Are you looking to maximize your investments while minimizing your tax burden? Crafting an investment tax efficiency plan can be a game-changer for your financial strategy, allowing you to keep more of your hard-earned money in your pocket. By understanding the nuances of tax-efficient investing, you can make informed decisions that align with your long-term goals. Join me as we explore effective strategies and tips to boost your investment returnsâread on to discover how to optimize your financial future!

Image cover: Letter Template For Investment Tax Efficiency Plan

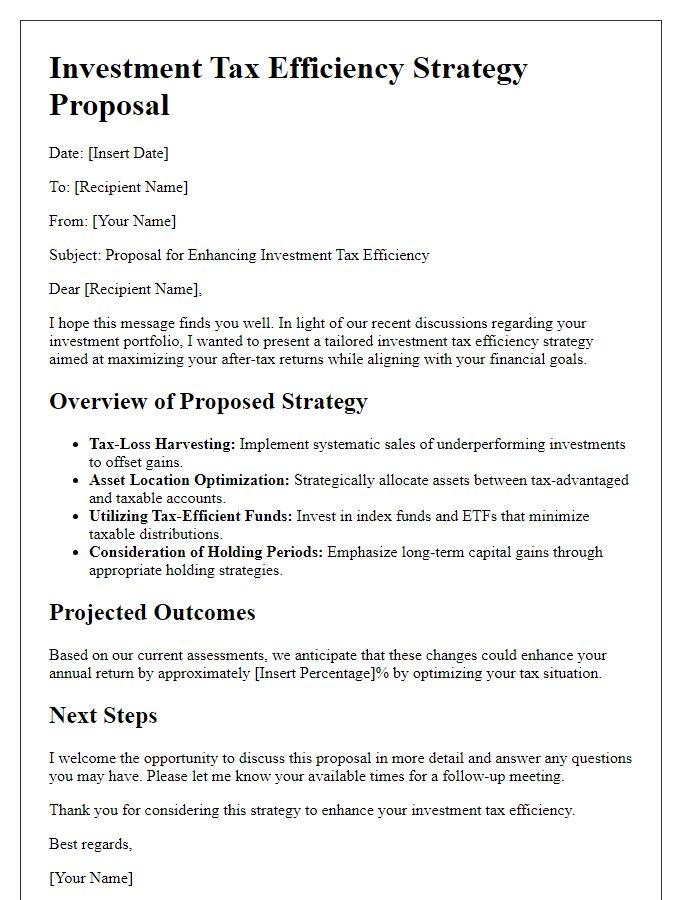

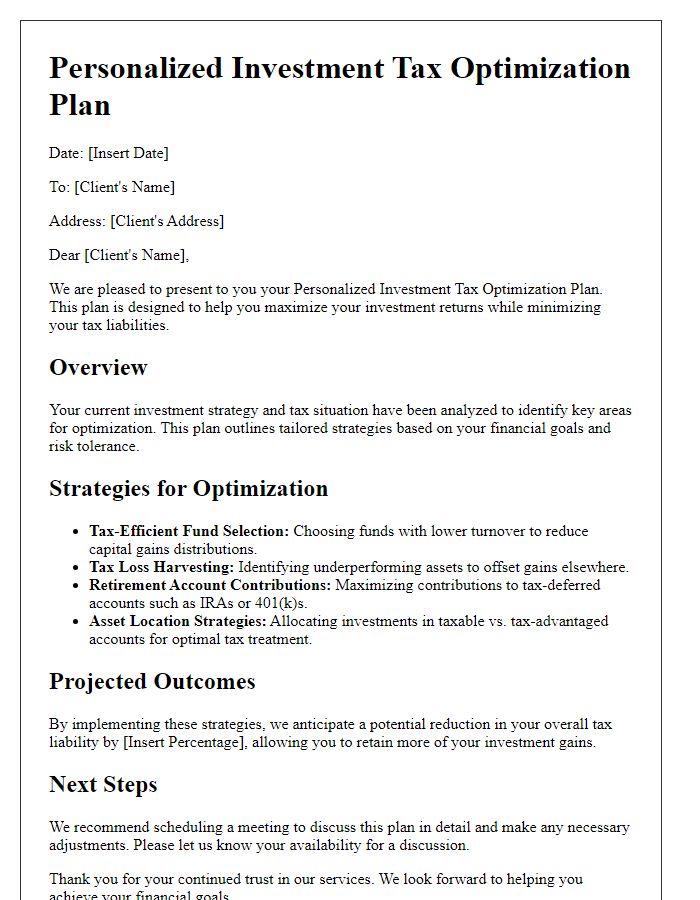

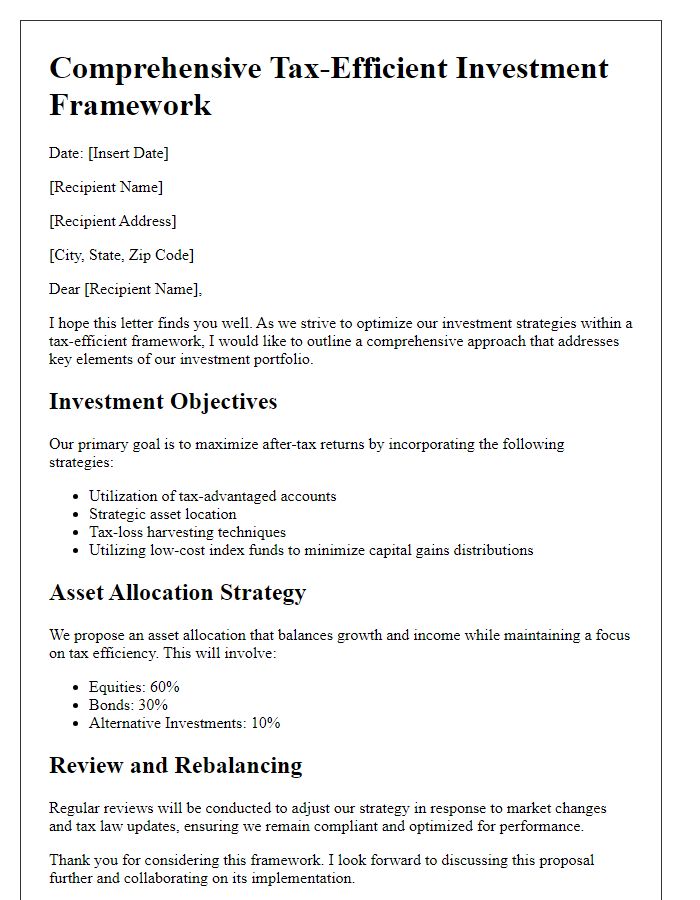

Letter Template For Investment Tax Efficiency Plan Samples

Investment account types and tax implications

Investment accounts vary in structure and tax implications, influencing how investors optimize returns while minimizing tax burdens. Taxable brokerage accounts expose investors to capital gains tax rates (15% to 20% for higher earners) on profits from asset sales. In contrast, tax-advantaged accounts such as Individual Retirement Accounts (IRAs) and 401(k) plans allow for tax-deferred growth or tax-free withdrawals (in the case of Roth IRAs), depending on the type chosen. Additionally, 529 plans provide tax benefits for educational savings, offering tax-free withdrawals when used for qualified education expenses. Understanding the implications of each account type is crucial in crafting a comprehensive investment tax efficiency plan that aligns with personal financial goals and timelines.

Asset allocation and diversification strategies

Effective investment tax efficiency plans focus on strategic asset allocation and diversification to maximize returns while minimizing tax liabilities. Investments in tax-advantaged accounts, like Individual Retirement Accounts (IRAs) or 401(k)s, help defer taxes until withdrawal, which usually occurs during retirement when individuals may be in a lower tax bracket. The inclusion of municipal bonds, which provide tax-free income at the federal level, can enhance tax efficiency. Diversifying across various asset classes, such as equities, fixed income, and alternative investments, can reduce risk while optimizing tax efficiencies. Employing tax-loss harvesting strategies allows investors to offset capital gains with losses, further enhancing after-tax returns. Regular portfolio rebalancing maintains a targeted asset allocation, ensuring alignment with risk tolerance and investment objectives, thus safeguarding overall investment tax efficiency.

Timing of capital gains and tax-loss harvesting

Capital gains taxes represent a significant financial consideration for investors during their investment journey. The timing of capital gains realization can drastically affect tax liabilities, especially when held for over one year, qualifying for the long-term capital gains tax rates, which can be lower than short-term rates. Tax-loss harvesting, a strategic approach to offset gains, allows investors to sell underperforming assets, realizing losses that can be used to reduce their taxable gains. This process requires careful management of investment portfolios to ensure compliance with regulations while capitalizing on losses. Effective planning should account for market conditions, individual income levels, and overall financial goals to optimize the investment tax efficiency plan. Notably, the end of the fiscal year often presents an opportune moment for reviewing portfolios and making decisions regarding capital gains and losses to minimize tax burdens.

Potential changes in tax regulations

Investment tax efficiency plans must consider potential changes in tax regulations that can impact net returns. Legislative developments (such as the Tax Cuts and Jobs Act of 2017) may alter capital gains tax rates, which currently stand at 0%, 15%, or 20% depending on income levels. Modifications in tax-free savings accounts, such as Roth IRAs, could limit contributions or alter withdrawal policies. Additionally, state tax considerations, particularly in high-tax states like California and New York, may affect overall tax liability. Investors must stay informed about proposals in Congress, such as adjustments to estate tax exemptions, which could reach $12.06 million per individual for 2023. Regular evaluations of tax-loss harvesting strategies can optimize portfolio efficiency, reducing taxable income. Active engagement with financial advisors can ensure strategies remain effective under evolving tax landscapes.

Long-term financial goals and risk management

Creating a sustainable investment tax efficiency plan is essential for achieving long-term financial goals while effectively managing risk. The plan should focus on various investment vehicles like tax-advantaged retirement accounts (such as 401(k)s or IRAs), which can significantly reduce taxable income. Specific asset classes, including stocks, bonds, and mutual funds, must be prioritized based on their potential tax implications. Regular portfolio rebalancing is necessary to minimize capital gains taxes, ideally utilizing strategies such as tax-loss harvesting, which involves selling losing investments to offset gains. Additionally, understanding the impact of holding periods on capital gains taxes can help in making informed decisions about when to sell. Investors should also consider the significance of their individual tax bracket, as the efficiency of investment strategies may differ based on income levels and changes in tax laws. Risk management techniques such as diversification across different sectors and geographical regions can mitigate potential losses while ensuring strong long-term growth. Finally, periodic reviews of the investment tax efficiency plan with a financial advisor will ensure that the strategy aligns with evolving financial goals and adheres to the latest tax regulations.

Read Also: Our Investor's Blogs

Comments