Are you dreaming of owning your own home but feeling overwhelmed by the loan application process? You're not aloneâmany first-time buyers find themselves confused by the various steps and requirements. Fortunately, with the right guidance and resources, securing a home loan can be a smooth experience. Dive into our article for expert tips and a handy letter template to assist you in your home loan application journey!

Image cover: Letter Template For Home Loan Application Assistance

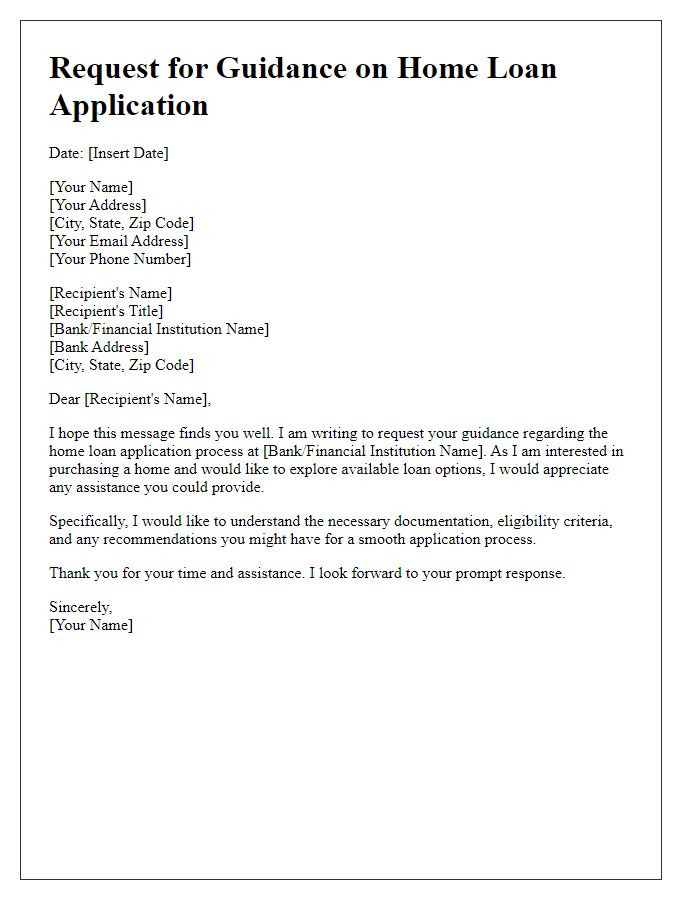

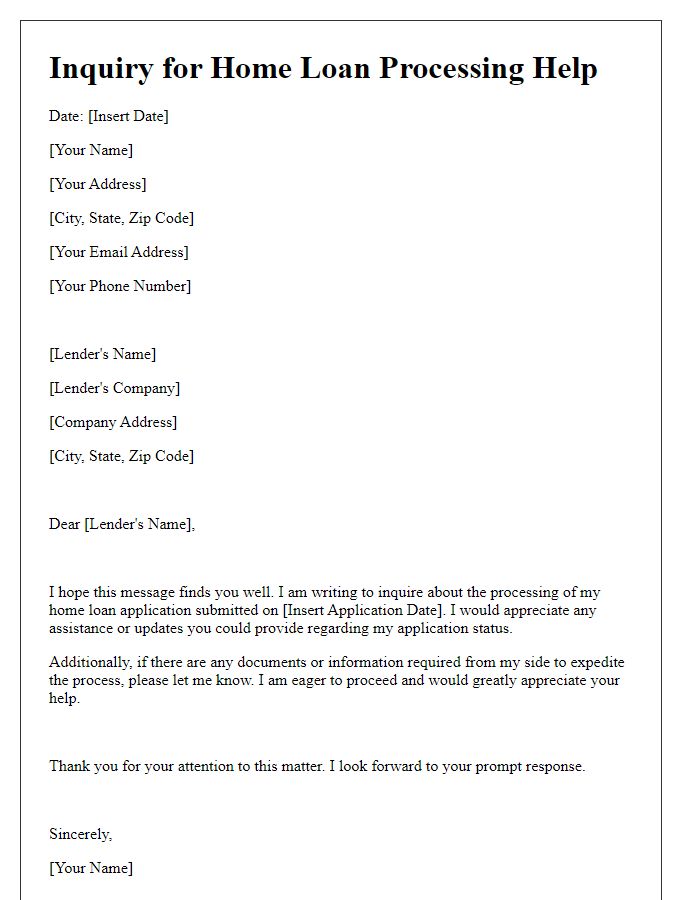

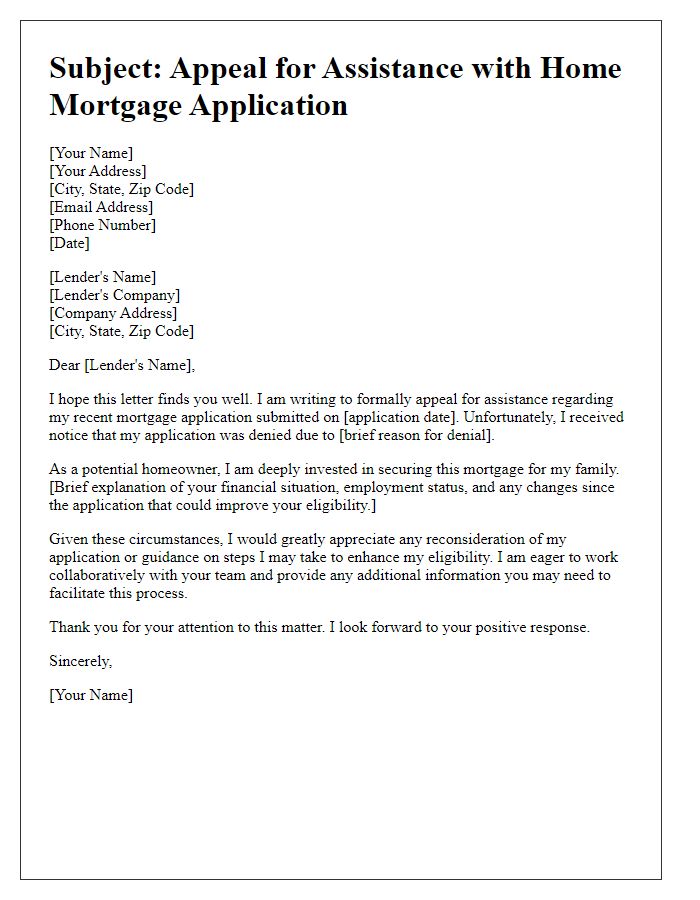

Letter Template For Home Loan Application Assistance Samples

Personal Identification Information

Personal identification information is crucial for processing home loan applications. Key documents include a government-issued photo ID, such as a driver's license or passport, providing verifiable identification. Social Security numbers must be accurate to ensure unique identification during the loan evaluation process. Additionally, proof of residence, consisting of utility bills or lease agreements from the past three months, confirms current living situations. Financial documents like recent pay stubs, bank statements, and tax returns from the last two years are essential to validate income and financial stability. Affordability assessments often require information about existing loans, credit card balances, and outstanding debts, which help lenders determine the applicant's creditworthiness.

Employment and Income Details

Employment verification is crucial in the home loan application process. Accurate documentation of employment status, company name, role, and duration is required. Lenders often request pay stubs, bank statements, and tax returns (typically for the last two years) to assess monthly income and stability. Full-time positions in established companies, especially those with a consistent income, enhance approval chances. For self-employed individuals, a detailed profit and loss statement may be necessary. Moreover, income types such as salary, bonuses, commissions, and other compensations must be clearly documented to provide a comprehensive view of financial reliability.

Loan Amount and Purpose

When applying for a home loan, clearly articulating the loan amount and purpose is crucial. A requested loan amount of $350,000 may be necessary to purchase a three-bedroom home located in Denver, Colorado, particularly in neighborhoods known for their excellent schools, such as Cherry Creek and Wash Park. This loan will facilitate the acquisition of a property with designated areas for family gatherings and easy access to parks and recreational facilities. Additionally, detailing specific renovations, such as kitchen upgrades or energy-efficient windows, can further illustrate the purpose of the loan, offering potential lenders a comprehensive view of financial needs and future value enhancements.

Financial Status Overview

A comprehensive financial status overview is essential for a successful home loan application, highlighting crucial elements like credit score, income, and debt-to-income ratio. The average credit score for applicants typically ranges from 300 to 850, with a score above 740 deemed favorable for lower interest rates. Monthly income, including salaries and additional income sources like rental or investment returns, should be documented, reflecting stable earnings typically above $50,000 annually for most applicants. Debt-to-income ratio, calculated by dividing monthly debt obligations by gross monthly income, is ideally below 36% to indicate financial stability. Additionally, an overview of assets, including savings accounts, stocks, bonds, and retirement accounts, can strengthen the application, showcasing the applicant's financial health and ability to manage mortgage repayments effectively.

Contact Information and Availability

Seeking home loan application assistance often requires detailed contact information, including email addresses, phone numbers, and preferred means of communication. Availability plays a critical role in the process; specifying times during the week when the client is free can streamline appointments and discussions with loan officers. Setting clear expectations about response times, such as typical hours (9 AM to 5 PM), helps ensure efficient communication. Additionally, including alternate contacts, such as family members or financial advisors, can facilitate smooth interactions if the primary applicant is unavailable. This organized approach can enhance the overall experience and improve the chances of a successful loan application.

Read Also: Our Real estate firm's Blogs

Comments