As we navigate the journey of retirement planning, it's essential to stay informed about your contribution options to secure your financial future. Whether you're just starting to save or looking to make adjustments to your existing plan, understanding how contributions work can significantly impact your retirement readiness. In this article, we'll explore the latest updates to retirement plan contributions and provide practical tips to help you maximize your savings. So, grab a cup of coffee, and let's dive deeper into how you can enhance your retirement strategy!

Image cover: Letter Template For Retirement Plan Contribution Update

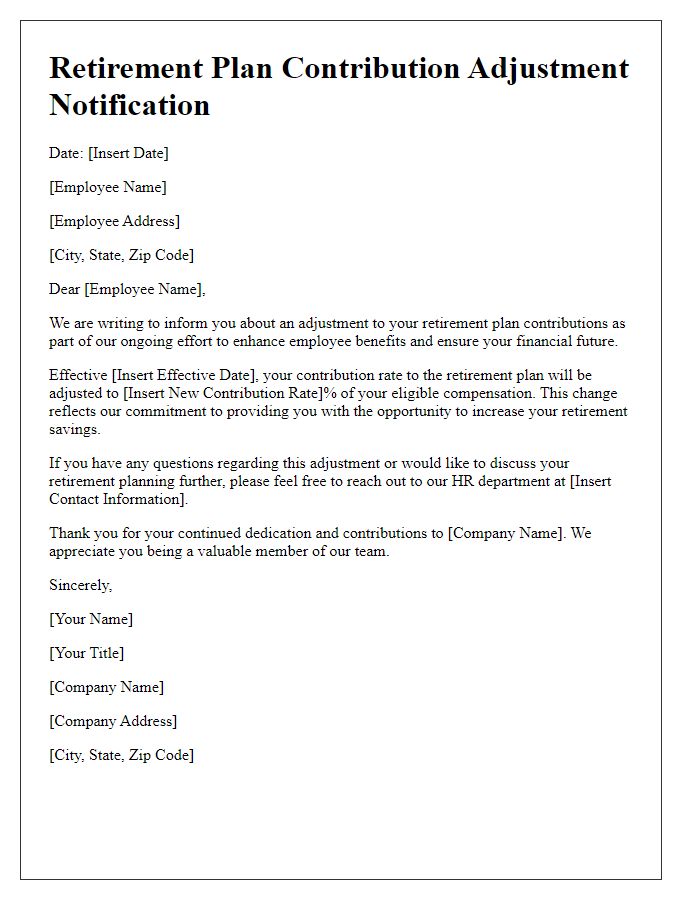

Letter Template For Retirement Plan Contribution Update Samples

Personal Information Update

Retirement plan contributions can significantly impact long-term financial stability. Regular updates to personal information, such as employment status (like transitioning from full-time to part-time work), address changes (to ensure correct tax documentation), or beneficiary designations (ensuring loved ones receive assets) are crucial. Employers often require documentation for changes in marital status or the addition of dependents, as these factors influence contribution limits and tax advantages. Accurate information ensures optimized benefits under federal regulations, such as ERISA (Employee Retirement Income Security Act), enhancing the retirement savings strategy.

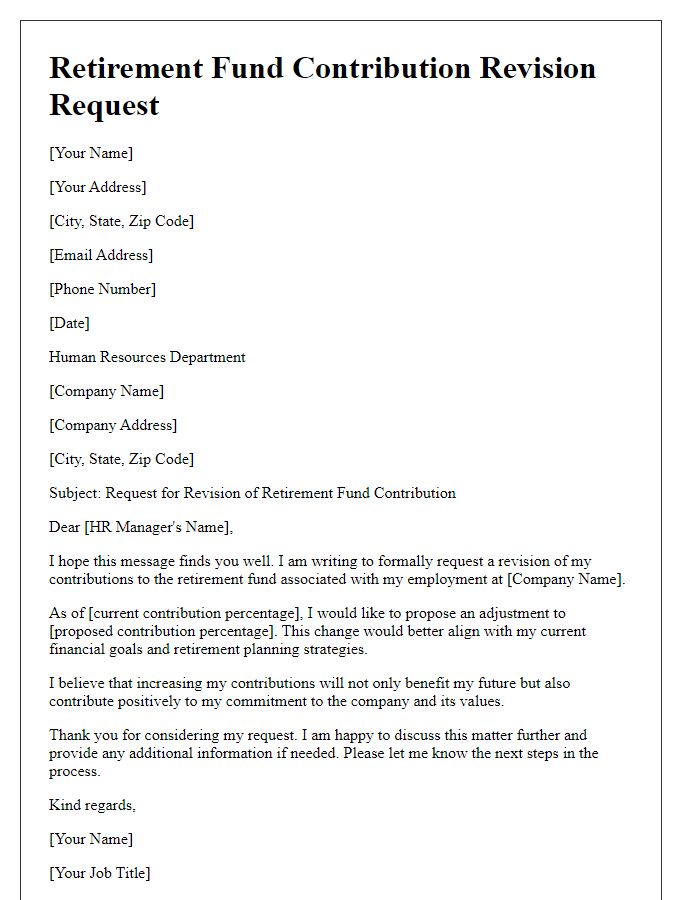

Contribution Amount Adjustment

During the 2023 fiscal year, many employees experienced adjustments in their retirement plan contributions, specifically in 401(k) programs, due to changes in income levels, employer policies, or IRS regulations. For instance, the IRS raised the contribution limits to $22,500 for individuals under 50 and $30,000 for those aged 50 and above, reflecting a significant increase from the prior year. Employees in diverse sectors, such as technology and healthcare, often find themselves reviewing their contribution amounts to optimize their retirement savings strategies, ensuring they leverage employer matching contributions and tax advantages effectively. Regular assessments of salary increments and expenditure changes can also inform these adjustments, aligning with long-term retirement goals for financial stability post-employment.

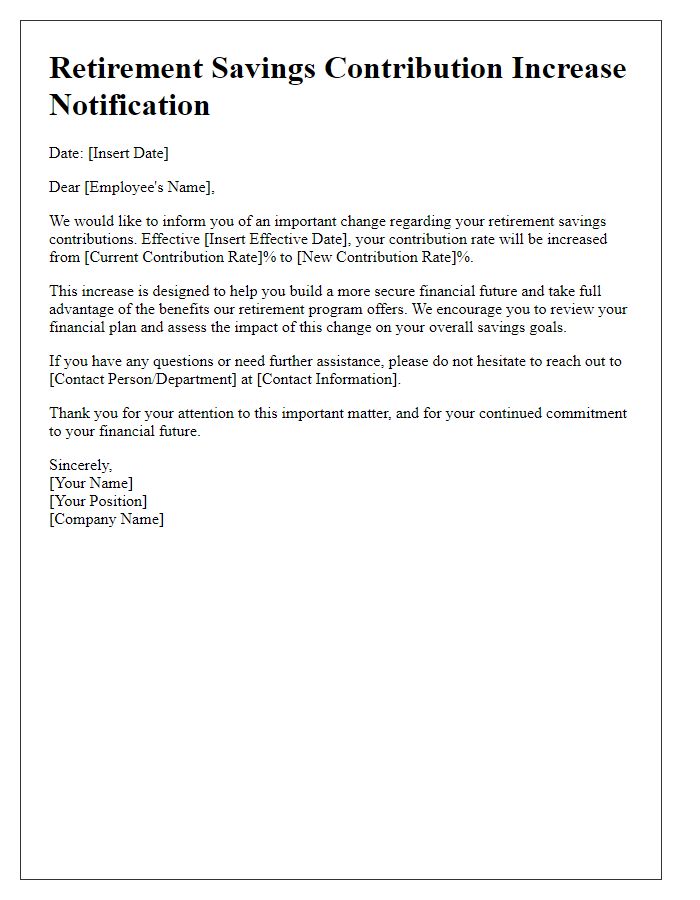

Plan Type and Details

Retirement plan contributions can significantly impact the long-term financial security of individuals. For example, 401(k) plans, often offered by employers, allow employees to contribute a portion of their salary, often matched up to a certain percentage by the employer. The contribution limits for 2023 have increased to $22,500 for individuals under 50 years old and $30,000 for those aged 50 and above, promoting savings for retirement. Additionally, Individual Retirement Accounts (IRAs) provide tax advantages, with contribution limits of $6,500 for individuals under 50 and $7,500 for those 50 and older. These contributions, whether traditional or Roth, can grow tax-deferred or tax-free, depending on the account type. Monitoring and updating contribution levels regularly can optimize retirement savings, ensuring a more secure financial future.

Automatic Enrollment Option

Automatic enrollment in retirement plans, particularly 401(k) plans, enables employees to save for their future with ease. This process typically enrolls eligible employees at a default contribution rate, often around 3% of their salary, unless they choose to customize their contributions. Organizations, such as Fortune 500 companies, utilize this option to increase participation rates, achieving upward of 80% engagement in some cases. Automatic escalation provisions may also be included, gradually increasing contributions by 1% each year until a maximum percentage, often set at 10%, is reached. This strategy promotes long-term financial security, as studies indicate that employees are more likely to remain invested in their retirement plans when automatic features are applied. Employees working in states with specific legislation, like California's Secure Choice program, may also encounter similar automatic enrollment frameworks designed to enhance retirement savings across diverse industries.

Beneficiary Designation Update

Updating beneficiary designations is crucial in retirement plans, such as 401(k) accounts or IRAs. Designating beneficiaries ensures that assets are transferred according to personal wishes after an individual's passing. For instance, the importance of keeping beneficiary information current becomes evident, particularly during major life events like marriage, divorce, or the birth of a child. To maintain alignment with personal intentions, individuals should review their designations regularly, especially when changes in tax laws or retirement account regulations occur. Employees should submit updates via official channels, ensuring compliance with plan rules and avoiding potential delays in fund distribution. Additionally, reviewing contact information for beneficiaries guarantees timely notifications in the event of a claim.

Read Also: Our Accounting firm's Blogs

Comments