Navigating the world of student loans can feel overwhelming, but you're not alone in this journey. Many students find themselves juggling various loans, interest rates, and repayment plans, making it essential to have solid advice at your fingertips. Understanding the nuances of student loans can help you make informed decisions that will positively impact your financial future. So, let's dive into some tips that can simplify your loan experience and set you on a path toward financial success!

Image cover: Letter Template For Student Loan Advice

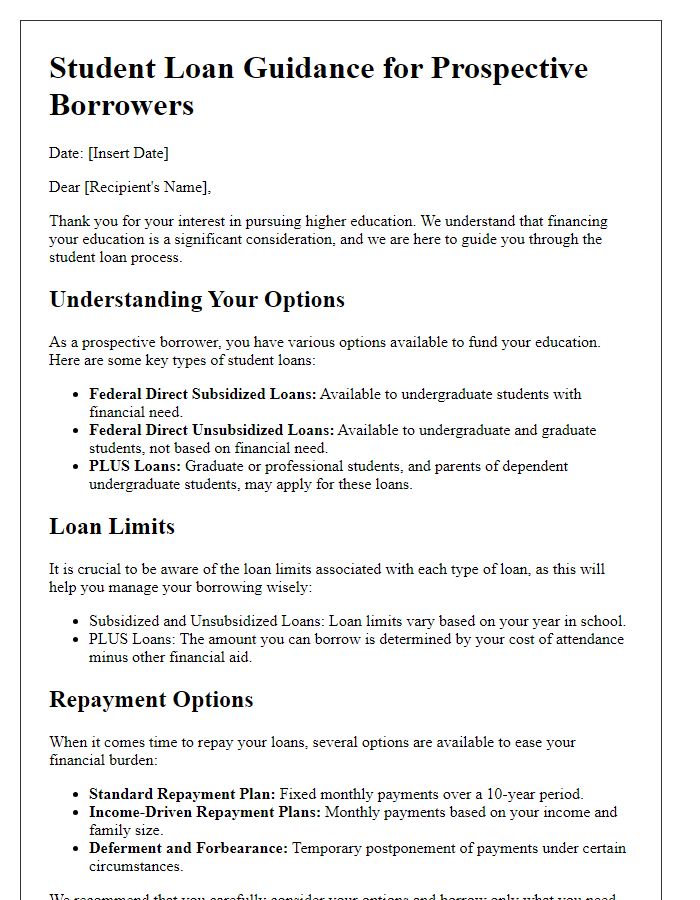

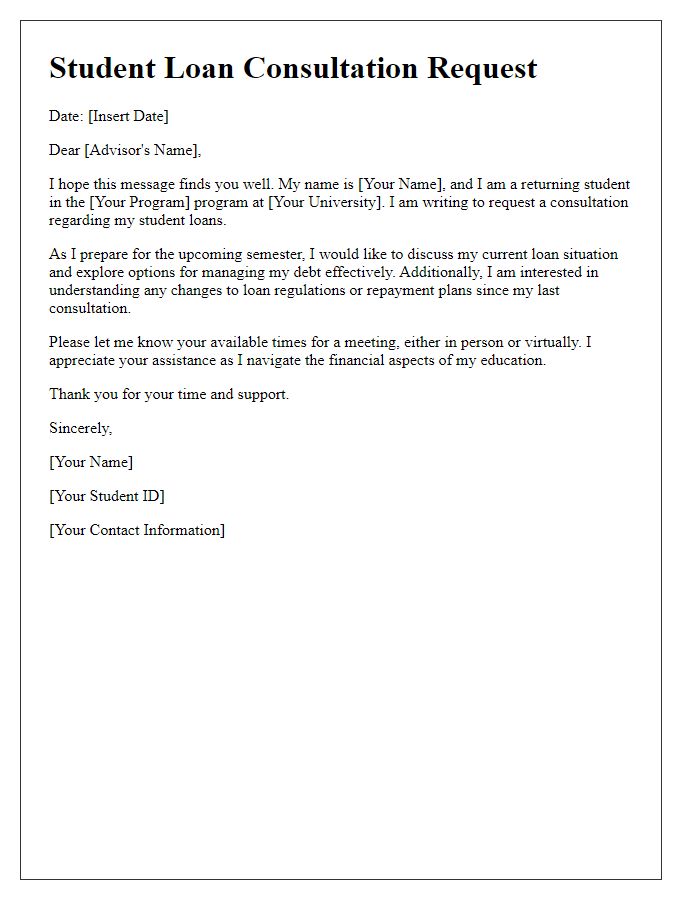

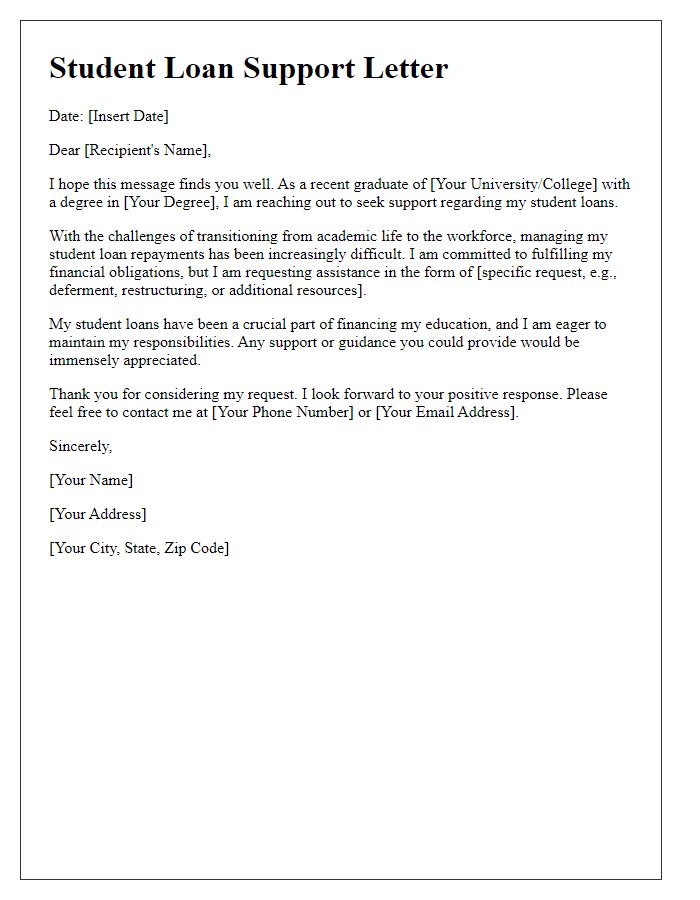

Letter Template For Student Loan Advice Samples

Loan Terms and Conditions

Understanding loan terms and conditions is crucial for students seeking financial assistance. Federal student loans, such as Direct Subsidized and Unsubsidized Loans, have interest rates set by the government, which for the 2023-2024 academic year is 5.5% for undergraduates. Repayment typically starts six months after graduation or dropping below half-time enrollment. Private student loans, offered by banks and credit unions, often have variable interest rates ranging from 4% to 12%, depending on the borrower's credit score and market conditions. Deferred repayment options might be available, allowing students to focus on education without immediate financial pressure. Loan forgiveness programs, especially those tied to public service jobs, present additional long-term financial strategies that can significantly reduce the overall loan burden. Understanding these factors helps students make informed decisions about their financial future.

Repayment Options

Student loan repayment options offer various plans tailored for borrowers' financial situations. Federal student loans, issued by the Department of Education, provide standard repayment (fixed monthly payments over 10 years), graduated repayment (lower payments that increase every two years), and income-driven repayment plans (payments based on income). Private loans from institutions like Wells Fargo or Chase may come with different terms, often requiring immediate repayment with limited flexibility. Borrowers in financial distress can explore deferment (temporary postponement of payments) or forbearance (temporary reduction or suspension of payments). Students should assess their loan types, interest rates, and financial circumstances when choosing a repayment strategy, considering potential forgiveness programs for public service or income-driven plans that may offer loan cancellation after a set number of qualifying payments.

Interest Rates and Accrual

Understanding student loan interest rates is crucial for managing education debt effectively. Federal student loans, such as Direct Subsidized Loans, typically have fixed interest rates around 3.73% for undergraduates as of the 2023-2024 academic year. Private loans, varying significantly based on creditworthiness, can range from 4% to over 12%. Interest accrual starts immediately for some loans while others, like subsidized loans, do not accrue interest while students are enrolled at least half-time. For borrowers with unsubsidized loans or private loans, interest begins to accumulate right after disbursement, which can significantly increase the total amount owed over time. Understanding these factors is essential for strategic repayment planning and minimizing long-term debt burdens.

Forgiveness Programs and Eligibility

Student loan forgiveness programs offer significant relief for borrowers, particularly the Public Service Loan Forgiveness (PSLF) program. Established in 2007, PSLF is designed for individuals employed by government or non-profit organizations, providing loan forgiveness after 10 years of qualifying payments under a qualifying repayment plan. Eligible loans include Direct Loans, while Federal Family Education Loans (FFEL) can be consolidated into a Direct Consolidation Loan. Additionally, the Teacher Loan Forgiveness program targets educators who work in low-income schools, allowing forgiveness up to $17,500 after five consecutive years of service. Borrowers must remain aware of specific eligibility criteria, such as full-time employment status and loan type, to maximize their potential benefits. Keeping diligent records and regularly checking for changes to programs through entities like the U.S. Department of Education enhances the chances of successful application for these life-altering forgiveness opportunities.

Financial Planning and Budgeting

Effective financial planning and budgeting are crucial for managing student loans, ensuring students can meet their educational expenses while avoiding overwhelming debt. The average student loan debt in the United States exceeds $30,000, with recent graduates facing repayment obligations that can last up to 30 years. Creating a realistic budget involves categorizing essential expenses such as tuition fees, textbooks, and living costs while considering income sources like part-time jobs or scholarships. Utilizing tools like budgeting apps or spreadsheets can help track spending and identify areas for savings. Additionally, understanding loan terms, including interest rates typically ranging from 3% to 7%, is vital for planning repayments. Prioritizing payments on high-interest loans can significantly reduce total costs over time, promoting financial health in the long run.

Read Also: Our Financial consultancy's Blogs

Comments