Improving your credit score is essential for securing better financial opportunities, and it all starts with a solid plan. Whether you're looking to buy a home, finance a car, or simply want to boost your creditworthiness, understanding the steps involved can make a world of difference. In this article, we'll explore effective strategies to help you enhance your credit score and achieve your financial goals. So, let's dive in and discover how you can take control of your credit journey!

Image cover: Letter Template For Credit Score Improvement Plan

Letter Template For Credit Score Improvement Plan Samples

Personal information

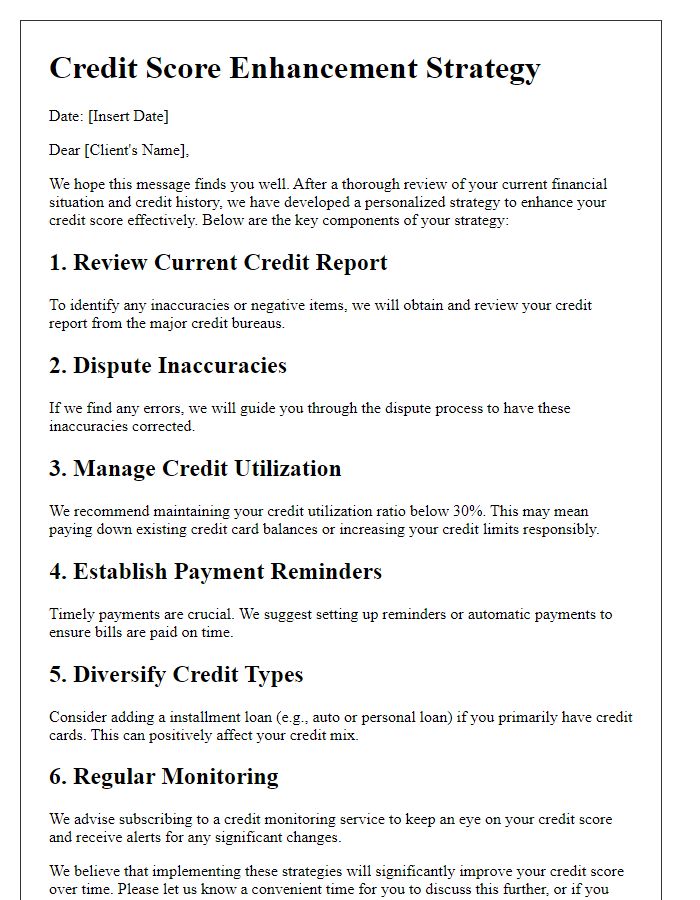

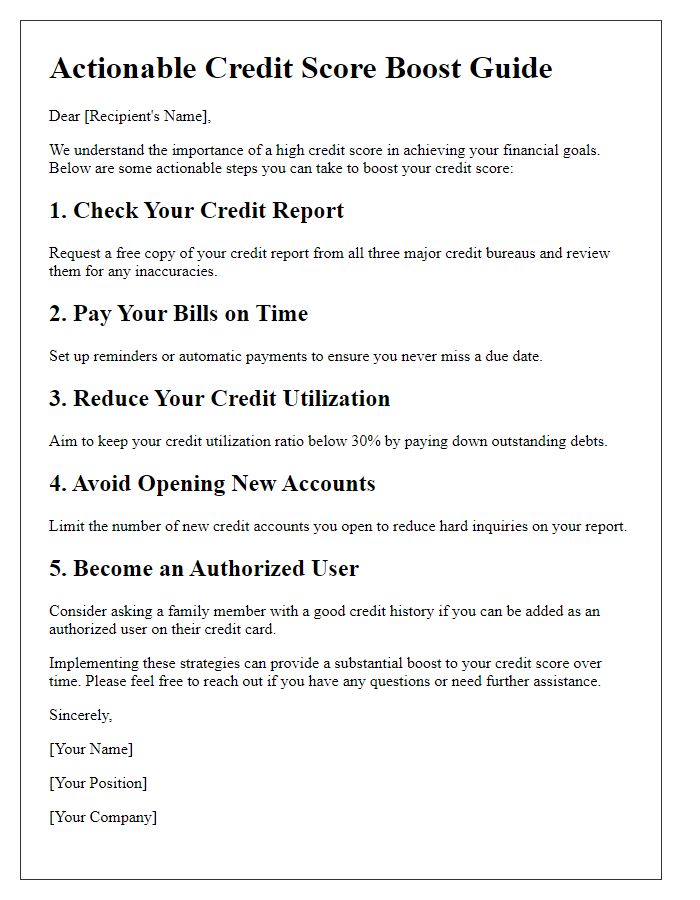

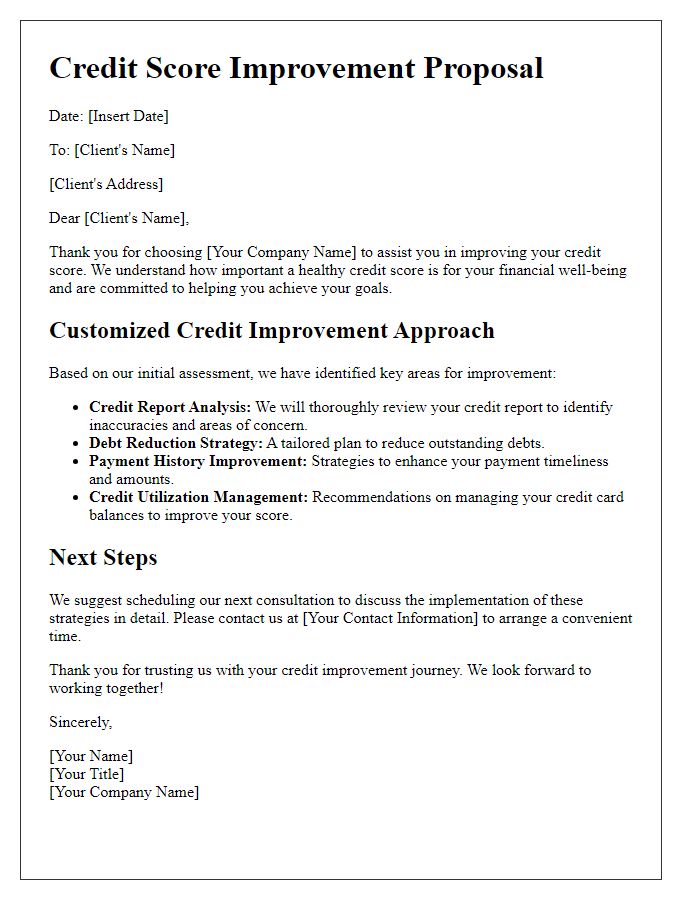

A credit score improvement plan outlines methods to enhance financial credibility and optimize personal creditworthiness. Essential components include identifying personal information such as full name, Social Security number (typically nine digits), address (including city, state, and zip code), date of birth, and employment details (including employer name and job position). Each factor influences credit score calculations, which generally range from 300 to 850. Regular monitoring of your credit report from major agencies like Experian, Equifax, and TransUnion can unveil inaccuracies or negative items requiring dispute. Establishing timely bill payments, reducing credit utilization ratio (ideally below 30 percent), and maintaining diverse types of credit accounts further bolster the credit profile. Integrating these strategies into a structured plan can systematically improve overall credit standing.

Current credit status

Current credit status reveals significant aspects influencing financial health. Various credit bureaus, including Experian, TransUnion, and Equifax, provide credit scores typically ranging from 300 to 850. A score below 580 is often considered poor, while scores between 580 and 669 are viewed as fair. Key factors affecting credit scores include payment history, credit utilization ratio, length of credit history, types of credit accounts, and recent inquiries. Payment history has a substantial impact, representing approximately 35% of the score, indicating the importance of consistently meeting payment deadlines. Furthermore, maintaining a credit utilization ratio below 30% is advisable to positively influence scores. Regular monitoring of credit reports (available annually at AnnualCreditReport.com) enables individuals to identify and correct discrepancies that may negatively impact their credit status.

Specific credit issues

A comprehensive credit score improvement plan addresses specific credit issues, including late payments, high credit utilization, and derogatory marks. Late payments, specifically over 30 days overdue, can significantly decrease scores (up to 100 points in some cases). High credit utilization ratios, particularly those exceeding 30%, may indicate financial strain and impact overall creditworthiness. Derogatory marks, such as bankruptcies (which remain on reports for up to 10 years), further complicate recovery efforts. Consistently making on-time payments, reducing credit card balances, and disputing inaccuracies on credit reports can enhance credit scores methodically. Regular monitoring through services like FICO can provide insights on progress and necessary adjustments to strategies.

Proposed strategies

To improve credit scores effectively, various strategies should be implemented. Key strategies include consistently paying bills on time, as timely payments contribute positively to credit history. Additionally, reducing credit utilization below 30% of available credit limits can enhance credit scores significantly; for example, a total credit limit of $10,000 should ideally have a balance of no more than $3,000. Regularly reviewing credit reports from major bureaus, like Experian and TransUnion, can help identify and rectify errors that might negatively impact scores. Moreover, diversifying credit types, such as including installment loans alongside credit cards, can demonstrate responsible credit management. Lastly, avoiding opening new credit accounts too frequently is crucial; each new inquiry can reduce scores temporarily. These strategies create a comprehensive approach to credit score improvement.

Timeline and goals

A credit score improvement plan requires a structured timeline and specific goals to enhance financial health effectively. Initially, reviewing credit reports from major agencies, such as Experian, Equifax, and TransUnion, is crucial within the first week to identify discrepancies or outdated information. Setting a goal of disputing any inaccuracies within two weeks can help eliminate potential negative impacts on the score. Establishing a budget by the end of the month to pay down outstanding debts, targeting credit card balances that should ideally be below 30% utilization, is essential. Aiming for timely payments can be implemented immediately, with a goal to maintain this habit over the next six months. Additionally, opening a secured credit card within the first three months can build positive credit history, while checking the progress of the credit score every 30 days ensures accountability and adjustments to the plan as needed. Engaging with a financial advisor by the end of the fourth month could provide personalized strategies to accelerate improvement beyond the initial goals, potentially resulting in a 50-point increase in credit score within six to twelve months.

Read Also: Our Bank's Blogs

Comments