies (up to 25% of reports may contain errors) and allow for timely dispute resolutions. Keeping credit utilization below 30% on revolving accounts (credit cards) further contributes to score improvement, as high utilization ratios are viewed negatively by lenders. Adopting these strategies can lead to healthier credit management and improve long-term financial outcomes.

Long-term Financial Planning Guidance

Long-term financial planning involves a strategic approach to managing finances over an extended period, ensuring stability and growth. Regularly monitoring your credit score, which ranges from 300 to 850, is vital for securing loans at favorable interest rates. Implementing a budget that accounts for monthly expenses, income, and savings goals can aid in making informed financial decisions. Paying bills on time contributes significantly to improving credit history, as payment history constitutes 35% of the credit score calculation. Reducing existing debt, particularly on credit cards which can have high-interest rates, will enhance credit utilization ratio--keeping it below 30% is ideal for building a healthy credit profile. Moreover, diversifying credit types, such as having a mix of installment loans and revolving credit, can further bolster your credit score over time. Regularly checking credit reports from major agencies like Experian, TransUnion, and Equifax for errors is essential; disputing inaccuracies can lead to score improvements. Establishing an emergency fund, ideally filled with three to six months' worth of living expenses, adds financial security, preventing reliance on credit in times of need, thereby contributing to a more robust financial future.

Read Also: Our Real estate agency's Blogs

Comments